This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

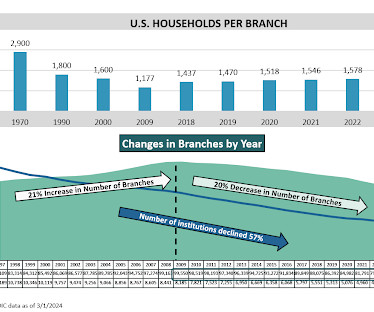

Communitybanks are pushing for a stronger role with their small business (SMB) customers. However, through an embrace of FinTech collaboration and industry consolidation, communitybanks appear poised to further dispel assumptions of a lack of digitization. has dropped from 8,000 in 2004 to about 5,400 in 2018.

Communitybanks are often the familiar faces of the financial services world, and when small businesses seek capital, their neighborhood financial institution can be a promising place to start. While they continue to play an important role in small business financing, the communitybanking market is drastically shrinking in the U.S.

Banks must plan for the possibility of high inflation and rising interest rates, not just for the next few years but perhaps for the remainder of the decade. This rapid change in interest rates requires careful planning, product selection, and new lending and deposit-gathering strategies. Jun 2004 – Jun 2006. Time Period.

Louis Fed recently performed a study to uncover the characteristics of communitybanks that thrived during the financial crisis. Thriving banks were defined as under $10 billion in assets, and maintained a composite CAMELS 1 rating in each exam cycle from 2006-11, an impressive accomplishment. Build a Better Lending Function.

September 2004, driving from a meeting in New York, on the grossly miss-titled Cross Bronx Expressway, Nathan Stovall, a reporter from SNL Financial gave me a call. The question: What was up with an upstate New York bank? of Ocala, Florida on the bank''s sale to Heritage Financial Group, Inc. He printed it as I said it.

And then what happened in 2004-06 happened again. Depositors woke up and thought "what is my bank paying me?" And, according to some EDP students that are lenders, are turning to the shadow banking market that do not have deposit demands. Such as direct lending funds, and insurance companies.

imberly Anderson, senior vice president and chief administrative officer of Cañon National Bank in southern Colorado, became her communitybank’s loan compliance officer in 2003. In early 2004, examiners visited her $253 million-asset bank, an experience that revealed a need—someone with a stronger compliance background. “I

It is the Mountlake Terrace, Washington holding company for 1st Security Bank, a $1.7 billion in assets communitybank with 22 branches that encircle the Seattle Sound. Their vision is simple: "Build a great place to work and bank." It is the $888 million holding company for Plumas Bank. First Capital, Inc.

The old borrow short, lend long strategy. I want to read to you the FDIC’s conclusion from their An Examination of the Banking Crisis of the 1980’s and Early 1990’s. percent in 2004, a decline of 1.1 By comparison, non-high-tech industries lost 689,000 jobs between 2001 and 2002 but recovered the lost jobs by 2004.

Indeed, banks generally pull back on lending if longer-term loan rates are less than their cost of funds, which are generally based on shorter-term rates. Dorothy has been with Penn CommunityBank and its predecessor since November, 2004. Since 1960, all six recessions have been preceded by inverted yield curves.

The bad news is the first review, conducted from 2004 to 2006, was a bust. Even though the industry identified several major regulatory burdens, including those posed by the Truth in Lending Act and the Home Mortgage Disclosure Act, few substantive regulations were repealed. Community Bankers Chosen as CFPB Advisors.

Readers note: You can also view this post on Penn CommunityBank's website. They also implemented large, aggressive borrowing and purchase programs for Treasuries, Agency mortgage backed securities, corporate bonds, municipal bonds, loans, commercial paper, banklending, and small business loan programs. Click here.

Banklending has not been the catalyst it used to be for improved growth in this recovery compared to prior ones; maybe we can point at regulation after regulation being forced onto banks and higher, more restrictive capital requirements. If bank regulations are lifted, lending and thus growth can improve.

2019 Mehrsa Baradaran Baradaran, Mehrsa The Color of Money: Black Banks and the Racial Wealth Gap 2019 Neil Barofsky Barofsky, Neil Bailout: An Inside Account of How Washington Abandoned Main Street While Rescuing Wall Street 2012 Patricia Beard Beard, Patricia Blue Blood and Mutiny: The Fight for the Soul of Morgan Stanley 2007 Ben S.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content