This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

And to thrive, those customers need economically diverse and healthy communities in which to live and work. Partnering with local organizations to promote the health of those communities is often a top priority for banks. communities where capital tends to be scarce.

Ready to catch the next wave of lending growth? Commercial and industrial lending (C&I) will be the next big performance driver for banks and credit unions. You might also like this paper on how institutions can produce smarter, faster lending. C&I lending will be the next “bomb.”

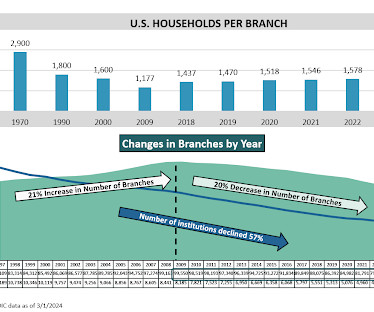

Community banks are pushing for a stronger role with their small business (SMB) customers. However, through an embrace of FinTech collaboration and industry consolidation, community banks appear poised to further dispel assumptions of a lack of digitization. has dropped from 8,000 in 2004 to about 5,400 in 2018.

This rapid change in interest rates requires careful planning, product selection, and new lending and deposit-gathering strategies. Jun 2004 – Jun 2006. Application to Community Banks. In today’s lending market, borrowers start from historically low interest rates, making the DSCR deterioration much more likely.

Louis Fed recently performed a study to uncover the characteristics of community banks that thrived during the financial crisis. It appears that banks that had the ability to do the same during the heady lending times of 2004 - 2007 found it to be an enduring strategy (see table from Fed study). Build a Better Lending Function.

September 2004, driving from a meeting in New York, on the grossly miss-titled Cross Bronx Expressway, Nathan Stovall, a reporter from SNL Financial gave me a call. The question: What was up with an upstate New York bank? My answer: The CEO was 67 years old and that would obviously be an impetus for a sale. He printed it as I said it.

And then what happened in 2004-06 happened again. Such as direct lending funds, and insurance companies. Shadow bank lending is similar to bank lending but is not subject to the same regulations, and compensating deposit balace requirements. Depositors woke up and thought "what is my bank paying me?"

imberly Anderson, senior vice president and chief administrative officer of Cañon National Bank in southern Colorado, became her community bank’s loan compliance officer in 2003. In early 2004, examiners visited her $253 million-asset bank, an experience that revealed a need—someone with a stronger compliance background. “I By Ed Avis.

The bad news is the first review, conducted from 2004 to 2006, was a bust. Even though the industry identified several major regulatory burdens, including those posed by the Truth in Lending Act and the Home Mortgage Disclosure Act, few substantive regulations were repealed. Community Bankers Chosen as CFPB Advisors.

The joint complaint filed by the CFPB and DOJ in federal district court in New Jersey states that the action resulted from a joint investigation by the agencies of the bank’s lending practices following the CFPB’s referral of the bank to the DOJ pursuant to the ECOA.

And Blockbuster, which in 2004 had about 60,000 employees and more than 8,000 stores, was in bankruptcy by 2010 because Netflix and other on-demand video providers figured out how to deliver a much more convenient and rewarding experience. Many major hotel chains are aware that their market valuation has been eclipsed by Airbnb.

billion in assets community bank with 22 branches that encircle the Seattle Sound. But in 2004 they converted to a mutual savings bank, and then in 2012 converted to shareholder owned. Founded in 1980, Plumas Bank is a full-service community bank headquartered in Quincy in Northeastern California. First Capital, Inc.

The old borrow short, lend long strategy. percent in 2004, a decline of 1.1 By comparison, non-high-tech industries lost 689,000 jobs between 2001 and 2002 but recovered the lost jobs by 2004. Who would’ve thought lending $1 million to a San Francisco cab driver to buy a house at 100% loan to value would go bad?

It seems to me that reducing burdensome regulations and not implementing harsher capital requirements would be more effective alternatives to incentivize lending than pushing all yields toward zero while buying up all of our bonds. Dorothy has been with First Federal of Bucks County since November, 2004.

Indeed, banks generally pull back on lending if longer-term loan rates are less than their cost of funds, which are generally based on shorter-term rates. Dorothy has been with Penn Community Bank and its predecessor since November, 2004. Since 1960, all six recessions have been preceded by inverted yield curves.

Readers note: You can also view this post on Penn Community Bank's website. They also implemented large, aggressive borrowing and purchase programs for Treasuries, Agency mortgage backed securities, corporate bonds, municipal bonds, loans, commercial paper, bank lending, and small business loan programs. Click here. Congress passed $2.3

Community banks are often the familiar faces of the financial services world, and when small businesses seek capital, their neighborhood financial institution can be a promising place to start. While they continue to play an important role in small business financing, the community banking market is drastically shrinking in the U.S.

Lending Club made changes to its business model that created new opportunities for growth. Lending Club. Thiel became an outside board member with his $500K seed investment in Facebook in 2004. in its 2004 IPO, however, the deal made NEA many multiples in returns. Between 1999 and 2004, $1.8T Delivery Hero.

Bank lending has not been the catalyst it used to be for improved growth in this recovery compared to prior ones; maybe we can point at regulation after regulation being forced onto banks and higher, more restrictive capital requirements. If bank regulations are lifted, lending and thus growth can improve.

Essays on the Great Depression 2004 Ben S. A Term at the Fed: An Insider's View 2004 John Moody Moody, John The Masters of Capital: A Chronicle of Wall Street 2012 George S. Bye Bye Banks: The End of Community Banking as an Engine of Economic Growth 2010 Robert H. Bernanke Bernanke, Ben S. Bernanke Bernanke, Ben S.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content