This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

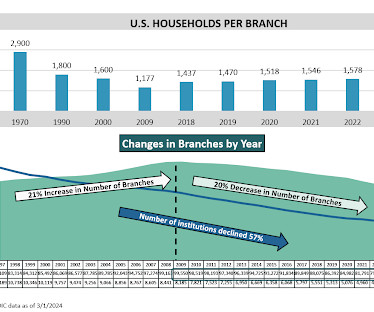

Community banks are pushing for a stronger role with their small business (SMB) customers. However, through an embrace of FinTech collaboration and industry consolidation, community banks appear poised to further dispel assumptions of a lack of digitization. has dropped from 8,000 in 2004 to about 5,400 in 2018.

PYMNTS recently spoke with Saqib Sheikh, global head of SWIFT’s ISO 20022 program, to learn more about SWIFT’s commitment to assist the financial community in the transition to the new standard in cross-border payments: ISO 20022. In 2004, financial institutions around the world had had enough. A Gradual Move With Big Benefits.

Community banks are often the familiar faces of the financial services world, and when small businesses seek capital, their neighborhood financial institution can be a promising place to start. While they continue to play an important role in small business financing, the community banking market is drastically shrinking in the U.S.

Jun 2004 – Jun 2006. Application to Community Banks. While we broke down the seven waves of impact that banks need to be concerned about across the enterprise ( HERE ), there are several immediate risks from inflation and persistently rising interest rates for community banks. Time Period. Total Change in Fed Funds. (%).

In our previous article ( HERE ), we reviewed the banking industry’s cost of funding earning assets (COF), and we compared how community banks’ COF behaves relative to national banks in a rising interest rate cycle. Second, the market has priced in interest rate risk, but it has not priced liquidity risk.

Financial Markets Update – Third Quarter 2024 I had a fantastic September traveling to France and Luxembourg with my sisters. You wouldn’t know we have recession risk when stocks are rampaging; markets crashed for a day on August 5 th but recovered in mere days. 5% in a short period), with the unemployment rate at 4.2% on average.

Financial Markets Update – Second Quarter 2024 A dream vacation! One of the components of the LEI which is up strongly is the S&P 500 stock market index, by +14.5%. So, you tell me, is this a strong labor market? To me, they were worth tracking as an indicator of the mortgage whole loan versus MBS market spread.

In the markets, we watched helplessly as real GDP plummeted -5% in 1Q20 and -31% in 2Q20 before rebounding by +33% in 3Q20. I’ve previously theorized that China would try to reclaim its global market share lost during the pandemic by flooding the markets with cheaper goods. This development could give us good news on inflation.

Conceived in 2004 and launched on Walmart.com, Triad Retail Media now has 13 offices worldwide with more than 600 global team members. We need to anticipate trends and understand where the market is moving toward. We create advertising and marketing campaigns that are personalized for the shopper, at scale.

We have discussed the importance of the CLV metric HERE , or bankers can look up our favorite academic paper on the topic “ Counting Your Customers Research Paper 2004 ” by Fader, Hardie, and Lee at Wharton. Lesson 1: Better Optimize Your Marketing Dollars For Cumulative Lifetime Value. Yet, it happens every day.

What we’re doing right now is we’re looking at our processes in place … to make sure this doesn’t happen again,” said Rene Daniels, director of communications and community engagement for Spotsylvania County Public Schools, according to the site, which added that no personal details or confidential information were compromised.

Across all asset sizes, the top 10 C&I lenders have nearly 49% market share of commercial lending. 2004-2008: 82.6% trillion “wave” of C&I lending expected in years ahead will position financial institutions for better performance and the ability to better serve the needs of their communities. 2010-2023: 137.3%

And then what happened in 2004-06 happened again. The Fed has paused for nearly a year now, and it was our experience in 2006-07 that bank cost of funds continued to increase as the market closed the delta between what someone could earn in a money market mutual fund and a bank account. Cost of funds is leveling off now.

In 2004, the infamous Riggs Bank (Riggs) case brought political corruption to the top of compliance officers’ lists of reasons not to sleep at night. have not historically seen this as a serious risk to their financial institutions, especially at the community financial institution level. Even at the community level, U.S.

Money market total financial assets, according to the St. But money market mutual funds seemed to be the benefactor of the switch. As far as community banks, I look to data gleaned from all of the banks where my firm does profitability outsourcing because we have a level of granularity that the FDIC and most readers do not have.

Never Satisfied The markets never seem to be satisfied. The Federal Reserve recently took heed of market and economic messages, ending its tightening campaign and beginning its “patience” campaign. The markets hardly seemed satisfied with these two moves as they began building in rate cuts. A Win for the Ages !

Rouse’s communications director, Robert Rubenkonig, said in a 2004 Shopping Centers Today story that the developer sought to create “community picnics” with the concept. At the Empire Stores complex in Brooklyn, the Time Out Market New York is set to open in 2019. They’re open areas — a great idea that stuck,” he said.

After easing and keeping rates low for three years, the Fed began tightening from June, 2004 to June, 2006. There are some signs of slowing in the housing markets; both existing and new home sales in June fell amidst rising mortgage rates and fewer gains in home prices. Consider the trade wars and tariffs.

Quarterly Financial Markets & Economic Update- October, 2017 I love this time of year. The markets have not given way to anything, with long term bonds still trading in a tight range and short term rates having risen from Fed action. Dorothy has been with Penn Community Bank and its predecessor since November, 2004.

Louis Fed recently performed a study to uncover the characteristics of community banks that thrived during the financial crisis. It appears that banks that had the ability to do the same during the heady lending times of 2004 - 2007 found it to be an enduring strategy (see table from Fed study). And fire your strategists.

Financial Markets & Economic Update - Fourth Quarter 2023 Summer Update On this warm October day, I am staring at my Bloomberg screen, still heartbroken over the Phillies Phailure. But not in this market. Stock markets have been very volatile and are mostly down since the summer months. for the Case Shiller 20, +2.6%

The markets continue to roll and bond markets continue to trade in a 25 basis point range, hitting the higher end when they think the economy is strong (why else would the Fed raise rates?) Presidential Agenda I am very surprised that the markets are not having fits over the lack of progress on the presidential agenda.

Readers note: You can also view this post on Penn Community Bank's website. As the stock market faltered in March, we saw the Federal Reserve step up with emergency rate cuts and Quantitative Easing to buy bonds. and promised trillions of dollars to stabilize the markets. The actions taken by the Fed stabilized markets.

After a lengthy stretch of strong economic growth and stock market gains, the inevitable correction arrived with force in the fourth quarter, culminating with a December that can only be described as “tres terrible!” Dorothy has been with Penn Community Bank and its predecessor since November, 2004. 50% between 2 and 10 years.

Trade wars and tariffs dominated the market discussion in the third quarter with talk quieting down for now. Dorothy has been with Penn Community Bank and its predecessor since November, 2004. The curve is not close to inverted yet, but if it does, it will be a precursor of tough economic times ahead.

Stock markets hit new highs in January and quickly began a long and painful sell-off that has continued into May. High mortgage rates will begin to affect the housing markets. I’m sure you’ll enjoy his insights on the markets and the economy as much as I have. I’m very happy to introduce our guest writer for this quarter.

The $120 million-asset community bank made the reverse move and relocated from the outskirts of the city into a vacant building in the heart of downtown. “We Founded in 2004, Thurston First Bank’s headquarters was located in a residential neighborhood north of downtown. Olympia, Wash., Then Thurston First Bank stepped in.

Financial Markets & Economic Update- Third Quarter, 2019 Summer is upon us and I cannot wait to get to the beach for vacation. Although business confidence fell from the uncertainty, stock markets were reaching new record highs on many of indices. Dorothy has been with Penn Community Bank and its predecessor since November, 2004.

The businesses that we track and profile in our Store Front Index — the home remodelers, salons, spas, small retailers, delis, coffee shops and restaurants that contribute to the health and vitality of the local communities — are not only declining, they’re not even getting off the starting blocks. But maybe that’s the good news.

Stock and bond market volatilities are also seeing winter squalls and are sending messages about shifting investor sentiments about risk. Now we will see if the Fed can keep it from becoming “sustained,” with wage inflation from tight labor markets filtering into the prices of all goods and services. in January. 76%, the 5 year is up.40%

And as part of the ASB merger, the foundation will commit at least $500,000 per year to ASB markets. Could it have been too much of a burden to deliver the same level of profits and have the same market valuations? I realize that other banks give time and treasure to support their communities. So the giving will continue.

The markets are taking it all in stride, rallying strongly for most of this week and they seem more grateful for the prospect of a divided Congress, i.e, The markets believe the chance of tax hikes, repeals of tax cuts, and gigantic initiatives are greatly diminished. The housing market is robust across the nation.

Financial Markets & Economic Update -Fourth Quarter 2022 What a year 2022 has been! We’ve seen tremendous market declines in both stocks and bonds, volatility, and a Federal Reserve who is raising interest rates at a breathtaking pace. Housing markets have suffered, with mortgage rates climbing up to 7.00%. in September.

Financial Markets & Economic Update -Third Quarter 2022 Inflation The Federal Reserve waited too long before beginning its fight against inflation. Even more egregiously, the Fed continued to purchase $100 billion of Treasury and Agency bonds in the market each month through March, 2022! in June, 2022, compared to +12.4%

imberly Anderson, senior vice president and chief administrative officer of Cañon National Bank in southern Colorado, became her community bank’s loan compliance officer in 2003. In early 2004, examiners visited her $253 million-asset bank, an experience that revealed a need—someone with a stronger compliance background. “I By Ed Avis.

The bank engaged in limited marketing outside of its branch network that focused on neighborhoods with relatively few Black and Hispanic residents and therefore “failed to advertise meaningfully in majority-Black-and-Hispanic neighborhoods.”

Lab126 was created by Amazon in 2004 for the purpose of creating the Kindle eReader. In fact, as the Bloomberg story details, a lot of steps taken on the path to creating — and selling — the Echo, at times, portended something of a disaster.

Many major hotel chains are aware that their market valuation has been eclipsed by Airbnb. And Blockbuster, which in 2004 had about 60,000 employees and more than 8,000 stores, was in bankruptcy by 2010 because Netflix and other on-demand video providers figured out how to deliver a much more convenient and rewarding experience.

percent to 4 percent since 2001-2004; severe obesity has expanded from 6 percent of urban females to 8 percent. And working to capture a piece of that $60 billion market – and hopefully help to boost its success rate to somewhere north of 20 percent – is Noom. Urban men’s severe obesity rate has climbed from 2.4

US stocks fell 6% to 7% during the first week of January, following world stock markets in a downward spiral. Its stock markets are said to have led the world markets plunge, with clumsy attempts by their regulators’ circuit breakers to stem declines actually making them worse. First and foremost, China is at it again.

I chose five years because banks that focus on year over year returns tend to cut strategic investments come budget time, which hurts their market position, earnings power, and future relevance than those that make those investments. billion in assets community bank with 22 branches that encircle the Seattle Sound. First Capital, Inc.

First of all, if they continue to buy securities, they are removing many of the high quality securities from the marketplace, possibly causing a disruption or shortage in the markets. We may be skeptical, but the markets keep telling us: Don’t fight the Fed! Dorothy has been with First Federal of Bucks County since November, 2004.

percent in 2004, a decline of 1.1 By comparison, non-high-tech industries lost 689,000 jobs between 2001 and 2002 but recovered the lost jobs by 2004. Between 1995 and its peak in March 2000, the Nasdaq Composite stock market index rose 800%, only to fall 740% from its peak by October 2002, giving up all its gains during the bubble.

If selling in stocks and bonds begins in earnest over this crisis, we will have some of the first tests of liquidity in the markets since new regulations kicked in and restricted financial institutions from trading or making markets. Dorothy has been with First Federal of Bucks County since November, 2004. Stay tuned!

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content