This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

To provide a report card on industry status and performance, the FDIC publishes a Quarterly Banking Profile. Results from the third quarter were just released, and while overall results were positive, communitybanks in particular excelled. Communitybanks’ net income grew almost 11 percent to $4.9

The latest FDIC Quarterly Banking Profile was just released and the industry continues to be led by the nation’s communitybanks. percent of communitybanks were unprofitable during the quarter. However, across all banks, fourth quarter net income fell by 7.9 Communitybank loan balances also rose 2.5

The latest FDIC Quarterly Banking Profile was just released and the industry continues to be led by the nation’s communitybanks. percent of communitybanks were unprofitable during the quarter. However, across all banks, fourth quarter net income fell by 7.9 Communitybank loan balances also rose 2.5

It is only natural for communitybanks to have loan concentrations that result from the market(s) they serve and the markets they pursue. In today’s times, a high commercial real estate (CRE) concentration is often the result of communitybanks pursuing opportunity in the market.

Jun 2004 – Jun 2006. Application to CommunityBanks. While we broke down the seven waves of impact that banks need to be concerned about across the enterprise ( HERE ), there are several immediate risks from inflation and persistently rising interest rates for communitybanks.

Louisa CommunityBank of Louisa, Kentucky also shuttered on Oct. 25, and the assets were purchased by Kentucky Farmers Bank Corporation in Catlettsburg, Kentucky. As of June 30, Louisa CommunityBank had approximately $29.7 Enloe State Bank of Cooper, Texas closed May 31 with total assets of $36.7

8/ @Schornack It is a niche that has only grown over time and one that has shown very little net losses since we started making these loans around the U of M in 2005-2006. 9/ @Schornack Running a bank is not much different than running a small business. Basic idea is that sales to a bank are loans. Inventory are deposits.

Before this year, the last time that happened was in 2006, when Walmart made a move on an ILC. Walmart initially had sought to own a bank that offered full consumer banking services – though by time of its final push 11 years ago, that ambition had been radically scaled back. ” An Unleveled Playing Field.

We let our actions speak for the bank.” Mark Zaback, Jonah Bank of Wyoming. Under the big Montana sky, Mark Zaback helps lead a communitybank with a cowboy code. Mark Zaback , Jonah Bank of Wyoming. Bank assets: $280 million. Jonah Bank is so much more than Mark Zaback,” he says. Casper, Wyo.

For example, loans originated in 2006 would show credit stress two to four years later. For many credits of an average-sized communitybank, ROE is highest for loans with terms from five years or longer. The pools can be analyzed for delinquencies, payoff trends, losses (typically charge-offs) and profitability.

Bradley Linskens was reportedly removed from his position as a result of the bank’s unauthorized accounts scandal that surfaced last year. According to Reuters, Linskens began oversight at Wells Fargo back in 2006 and was responsible for day-to-day supervision of the financial institution. Maxine Waters, U.S.

The Bank of Glen Ullin sets itself apart from other communitybanks through our strong involvement in the community we serve and the personal relationships we have with our customers. Our bank team is devoted to providing the quality service to our customers, whom we know on a first-name basis. Assets: $54 million.

Of course, Basel III—otherwise known as the Third Basel Accord—is a global regulatory framework on bank capital adequacy, stress testing and market liquidity risk. Most concerning has been the safety-and-soundness regulation’s unnecessary effect on reducing certain lending by communitybanks, say Kendrick and several community bankers.

As far as communitybanks, I look to data gleaned from all of the banks where my firm does profitability outsourcing because we have a level of granularity that the FDIC and most readers do not have. This was similar to the tightening cycle between 2004 and 2006 when Fed Funds rose again to 5.25%-5.50%.

Louis Fed recently performed a study to uncover the characteristics of communitybanks that thrived during the financial crisis. Thriving banks were defined as under $10 billion in assets, and maintained a composite CAMELS 1 rating in each exam cycle from 2006-11, an impressive accomplishment.

The first tweet ever written was by co-founder Jack Dorsey on March 21, 2006, at 9:50 p.m., According to a statistic released as part of the ICBA 2014 Top 50 CommunityBank Leaders in Social Media, nearly 2,500 banks have a Facebook or Twitter presence, and the numbers continue to exponentially grow.

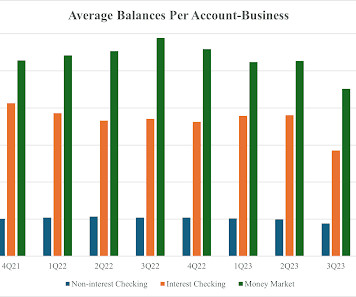

In the chart below, derived from The Kafafian Group’s (TKG) peer database of hundreds of communitybank branches, we see that the revenue generated from deposit spreads, asset spreads (typically consumer loans), and fees (typically deposit fees) as a percent of branch deposits averaged 2.08% for commercial banks and 1.88% for thrifts during 2014.

Today, I read an American Banker article on how a multi-billion dollar bank is going to ramp up its business lending. Reading between the lines, this bank is likely over the CRE guidance levels, and were probably getting grief from their regulators about it. We perform this service for dozens of communitybanks.

It's like 2006 all over again. When I asked a communitybank director of marketing about rate promotions and the success at turning them into loyal, core deposit customers, she was skeptical. A quick search on "bank rate promotions" gave me a trove of sites to compare offers, including this Nerd Wallet article.

It appears Mr. Davis and his communitybank outdid them both in ''09, and blew the cover off of the industry. Looking back to 2006, the years Mr. Stumpf assumed WFC''s presidency and Mr. Dimon ascended to JPM''s CEO chair, Bill Davis fared relatively well. Not too shabby Mssrs. Dimon and Stumpf. But hold on fellas.

Unsurprisingly, the largest declines occurred starting monthly in March, 2006 and on a y-o-y basis in September, 2006 and continued to November, 2009. We all remember the Great Recession, which began in 2007, but the LEI knew it as early as March, 2006. The largest monthly decline took place in May, 2009 at -27.2%

After easing and keeping rates low for three years, the Fed began tightening from June, 2004 to June, 2006. In my career, I’ve lived through many years of the Fed raising interest rates and it’s my experience that they usually tighten too much and keep rates high for too long, just like in 2001 and 2006-2007.

Depositors woke up and thought "what is my bank paying me?" The Fed has paused for nearly a year now, and it was our experience in 2006-07 that bank cost of funds continued to increase as the market closed the delta between what someone could earn in a money market mutual fund and a bank account.

Given communitybanks’ propensity to do real estate transactions, why wouldn’t such a fee-based line of business flourish? My company measures the profitability of products and lines of business for community financial institutions (“FIs”). Community FIs, in general, are not making money with these products.

Outside of those two crisis periods, American banking failures have generally been uncommon, at least since the end of the Great Depression. banks failed a year. bank failures per year between 1996 and 2006, and 3.6 Before SVB, Signature, and First Republic, in fact, it had been over two years since the last bank failure.

In 2006, when the median asset size within my firm's profitability outsourcing service was $696 million, the operating cost per business checking account was $586 per year. For example, deposit operations' expense as a percent of deposits should decline as the bank grows. Forget the things outside of your control.

It should be noted that in 2006, 40% of purchase mortgages were for investment or vacation property. Note the absence of anything resembling a communitybank. First Franklin, a JV between National City Bank (emergency sale to PNC) and Merrill Lynch (emergency sale to BofA). In 2007, that number climbed to 127%.

Both spread inversions precede recession by 13 months (as in 2000 for the 2001 recession) to 26 months (as in 2006 for the 2008-2009 recession). DJ 07/16/19 Dorothy Jaworski has worked at large and small banks for over 30 years; much of that time has been spent in investment portfolio management, risk management, and financial analysis.

We are located in a historic structure that was built in 1800 by Benjamin Harrington, directly across the street from the new branch of Union Bank. We started the business in 2006 here in Shelburne and moved to our present location in 2014. Get involved!” Stay Local.

OTCQX: FETM) In 2006, Fentura Financial, the holding company for the creatively named State Bank, had over $620 million in total assets, $51 million in total equity, an 0.85% ROA, and a book value per share of $24.08. Those investors that jumped onboard at the end of 2010 were well rewarded. Their total return was greater than 1,000%.

I may have missed some decorations that had already been stored in the banks’ virtual attics. Previous year-end holiday posts: 2015 , 2014 , 2013 , 2012 , 2011 (big banks), 2011 (CUs/communitybanks), 2009 part 1 , 2009 part 2 , 2007 , 2006 , 2006 , 2004. ———-. 2016 Holiday Messages.

Sherrod Brown (D-Ohio), two lawmakers tapped to lead the Senate Banking Committee for their respective parties, are both independent-minded senators who hold positive views on several priority communitybanking issues. Richard Shelby (R-Ala.) So I would say he’s open to things we are concerned about.”.

The good news is the law compels the federal banking agencies to review regulations they have issued to identify those that are outdated, unnecessary or unduly burdensome. The bad news is the first review, conducted from 2004 to 2006, was a bust. Community Bankers Chosen as CFPB Advisors. in Lowell, Mass.; in Lowell, Mass.;

We have many examples, notably 2000-2001, 2006-2008, and 2019, when restrictive rates impaired growth and recession followed. DLJ 06/30/24 Dorothy Jaworski has worked at large and small banks for over 30 years; much of that time has been spent in investment portfolio management, risk management, and financial analysis.

Ted Whitehurst, Providence Bank president and CEO, led the charge to open a new brick-and-mortar location of the Raleigh, N.C., communitybank during the pandemic. Providence Bank chose to open a new brick-and-mortar site during the pandemic, when many other businesses were ceasing operations or shutting down altogether.

Six years ago I asked in a blog post Will Plain Vanilla Kill CommunityBanking ? Didn't even exist in 2006. How do we balance strategic direction, customer demand, and the futurist or wildly over-caffeinated millennial that tells us we have to implement every shiny new object or we'll die? Was I, gulp, a futurist?

(Nasdaq: OZRK) of Little Rock, Arkansas Over a 100-year banking history, Bank of the Ozarks expanded from its headquarters in Little Rock, Arkansas, to more than 100 locations throughout the Southeast and is consistently ranked among the top performing banks in America (see chart). Their ROA in 2006 when their assets were $2.5

Known by his nickname Buz, John Gorman helped the Conference of State Bank Supervisors launch its nationwide cooperative agreement in 2006 and the National Multistate Licensing System for mortgage lenders two years later.

Previous year-end holiday posts: 2014 , 2013 , 2012 , 2011 (big banks), 2011 (CUs/communitybanks), 2009 part 1 , 2009 part 2 , 2007 , 2006 , 2006 , 2004. Banks in the Holiday Spirit. Following is a quick overview of the promotions, including a 1- to 5-bulb rating.

Other People's Money: How Banking Worked in the Early American Republic 2017 Allen Nevins Nevins, Allen History of the Bank of New York and Trust Company, 1784-1934 2006 George A. Irrational Exuberance 2006 William L. Bye Bye Banks: The End of CommunityBanking as an Engine of Economic Growth 2010 Robert H.

It is a concept that we have all heard of, however, the concept remains somewhat of a mystery in the communitybank world. Ultimately it poses a serious threat to global stability with the potential for catastrophic loss of life if a weapon of mass destruction was deployed.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content