This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

To provide a report card on industry status and performance, the FDIC publishes a Quarterly Banking Profile. Another bright spot: less than seven percent of community banks were unprofitable – the lowest since the second quarter of 2006. They performed better than a year ago and also outperformed the industry as a whole.

Governed by an interagency agreement among the Federal Reserve, the Federal Deposit Insurance Corporation (FDIC) and the Office of the Comptroller of the Currency (OCC), the program review credits with minimum aggregate loan commitments totaling $100 million or more that were shared by three or more regulated financial institutions.

recorded its fourth bank failure this year — the first collapse of financial institutions since 2017, according to data from the Federal Deposit Insurance Corp ( FDIC ). Assets and deposits were assumed by Industrial Bank, a press release from the FDIC indicated. “On Approximately $500,000 in deposits exceeded FDIC insurance limits.

The FDIC recently reiterated that financial institutions should determine whether loans affected by COVID-19 should be reported as TDRs. FDIC Issues Reminder of TDRs. FDIC, OCC, FED. 2006 Policy Statement on Prudent Commercial Real Estate Loan Workouts. FDIC, OCC, FED. It’s not a way for us to mask problems.”.

Last year was the first time since 2006 that not one U.S. FDIC) was founded in 1933 that an entire year went by without a bank going under. Sears is still in the bid game, a mobile banking operator thinks big and holiday sales in the U.K. disappoint. US Banking Industry Had No Failures in 2018.

The latest FDIC Quarterly Banking Profile was just released and the industry continues to be led by the nation’s community banks. This marked the largest gap since the fourth quarter of 2006. The FDIC’s “Problem List” dropped to 291 institutions, from 329 in 2013. Loan balances continue to increase.

The latest FDIC Quarterly Banking Profile was just released and the industry continues to be led by the nation’s community banks. This marked the largest gap since the fourth quarter of 2006. The FDIC’s “Problem List” dropped to 291 institutions, from 329 in 2013. Loan balances continue to increase.

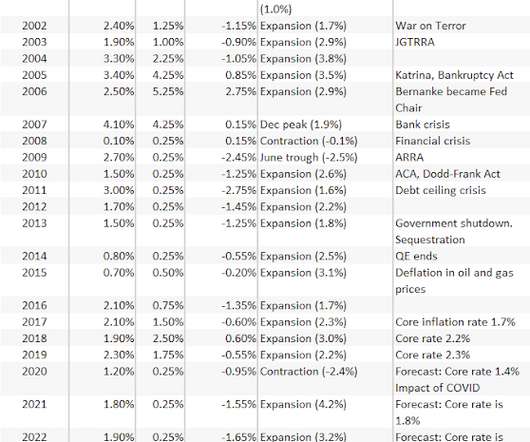

Over the next two years, the Fed raised rates 16 more times, ending at 5.25% on June 29, 2006 (see chart). When the Fed ended its tightening in June 2006 at 5.25%, bank cost of deposits was 2.68%, a significant spread. Yes, non-core deposits as a percent of total deposits grew from 32% in June 2004 to 38% in June 2006.

An industrial bank is an FDIC-insured depository institution that is generally subject to the same banking laws and regulations as any other bank charter type, with the important exception of the Bank Holding Act of 1956. Before this year, the last time that happened was in 2006, when Walmart made a move on an ILC.

Ashbaugh highlights that as of 2006, 31% of US banks exceeded at least one of the limits, and that 23% of banks that exceeded both limits failed, while 13% of banks that exceeded the construction limit failed. That 13% represented 80% of the losses to the FDIC insurance fund.

trillion in domestic deposits, according to the FDIC's Statistics at a Glance. As far as community banks, I look to data gleaned from all of the banks where my firm does profitability outsourcing because we have a level of granularity that the FDIC and most readers do not have.

This distress was clearly evident when I recently performed some "where are they now" research on the highest performing ROE FIs in 2006, the last normal year prior to the crisis (see table). I searched all publicly traded banks and thrifts that existed in 2006 and sorted them by the highest ROE. A note on the data. Yes, failed.

They acquired seven failed institutions in Georgia, Florida, and South Carolina from the FDIC, adding over $2 billion of acquired assets since March 2010. Bank of the Ozarks has historically been a very good performer as they grew and prior to their recent FDIC deal binge. Their ROA in 2006 when their assets were $2.5

She began her 17-year banking career as an FDIC examiner. She has been with the bank since 2006. We are deeply devoted to our mission, to our customers, to our neighbors and, ultimately, to our community. Jolene Muscha is president of the Bank of Glen Ullin.

The DOJ investigation centered on whether LendingClub had – between January 2009 to September 2010 – misled its FDIC-insured loan originator, WebBank , leading the bank to underwrite over 200 loans that did not conform to the bank’s lending requirements. The DOJ Finding. The Rundown on the Run-up to the Decisions.

If this were 2006, things would be good. Retiree: That's Not So Funny To the retiree that prefers the safe haven of FDIC insured deposits held at the local bank that lends it out locally, this is a serious issue. You've been conservative, preferring the stability and security of bank deposits versus the gyrations of the market.

To remind readers, in 2006 the OCC, Federal Reserve, and FDIC issued joint interagency Guidance on Concentrations in Commercial Real Estate Lending. Reading between the lines, this bank is likely over the CRE guidance levels, and were probably getting grief from their regulators about it. Maybe sub out an economist or two.

According to my firm’s profitability database, branches generated revenue (defined as consumer loan spreads, deposit spreads, and fees) as a percent of branch deposits of 3.50% in 2006. Today, that number is 2.08% due to the interest rate environment, the regulatory environment (reducing deposit fees), and customer behavioral changes.

When I wrote that post in January 2011 there were 7,700 FDIC insured financial institutions. Didn't even exist in 2006. Six years ago I asked in a blog post Will Plain Vanilla Kill Community Banking ? Did I get caught up in the change-or-die crowd? Was I, gulp, a futurist? Today there are less than 5,700. A 26% decline.

In 2006, when the median asset size within my firm's profitability outsourcing service was $696 million, the operating cost per business checking account was $586 per year. Forget the things outside of your control. These five themes are firmly within your ability to make a positive impact on your future. deposit market share in 2012 to a 80.7%

bank failures per year between 1996 and 2006, and 3.6 According to the FDIC, the causes of the 2008-09 financial crisis lay partly in the housing boom and bust of the mid-2000s; partly in the degree to which the U.S. In 2006, the then $686 million in asset bank made $8.8 Between 1941 and 1979, an average of 5.3

2/ @Schornack The primary asset of the organization was Flagship Bank Minnesota, a Member FDIC and Equal Housing Lender with two locations in the Twin Cities Metro Area. 8/ @Schornack It is a niche that has only grown over time and one that has shown very little net losses since we started making these loans around the U of M in 2005-2006.

Federal Deposit Insurance Corporation (FDIC) data, however, shows that the industry’s overall headcount has shrunk only 16 times as of 1935. According to a report in January, citing Calculated Risk, last year was the first time since 2006 that not one U.S. In separate news, U.S. In separate news, U.S.

Federal Deposit Insurance Corporation (FDIC) data, however, shows that the industry’s overall headcount has shrunk only 16 times as of 1935. According to a report in January, citing Calculated Risk, last year was the first time since 2006 that not one U.S. In separate news, U.S. In separate news, U.S.

Amid rising revenues and decreased taxes, the Federal Deposit Insurance Corporation (FDIC) announced on Thursday (Feb. In an announcement , FDIC Chairman Jelena McWilliams said, “Loan balances expanded, net interest margins improved and the number of ‘problem banks’ continued to decline.”. At the same time, interest income jumped by 8.1

According to a report in CNBC , citing Calculated Risk, last year was the first time since 2006 that not one U.S. FDIC) was founded in 1933 that an entire year went by without a bank going under. If a bank fails, the regulator looks to sell the assets to another bank and the FDIC assumes responsibility for the remaining assets.

Inside the FDIC: Thirty Years of Bank Failures, Bailouts, and Regulatory Battles 2015 Louis D. Other People's Money: How Banking Worked in the Early American Republic 2017 Allen Nevins Nevins, Allen History of the Bank of New York and Trust Company, 1784-1934 2006 George A. Irrational Exuberance 2006 William L.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content