This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This article covers these key topics: The evolution of AI Lending: A legacy of data-driven innovation Generative AI in lending: The next frontier Abrigo's approach to AI Parallel journeys of AI, banking technology Artificial intelligence (AI) is often heralded as a revolutionary force in todays world, but its story stretches back decades.

As banks are increasingly playing a bigger role in commercial real estate lending, it is more important than ever to ensure proper risk management practices. As a result, many banks are moving back into commercial real estate lending and borrowers are presented with more options. According to Forbes , U.S. According to Forbes , U.S.

Lending standards continue to relax, according to data from the OCC’s 2014 Survey of Credit Underwriting Practices. This type of easing is similar to that experienced between 2004 and 2006, the time period leading up to the financial crisis, which many attribute to inadequate lending standards.

Bloomberg reported there are about 15 million more consumers that have credit scores of more than 740 today than back in 2006. What’s more, Bloomberg cited Moody’s as saying there are around 15 million fewer consumers with scores under 660 today then back in 2006.

Renaud Laplanche, Lending Club’s former CEO, is back with a new internet lending startup called Credify Finance Corp. But despite its early status, Credify comes into the market pre-wired for lots of attention — since its founder is both famous and infamous in online lending circles. Department of Justice.

The CFPB also said the median loan amount for first-time homebuying servicemembers with a VA loan increased — as measured in nominal dollars —from $156,000 in 2006 to $212,000 in 2016. The rise showed a slower pace of gains, growing from $130,000 in 2006 to $150,000 in 2016.

Consequently, interagency guidance on CRE concentration risk management , released in 2006, helps institutions pursue CRE lending with safety and soundness. Important to note, though, is that these loans would comprise part of the 300 percent CRE limit set by the 2006 interagency guidance.

This rapid change in interest rates requires careful planning, product selection, and new lending and deposit-gathering strategies. Jun 2004 – Jun 2006. In today’s lending market, borrowers start from historically low interest rates, making the DSCR deterioration much more likely. Higher Rates Due To A Suprised Fed.

These times are different than the early 2000s or even 2006 to 2018 when economic activity was roaring, unemployment was low and financial institution liquidity was tight. CRE Lending. Lending & Credit Risk. CRE Lending. Lending & Credit Risk. CRE Lending. Lending & Credit Risk.

Interestingly, 2014 net income actually matched the pre-recession high set in 2006 – but on $2 trillion more in assets. The growth at smaller banks is led by commercial and industrial (C&I), commercial real estate (CRE) and residential mortgage lending. For example, net income declined 4 percent year over year. percent versus a 3.5

That could create more competition for Ally, which was spun off from GM in 2006 but remains a key lending partner. The automaker is reportedly planning to apply for a bank charter so it could collect deposits and grow its own auto-finance business.

In a recent Sageworks webinar Robert Ashbaugh, senior risk management consultant at Sageworks, discusses High Volatility Commercial Real Estate (HVCRE) lending best practices. How did we get here? Ashbaugh’s presentation begins with a quick summary of why regulators care about HVCRE.

Goldman Sachs Group is giving a $100 million loan to Konfio, marking the first time the lender’s structured finance, investment and lending business has provided a credit facility to a Latin American FinTech. I lived through the subprime crisis,” said Arana, who worked at Deutsche Bank AG in New York from 2006 to 2013. “In

Thriving banks were defined as under $10 billion in assets, and maintained a composite CAMELS 1 rating in each exam cycle from 2006-11, an impressive accomplishment. It appears that banks that had the ability to do the same during the heady lending times of 2004 - 2007 found it to be an enduring strategy (see table from Fed study).

Today, I read an American Banker article on how a multi-billion dollar bank is going to ramp up its business lending. To remind readers, in 2006 the OCC, Federal Reserve, and FDIC issued joint interagency Guidance on Concentrations in Commercial Real Estate Lending. They need a marketing person to title their reports.

In 2006, 44 percent of tappable equity came from homeownerships with credit scores of 780; in 2017, the share had increased to 53 percent. And here is the kicker: “Much of the corresponding decline in share came from homeowners under 45, whose share of equity declined from 24 percent in 2006 to 14 percent in 2017.”.

UK-based lender Zopa pioneered peer-to-peer (P2P) lending in 2005, quickly followed by US contenders Prosper Marketplace and LendingClub in 2006. By December 2014, venture-backed alternative lenders OnDeck Capital and Lending Club had gone public on the NYSE. from investors. FINTECH TRENDS Q3 2017 RESEARCH BRIEFING.

The DOJ investigation centered on whether LendingClub had – between January 2009 to September 2010 – misled its FDIC-insured loan originator, WebBank , leading the bank to underwrite over 200 loans that did not conform to the bank’s lending requirements. lending marketplace. Attorney Alex Tse. “We The Response.

The biggest individual cut will be a Utah office dedicated to lending for medical procedures, but 14 percent of Prosper’s San Francisco- and Phoenix-based workforce is also on its way out the door. Prosper also spent $40 million to acquire medical loan provider American Healthcare Lending LLC and personal finance startup Billguard Inc.

Goldman Sachs said that because it doesn’t have the same legacy costs as many of its competitors, its consumer lending initiative is at an advantage. Discover was the first to make a splash with its cash back bonus back in 2006.”. So we’re not going to win every deal, nor would you want us winning every deal.”.

Before this year, the last time that happened was in 2006, when Walmart made a move on an ILC. Square already has an SMB lending arm – Square Capital – which it operates through a deal with Utah-based Celtic Bank. That lending operation has been fairly successful for Square, and has lent out over $1.8

For example, loans originated in 2006 would show credit stress two to four years later. This specific study considered consumer lending, but we can extrapolate comparable results for commercial portfolios. The pools can be analyzed for delinquencies, payoff trends, losses (typically charge-offs) and profitability.

According to Reuters, Linskens began oversight at Wells Fargo back in 2006 and was responsible for day-to-day supervision of the financial institution. The Office of the Comptroller of the Currency accused Wells Fargo of an “extensive and pervasive pattern” of discriminatory and illegal lending practices for years.

A few days later, one of the founding fathers of FinTech, Renaud Laplanche , was forced out of Lending Club, the peer-to-peer lender he founded in 2006, following scandals over loan disclosures and conflicts of interest. The really interesting, though less juicy, story is what got Lending Club into trouble.

The total amount of debt in Cambodia is now roughly one-third of the country’s GDP — that is compared to markets in Africa like Nigeria or Tanzania, where micro-lending has also picked up a lot of steam in the last few decades, average loan balances are much lower and total indebtedness isn’t a systemic risk to the economy.

We examine the findings from several market reports on small business access to capital, lending, growth and employment. That figure represents a 30 percent increase in borrowing among these SMEs compared to 2010 and a 70 percent increase compared to 2006 figures. billion in loans were taken out by small U.K.

After starting in 2006 as a fashion-specific search platform, it has evolved into what it calls a fashion and lifestyle shopping platform, which is now owned by Rakuten. Although Stiefel doesn’t necessarily like calling it a marketplace, its variety and complexity lend itself well to that concept.

When Renaud Laplanche founded LendingClub 12 years ago in 2006, the lending landscape was a very different place. Most consumer and business lending was done through traditional banks, and to say that peer-to-peer (P2P) or marketplace lending was nascent would be overly generous.

ICBA warns of risks of online marketplace lending models. Online marketplace lenders are a new form of nonbank specialty lending that uses technology platforms to allow Wall Street and individual investors to directly fund loans to consumers and small businesses. Lend exclusively over online peer-to-peer platforms.

The Fed has paused for nearly a year now, and it was our experience in 2006-07 that bank cost of funds continued to increase as the market closed the delta between what someone could earn in a money market mutual fund and a bank account. Such as direct lending funds, and insurance companies. Cost of funds is leveling off now.

The Incredible Shrinking Non-Bank Mortgage Lending Market. In 2006, for example, there were three straight quarters during which borrowers withdrew more than $80 billion from their homes. Interest rates on 30-year fixed-rate mortgages dropped in the third week of November, down 13 basis points to 4.81

The Bureau analyzed servicemember first-time homebuyer data over a ten-year period from 2006-2016. The Bureau concluded that veterans who took the survey reported higher levels of financial well-being than the average U.S. VA-Home Loans. Educational Activities and Coordination with Other Federal and State Government Agencies.

Most concerning has been the safety-and-soundness regulation’s unnecessary effect on reducing certain lending by community banks, say Kendrick and several community bankers. In 2006, before Basel III and the financial crisis that precipitated it, the call report instructions were about 45 pages long. Headwind for lending.

According to “the father of mPesa,” Michael Joseph , when the idea first appeared on his desk in 2006, M-Pesa was really about something quite different than what it has since grown into — originally it was designed for the microfinance industry for the disbursement and repayment of microfinance loans.

PYMNTS researchers also point to wine prices — shown through BLS data — which have increased drastically, by about 56 percent, from 2006 until this year. While that was, of course, for the entire year, even lending a small portion of that to the Thanksgiving holiday is higher now than it was 50 years ago.

While the economy has recovered from the great recession, lending still lags the “heyday” of 2005. First, I looked at FICO® Score 8 scorable rates and average score by age group to see if either would explain today’s lending lag. balances generally increase). Taken overall, it isn’t an encouraging picture.

If this were 2006, things would be good. Retiree: That's Not So Funny To the retiree that prefers the safe haven of FDIC insured deposits held at the local bank that lends it out locally, this is a serious issue. You've been conservative, preferring the stability and security of bank deposits versus the gyrations of the market.

It is well below that of 2006, when that same figure hit 558,000 – and still trailing the 500K-600K that was the average in the U.S In 2015, 414,000 new businesses were formed in the latest year surveyed, according to the Census. The good news? That is slightly more than the previous year. The bad news?

We previously wrote about the first investigative report in this series, which was titled “ Unsafe at Any Bureaucracy: CFPB Junk Science and Indirect Auto Lending.” The latest report discusses two subjects. The Auto Finance Larger Participant Rule.

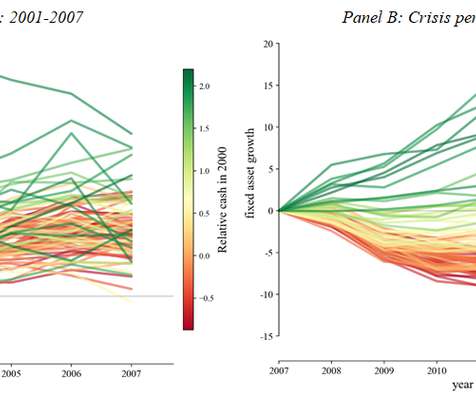

Figure 1: Variations in cash holdings by industry (2006). Cash holdings are defined as deposits over total assets and measured in 2006. We now repeat this exercise, but measure cash in 2006 instead. During a financial crisis banks are more likely to cut lending to young and small firms. Well, does this matter?

The two companies already have a payments partnership, one that involves Walmart MoneyCard program and which launched in 2006. That would seem to bolster the case for this Walmart-Green Dot joint accelerator — and lend credence to how Eckert described the possible coming attractions from that operation.

There is ample evidence that a monetary policy tightening triggers a decline in consumer price inflation and a simultaneous contraction in investment and consumption (eg Erceg and Levin (2006) and Monacelli (2009) ). Since banks are highly leveraged, the decline in bank equity exacerbates the reduction in lending to the real economy.

The bank was founded in 2006 and operates 19 full-service branch locations in multi-ethnic communities in Alabama, Florida, Georgia, New York, New Jersey, Texas and Virginia. and equipment lending and asset based lending through Triumph Commercial Finance. Crypto is blazing hot! #2. MetroCity Bankshares, Inc.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content