This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As banks are increasingly playing a bigger role in commercial real estate lending, it is more important than ever to ensure proper riskmanagement practices. Due to the volatility of CRE concentrations at banks, regulators have released supervisory guidance to ensure sound riskmanagement practices.

In a recent Sageworks webinar Robert Ashbaugh, senior riskmanagement consultant at Sageworks, discusses High Volatility Commercial Real Estate (HVCRE) lending best practices. How did we get here? Ashbaugh’s presentation begins with a quick summary of why regulators care about HVCRE.

Consequently, interagency guidance on CRE concentration riskmanagement , released in 2006, helps institutions pursue CRE lending with safety and soundness. Important to note, though, is that these loans would comprise part of the 300 percent CRE limit set by the 2006 interagency guidance. Blog Bank Credit Union'

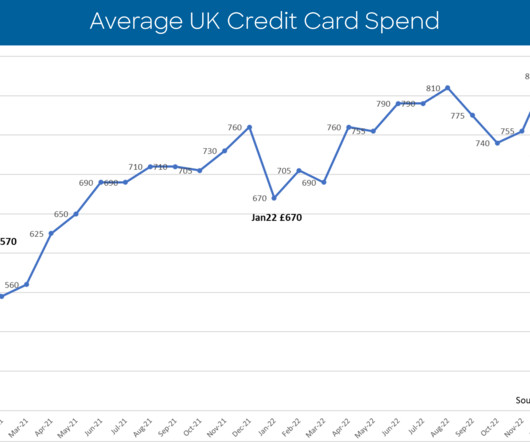

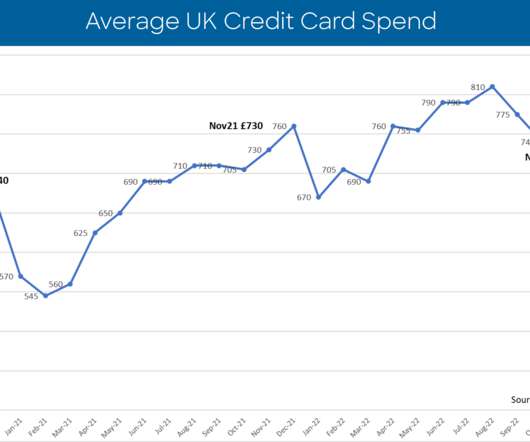

But this year’s rise seems to also have been driven by inflation, pushing the amount of average credit card spend in the UK to the highest level since our UK Risk Benchmarking records began in 2006. This rise occurred in a month when UK retail sales volumes were widely reported as being down relative to past years.

These times are different than the early 2000s or even 2006 to 2018 when economic activity was roaring, unemployment was low and financial institution liquidity was tight. That is an overall asset/liability management decision that requires more time and attention, so stay tuned for that. Credit RiskManagement.

The first tweet ever written was by co-founder Jack Dorsey on March 21, 2006, at 9:50 p.m., In fact, the FFIEC even released guidance in December 2013 on social media, entitled “Social Media: Consumer Compliance RiskManagement Guidance.” A status update on banks and social media. By Russ Horn, CoNetrix. Following the tweets.

Property managers also used an incredibly archaic system that made it difficult to deal with rent, security deposits and payment collections. This is exactly where YapStone identified the opportunity to solve a real problem for property management companies and build long-term relationships. eventually become commoditized.”.

From user interface technology to security and riskmanagement, the only constant in the financial space is that nothing stays the same for long. For example, we were the first in the Middle East region in 2006 to close the loop by sending back a text alert to the remitter that the beneficiary had collected the money.

By using funds managed by LCA to benefit its parent company, LCA and Laplanche failed to do so.”. We have full confidence in our new management team and we are a better company today.”. When LendingClub entered the market in 2006, Laplanche had one idea in mind: disrupt the banks. The Rundown on the Run-up to the Decisions.

By better modelling how this relationship might raise insurers’ capital risk we can more firmly argue that insurers’ model assumptions should account for key dependencies between perils. In panel (a) the historically observed losses (2006–18) on Great Britain’s rail network are used as a sense-check on the climate projection results.

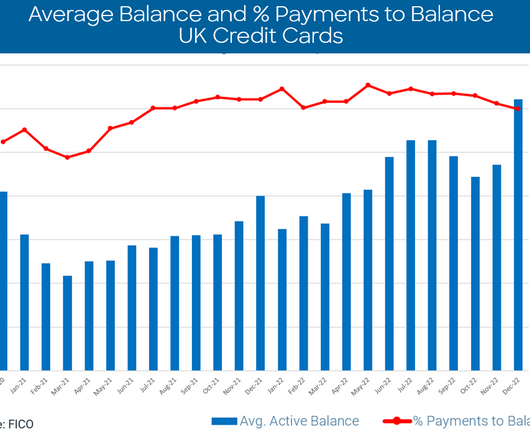

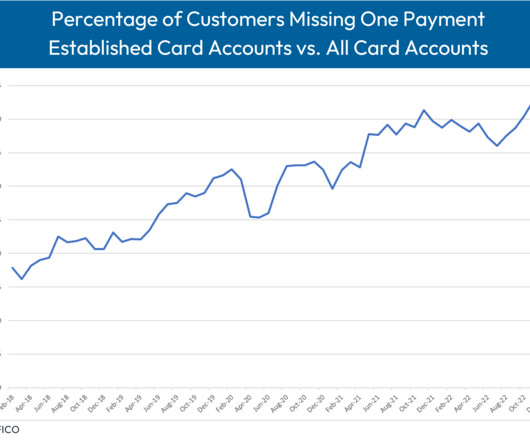

In comparison, the average Established cards balances at risk was 47 percent higher than all vintages in 2018. All of these trends will be of concern to riskmanagers. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80 percent of UK card issuers.

In the past decade, we have seen several Treasury routs that resulted in huge selling in the markets, most notably in 2003-2004, 2005-2006, and 2009. DJ 07/03/13 Dorothy Jaworski has worked at large and small banks for over 30 years; much of that time has been spent in investment portfolio management, riskmanagement, and financial analysis.

These tools are generally aimed at riskmanagement : reducing the overall level of tail risk, rather than simply stabilising the economy during normal times. Introduction to GDP-at-Risk. Notes: Dots show estimates of two year ahead GDP-at-Risk. Green line shows estimate from domestic-only model from 2006 Q4.

The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80 percent of UK card issuers. Liz also works on a range of projects including customer management software implementations and upgrades, current state assessments and delivery of data-driven strategies.

According to Intel , the “breathtaking” rate of growth in the IoT could result in it encompassing 200 billion objects by 2020, compared to two billion in 2006. million in 2016 to US$38.8 billion by 2025.

I recently spoke at a Financial Managers' Society (FMS) breakfast meeting on this subject and thought I would share my comments with you. In 2006, when the median asset size within my firm's profitability outsourcing service was $696 million, the operating cost per business checking account was $586 per year.

To remind readers, in 2006 the OCC, Federal Reserve, and FDIC issued joint interagency Guidance on Concentrations in Commercial Real Estate Lending. Construction concentration criteria : Loans for construction, land, and land development (CLD) represent 100% or more of a banking institution's total risk-based capital.

The bad news is the first review, conducted from 2004 to 2006, was a bust. The bankers serving on the council are these: Angela Beilke , vice president, mortgage department at American Bank & Trust in Davenport, Iowa; Michael Gallagher , senior vice president, riskmanagement director at Enterprise Bank & Trust Co.

Unsurprisingly, the largest declines occurred starting monthly in March, 2006 and on a y-o-y basis in September, 2006 and continued to November, 2009. We all remember the Great Recession, which began in 2007, but the LEI knew it as early as March, 2006. The largest monthly decline took place in May, 2009 at -27.2%

We have many examples, notably 2000-2001, 2006-2008, and 2019, when restrictive rates impaired growth and recession followed. DLJ 06/30/24 Dorothy Jaworski has worked at large and small banks for over 30 years; much of that time has been spent in investment portfolio management, riskmanagement, and financial analysis.

FICO’s latest market report of UK card trends suggests that consumers managed their credit card debt to keep lines of credit open for the festive season as spend increased month on month. percent Clearly, November was a mixed story when it came to credit card spend and debt management. percent Year-on-year there were 14.8

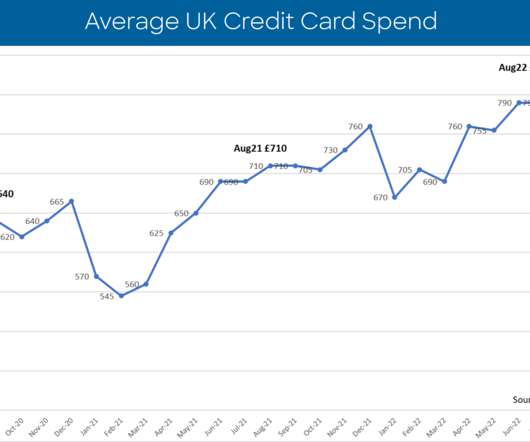

FICO’s report of UK card risk trends for summer 2022 (June-August) paints a picture of inconsistent consumer behaviour and market patterns which will be challenging for lenders to manage as the cost-of-living crisis impacts financial spending and consumer finances. How FICO Can Help You Manage Credit Card Risk and Performance.

For the first time since we’ve been tracking these stats, the average national FICO Score reached the 700 threshold — some 10 points above what it was just prior to the recession in October 2006.”. Using Alternative Data in Credit Risk Modelling. Read the full post. Millennials and Credit: Are We Missing the Real Story?

After easing and keeping rates low for three years, the Fed began tightening from June, 2004 to June, 2006. In my career, I’ve lived through many years of the Fed raising interest rates and it’s my experience that they usually tighten too much and keep rates high for too long, just like in 2001 and 2006-2007. Life is good!

percent year-on-year Consumer Duty Guidance Deadline Nears The yo-yo pattern of financial management — seen for the last few months — reflects the general economic uncertainty, particularly for mortgage holders. percent in March and 8.7 percent in April. However, year-on-year they are still significantly higher - by 20.2 percent and 9.4

We have a long way to go before recapturing the home price highs of 2006 and 2007, but it is a start. The stock markets rejoiced and rallied 2% to 3% on January 2nd, because the fiscal cliff was now manageable, not an apocalypse. Stay tuned! Thanks for reading.

Historically, the nine day streak is only the second of its kind since a similar streak in 1974—the other being during June, 2006. DJ 03/27/12 Dorothy Jaworski has worked at large and small banks for over 30 years; much of that time has been spent in investment portfolio management, riskmanagement, and financial analysis.

It has been nine years since the Fed last tightened policy in June, 2006; maybe they are getting anxious. 03/30/15 Dorothy Jaworski has worked at large and small banks for over 30 years; much of that time has been spent in investment portfolio management, riskmanagement, and financial analysis. Stay tuned!

bank failures per year between 1996 and 2006, and 3.6 To you, manage your interest rate risk. Before becoming desperate and trading interest rate risk for credit risk. In 2006, the then $686 million in asset bank made $8.8 Between 1941 and 1979, an average of 5.3 banks failed a year. between 2015 and 2022.

Both spread inversions precede recession by 13 months (as in 2000 for the 2001 recession) to 26 months (as in 2006 for the 2008-2009 recession). DJ 07/16/19 Dorothy Jaworski has worked at large and small banks for over 30 years; much of that time has been spent in investment portfolio management, riskmanagement, and financial analysis.

Valentine’s Day on 14th February every year to commemorate the introduction of chip and UK In the UK on 14th February 2006. 2017 will see the emergence of the next generation of innovation in fintech that addresses riskmanagement and regulation for the bank. EMV is getting long in the tooth and needs to be refreshed.

Carranza has a history at the SBA, serving as its deputy administrator between 2006 and 2009. . “Jovita was a great Treasurer of the United States, and I look forward to her joining my Cabinet!” ” said Trump in a tweet announcing the nomination, according to Reuters. Last year, the U.S.

Carranza was the SBA deputy administrator from 2006 to 2009. Senate passed a bill broadening the SBA’s authority over its Small Business 7(a) loan program, which would strengthen its credit riskmanagement office, enhance the SBA’s oversight of lenders and enable full-risk analysis of its small business loan program.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content