This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Ken Finley, president of Johnson City Bank, in downtown Johnson City with Shannon Sultemeier, executive vice president (left); and Brenda Haynes, vice president/cashier (right). Here’s how four communitybanks are thriving in this environment. These include family-owned businesses, community businesses and operating companies.

The latest FDIC Quarterly Banking Profile was just released and the industry continues to be led by the nation’s communitybanks. percent of communitybanks were unprofitable during the quarter. However, across all banks, fourth quarter net income fell by 7.9 Communitybank loan balances also rose 2.5

The latest FDIC Quarterly Banking Profile was just released and the industry continues to be led by the nation’s communitybanks. percent of communitybanks were unprofitable during the quarter. However, across all banks, fourth quarter net income fell by 7.9 Communitybank loan balances also rose 2.5

Premium benefits packages, professional development and TLC during the pandemic—this year’s winners do everything in their power to keep their community bankers happy and fulfilled. We asked both leaders and staffers to tell us what makes their communitybanks stand out as employers. Key CommunityBank: Leading by example.

The banking industry has seen a steady stream of media attention since 2008, much of it in the form of stories about data breaches linked to major retailers or mega banks’ profits. Risk management issues were also a high-ranking hurdle to growing banks, with 26 percent calling it a concern for 2015.

In June of 2008 I gave a speech titled "The Death of the CommunityBank" and in that speech I made predictions. Prediction: The General Bank will become extinct. Much like competitors nip at communitybanks' customers. Eighteen percent of that group opened an account at a digital bank. Result: Mixed.

smaller communitybanks and credit unions (CUs) stepped up to the plate and, according to the Small Business Association (SBA), ended up facilitating more than half of PPP loan volume to SMBs. That's good news for communitybanks and credit unions, which could see a wave of new SMB customers and members in the coming months.

Community financial institution (FI) Cross River Bank is acquiring Seed , a small business (SMB) digital banking company, reports in Reuters said on Monday (June 24). Cross River Bank has partnered with a range of FinTech startups since its 2008 launch, including collaborations with Stripe , Coinbase and Affirm , reports said.

Derek Williams, president and CEO of Century Bank & Trust in Milledgeville, Ga., wanted to be a financier before finding his way to communitybanking. I went to work for a communitybank, kind of by accident, and found the job love of my life,” he says. “I That love of community has defined his career.

Chamber of Commerce is voicing its support for legislation that would ease regulatory burdens for the nation’s communitybanks in an effort to improve access to funding for small business borrowers. According to reports, the Senate is expected to pass the legislation this week.

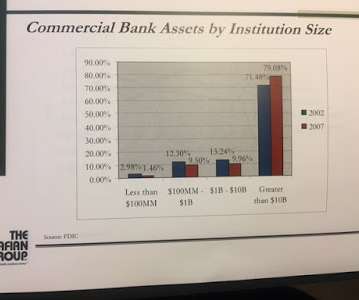

CRE Risk Background While ten years ago, community and regional banks use to make up some 55% of the CRE market, in 2023, these banks now compose approximately 72% (below). The risk here is that communitybanks continue to take on an above-average amount of CRE credit exposure.

Working through any difficulty or crisis at your communitybank won’t be a walk in the park, but it may lead to an experience for which you’re truly grateful. As a community banker, you’re either going through a crisis or you’re preparing for one. Is there education or training at ICBA Community Banker University that can help?

While we will cover the general lessons HERE , in this article, we wanted to focus on the root cause – how and why interest rate risk caused the second-largest bank failure in US history (Washington Mutual was the largest in 2008). Notably, most communitybanks’ duration risk is in the loan portfolio.

I was at a strategic planning retreat a few weeks back where a colleague lauded the concept of bankers getting back to plain vanilla communitybanking. But if you read or watch interviews of CEOs of community FIs from 2008 forward, you will be bombarded with the message that they didn''t engage in the things that led to the collapse.

Banks had enough liquidity so it didn’t really matter in terms of day-to-day operations. Without liquidity, finance companies and investment banks had to draw on their lines. By 2008, there were a variety of failures as a result of liquidity – Bear Sterns, Lehman Brothers, and more. Capital got scarce.

Its predecessor, RegalPay, has been available since 2008, connecting to more than 160 enterprise resource planning (ERP) systems. To streamline B2B payments, MineralTree company Regal Software unveiled its RegalPay One offering in a Wednesday (Oct. 14) announcement.

This article provides an update on pricing trends driven by our Loan Command aggregated communitybank data and highlights some working pricing ideas. Regarding loan growth, lending continues to be at the slowest pace since 2008. Total industry loans grew 5.1% for the year compared to last year.

Bank failures increased dramatically in the last financial crisis, rising from 25 in 2008 to 140 in 2009. Resolute Bank in Maumee, Ohio closed on Oct. 25 and was assumed by Buckeye State Bank in Powell, Ohio. Louisa CommunityBank of Louisa, Kentucky also shuttered on Oct. It had one branch with $27.1

Last year, communitybank loan producers were faced with both record-low interest rates and a glut of deposits. But as they always do, they came through for individuals and businesses in their communities with a combination of personalized service and prudent risk management practices. American Bank, National Association.

Earlier this month, the FASB considered and rejected further deferral of the CECL standard, initially issued in 2016 in response to the 2008 global financial crisis. The decision appears to mark the board’s final word on ongoing petitions from communitybanks and credit unions who asked for a delay or total exemption.

We cannot afford to repeat the mistakes that contributed to the 2008 financial catastrophe, which community bankers remember all too well. Every time you think of something that makes your bank unique, whether it’s going one step further to make a loan happen or making a decision that will shore up your capital position, write it down.

While federal regulators only require this small number of banks to be subject to these particular stress tests, as outlined in the Dodd-Frank Act following the economic crisis of 2008, stress testing is becoming a critical part of financial institutions’ risk management strategies, regardless of their asset sizes.

The combination of RTP and FedNow will allow providers, such as correspondent banks, to offer both rails to provide a more expansive network reach and redundancy. Communitybank customers will only have to agree to an irrevocable instant payment, and payment providers will route the payment to the fastest, cheapest, and most stable network.

The vast majority of United States senators have penned a letter urging the CFPB to let communitybanks and credit unions live free from additional regulations. “We request that the CFPB carefully tailor its regulations to match the unique nature of communitybanks and credit unions,” the letter stated.

“… it’s not 2008.”. NCUA seems to have forgotten that it's not 2008, but, instead, 2015 and that the credit union community — in NCUA's own assessment — is strong and resilient,” McWatters said in the Credit Union Journal. The longer interval is on the table for banks as well.

It's what we did in 2008-10. I delivered this talk on a recent bank trade association webinar. Unlike 2008, banks were not the bane of our problems. In 2008, we were in the eye of the storm. Sure, communitybanks had little to do with liar loans or what was otherwise termed sub-prime. Capital aplenty.

It is of interest to note that many may be considered smaller, communitybanks. Live Oak Bank. Take, for example, Live Oak Bank in Wilmington, NC, which has the top spot on the list. According to American Banker, perks on the bank’s campus include a gym, dog park and catered lunches every Friday.

People facing charges include former communitybank manager Carrie Tolstedt, former chief administrative officer Hope Hardison and former chief auditor David Julian, the sources told Bloomberg. The incident was among the biggest scandals in the banking industry since the 2008 crisis.

SMBs since the 2008 financial recession. percent decline in shares at large banks , coinciding with a 7.8 percent increase in shares at mid-cap regional banks and a 12.1 percent share increase for communitybanks, suggest that large FIs are losing out to smaller competitors, per CNBC reports last week.

What this has to do with communitybank investment management may not be readily apparent. The S&P 500 Index dropped 12.4%, which was the worst monthly stock performance since 2008. Belly of the curve matters to communitybanks. In fact, the tone is about to improve. More often, the two operate independently.

15, 2008 fall of Lehman, which filed for bankruptcy that day. The traditional banking model may be disrupted, or about to be disrupted, depending on where you look. Outstanding credit card debt is at the second highest point seen since the end of 2008, and total outstanding debt stands at $1 trillion. trillion this year.

Army Infantry Platoon leader who became a communitybanking manager. It’s no different in communitybanking. When I returned home from the deployment, the support I had from my community was clear—the same way Think Mutual Bank supports its local community. By Jeff Sabatke. It was 1 a.m. Paul, Minn.,

For the largest of American financial institutions – those that much of the public banks with for checking, mortgages and auto loans – stress testing regulations have been passed and executed to avoid a repeat of 2008. California is also a healthy state for banking – with 15 of 20 banks on the Western list in the Golden State.

“It’s going to be easier for banks to serve their customers, clients and communities — that’s what’s most important.”. Deregulations for smaller banks and credit unions could theoretically lead to more innovation — a topic that was the focus of the latest PYMNTS Innovation Readiness Playbook.

The CARES Act extended the CECL implementation deadline for many larger communitybanks until the end of the COVID-19 pandemic. Community bankers tell us that while the extension is welcome, they’re already down the road to implementation. ICBA tells FASB CECL isn’t feasible for communitybanks. By Stephanie Vozza.

launched its own Faster Payments Service in 2008. Communitybanks and credit unions also offered their backing. They stated that major banks have too much control over the RTP system and that they regarded the Fed as a compelling and more equitable alternative to achieving payments ubiquity. billion in 2018 to $26.9

The Dodd-Frank Wall Street and Consumer Protection Act was supposed to prevent another 2008banking meltdown — and solve the problem of “too big to fail.” banks have disappeared. And those banks are going out of business — or merging with bigger players — largely due to the complexity and cost of compliance.

Communitybanks are doing very well, thank you very much, Mr. Dimon. But it's not necessarily a return to the salad days of pre-2008. The Wall Street Journal's ongoing series on the banking industry looks at the state of communitybanking, and pronounces the sector healthy, but facing serious issues. …

Section 4012 – Temporary Relief For CommunityBanks. Section 4012 of the CARES Act provides temporary relief to financial institutions that elected to be subject to the CommunityBank Leverage Ratio pursuant to the Economic Growth, Regulatory Relief, and Consumer Protection Act (EGRRCPA).

Sarah Huckabee Sanders, the White House press secretary, was pleased with the result: “The bill provides much-needed relief from the Dodd-Frank Act for thousands of communitybanks and credit unions and will spur lending and economic growth without creating risks to the financial system,” she said.

Community bankers offer real-world reasons for more Basel III relief. Nearly one year after the Basel III capital rules went into effect, community bankers say that now recognize just how much more complex and how much more difficult this new set of capital rules will make life and business for them if they remain in place.

A New Accounting Twist—ICBA’s accounting expert James Kendrick tells communitybanks to closely watch for the Financial Accounting Standards Board’s pending new standards for recognizing credit losses, much earlier than currently required. Under the FASB plan, banks would instead take a hit the moment they make a loan.

The financial services market has progressed by leaps and bounds in terms of innovation, from the rise of alternative finance to the development of technologies like blockchain and open banking initiatives. Meanwhile, bank lending to small businesses dropped by nearly $100 billion during that time.

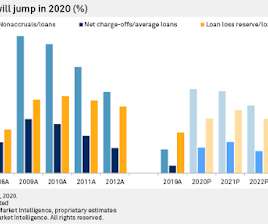

Key Takeaways This recession is significantly different than the 2008 financial crisis, creating a unique credit environment for financial institutions. Now, banks and credit unions must determine how to safely and effectively manage risk in the portfolio while also driving growth at their institution.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content