This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

smaller community banks and credit unions (CUs) stepped up to the plate and, according to the Small Business Association (SBA), ended up facilitating more than half of PPP loan volume to SMBs. That's good news for community banks and credit unions, which could see a wave of new SMB customers and members in the coming months.

Ready to catch the next wave of lending growth? Commercial and industrial lending (C&I) will be the next big performance driver for banks and credit unions. You might also like this paper on how institutions can produce smarter, faster lending. C&I lending will be the next “bomb.”

Here’s how four community banks are thriving in this environment. Clearly, community banks in the region have plenty of opportunities to do what they do best: forge deep and lasting relationships with their customers and communities. These include family-owned businesses, community businesses and operating companies.

The banking industry has seen a steady stream of media attention since 2008, much of it in the form of stories about data breaches linked to major retailers or mega banks’ profits. Two recent surveys addressing the community banking landscape have pointed to increasing regulations as the primary cause of stress for these institutions.

The relaxing of the limits has let families, businesses and communities stay afloat fiscally as the virus forces normal courses of money, like most businesses and restaurants, to close down for fear of spreading infectious germs or catching them.

From leveraging PPP technology to building relationships, reasons for boosting SBA lending are numerous. . Takeaway 1 SBA lending can expand your product offerings to help win deals with prospects and existing business customers or members. Why SBA Lending? Would you like others articles like this in your inbox? 1 and Sept.

wanted to be a financier before finding his way to community banking. Photo by Harold Daniels Derek Williams, president and CEO of Century Bank & Trust in Georgia, is bringing his passion for community banking to his term as ICBA chairman for 2023/24. That love of community has defined his career.

And in lending, with the financial crisis in the rearview mirror, a decade on, invention – okay, innovation – has become a hallmark, at least in some corners. 15, 2008 fall of Lehman, which filed for bankruptcy that day. But a standstill in the credit markets created a vacuum for a bit, at least along traditional lending conduits.

Premium benefits packages, professional development and TLC during the pandemic—this year’s winners do everything in their power to keep their community bankers happy and fulfilled. We asked both leaders and staffers to tell us what makes their community banks stand out as employers. Key Community Bank: Leading by example.

Effective stress testing can benefit many different facets of lending, from risk management and strategic decision-making to capital adequacy and liquidity management. However, the lack of prescriptive guidance on how to effectively stress the loan portfolio has created challenges for some community financial institutions. Learn More.

The global financial crisis in 2008 was, in many ways, a catalyst to this innovation, especially in the area of small business (SMB) finance, as banks pulled their services away from SMBs and FinTechs stepped in to offer another option. author of the report and Florida Atlantic University’s Kaye Family Endowed Professor in Finance.

Working through any difficulty or crisis at your community bank won’t be a walk in the park, but it may lead to an experience for which you’re truly grateful. As a community banker, you’re either going through a crisis or you’re preparing for one. Is there education or training at ICBA Community Banker University that can help?

India-based financial services provider Reliance Capital has announced it will exit the lending market. 30), Reuters reported , noting that the company is struggling to overcome “collateral damage” resulting from a slowing national economic and a broader “crisis,” the publication said, in India’s lending sector.

CRE Risk Background While ten years ago, community and regional banks use to make up some 55% of the CRE market, in 2023, these banks now compose approximately 72% (below). The risk here is that community banks continue to take on an above-average amount of CRE credit exposure. This article explores the risk and what to do about it.

Find commercial real estate risks in the loan portfolio Sound risk management practices in commercial real estate lending help lenders manage CRE credit losses and protect the portfolio's profitability. For example, during the 2008 Subprime Mortgage Crisis, commercial real estate prices fell drastically by 30 percent year over year.

This article provides an update on pricing trends driven by our Loan Command aggregated community bank data and highlights some working pricing ideas. Regarding loan growth, lending continues to be at the slowest pace since 2008. Total industry loans grew 5.1% for the year compared to last year.

In recent years, banks have even seen greater competition in the lending market from new FinTech players that can quickly approve loan applications and distribute funds to lenders. Some of the more prominent names in the marketplaces lending space include OnDeck, Kabbage and Orion First. New tools for new FinTechs.

From leveraging PPP technology to building relationships, reasons for boosting SBA lending are numerous. . Takeaway 2 Far fewer financial institutions regularly participate in SBA (7a) lending than the more than 5,000 that joined the PPP. . Why SBA Lending? Want other articles like this on SBA loan origination in your inbox?

In 2020, we will likely see financial institutions putting more emphasis on automating time-consuming, manual processes that bog down lending decisions. By automating these mundane, laborious tasks, lenders and credit analysts are then able to focus their time on the borrower or member and make faster, more efficient lending decisions.

While we will cover the general lessons HERE , in this article, we wanted to focus on the root cause – how and why interest rate risk caused the second-largest bank failure in US history (Washington Mutual was the largest in 2008). Notably, most community banks’ duration risk is in the loan portfolio.

Last year, community bank loan producers were faced with both record-low interest rates and a glut of deposits. But as they always do, they came through for individuals and businesses in their communities with a combination of personalized service and prudent risk management practices. Ag lending in the South: Relationships matter.

The 2008 financial crisis exposed significant weaknesses of relying on incurred losses. CRE Lending. Lending & Credit Risk. SBA Lending. How the Pandemic and PPP Have ‘Turbo-charged’ New Business Lending Strategies. CRE Lending. Lending & Credit Risk. CRE Lending. C&I Loans.

Biz2Credit’s latest Small Business Lending Index found that loan approval rates at alternative lenders stagnated – and at credit unions, they actually fell. SMBs since the 2008 financial recession. percent, while community banks ‘ portfolios grew 14.7 But the story doesn’t end there. percent a month prior.

I was at a strategic planning retreat a few weeks back where a colleague lauded the concept of bankers getting back to plain vanilla community banking. But if you read or watch interviews of CEOs of community FIs from 2008 forward, you will be bombarded with the message that they didn''t engage in the things that led to the collapse.

While federal regulators only require this small number of banks to be subject to these particular stress tests, as outlined in the Dodd-Frank Act following the economic crisis of 2008, stress testing is becoming a critical part of financial institutions’ risk management strategies, regardless of their asset sizes.

Historic collapse SVB is different from other financial institutions The FDIC closure and assumption of Silicon Valley Bank (SVB) – the largest bank failure since 2008 – is a stark reminder that when a crisis occurs, it can spread as fast as a wildfire in dry fields with a strong wind. Do you get that from your deposit analysis ?

As originally showcased in a 2012 Channel 4 series, it is the true story of how self-made Burnley businessman Dave Fishwick took on London’s elite banking institutions to get a licence to open his own bank serving the local community.

Key Takeaways This recession is significantly different than the 2008 financial crisis, creating a unique credit environment for financial institutions. This recession is significantly different than the 2008 financial crisis, creating a unique credit environment for financial institutions. Learn More. Portfolio Risk & CECL.

When the Small Business Borrowers’ Bill of Rights was developed in 2015, it appeared as if alternative SME lenders were collectively taking a stance against predatory lending practices in an effort to protect small businesses. “Bank lending has still not recovered from 2008. Loan sizes have gone up.”.

keep me informed watch SVB: Early lessons for all financial institutions from Silicon Valley Bank’s failure The FDIC closure and assumption of Silicon Valley Bank (SVB) – the largest bank failure since 2008 – is a stark reminder that when a crisis occurs, it can spread as fast as a wildfire in dry fields with a strong wind.

Though small businesses have suffered from a gap in financing availability post-2008, the demographic continues to shape the financial markets. One of these lenders, Clearinghouse Community Development Financial Institution , better known as Clearinghouse CDFI, offers an interesting view into the state of SME finance. A Regional Reach.

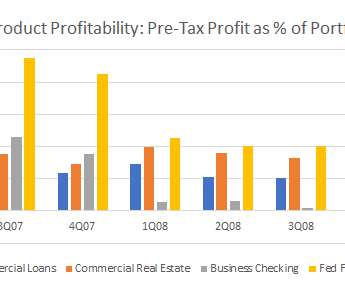

Me: Commercial Real Estate loans are the most profitable product in a community bank's arsenal and have been through various interest rate environments. By the time the FF hit zero at the end of 2008, CRE was the last product standing. Bank Senior Lender: Not when you consider the whole relationship. But we have work to do.

CPAs [(certified public accountants)] play a key role in the small business community as trusted business advisors,” said AICPA Vice President of Small Firm Interests Carl Peterson in a statement. The SBA and AICPA have been working together since 2008, the entities noted.

For the largest of American financial institutions – those that much of the public banks with for checking, mortgages and auto loans – stress testing regulations have been passed and executed to avoid a repeat of 2008. California is also a healthy state for banking – with 15 of 20 banks on the Western list in the Golden State.

The Dodd-Frank Wall Street and Consumer Protection Act was supposed to prevent another 2008 banking meltdown — and solve the problem of “too big to fail.” Louis Fed estimated that community banks pay an estimated $4.5 Since the passage of Dodd-Frank, over 1,700 U.S. banks have disappeared. billion annually in compliance costs.

The program, created in response to the 2008 financial crisis, generated $19 billion in small-business loans. It could be used as a viable path out of the coronavirus pandemic.

The alternative finance boom post-2008 financial crisis undoubtedly provided more options for small business (SMB) borrowers, but that doesn’t mean the industry is guaranteed to become a staple among entrepreneurs seeking financing.

While troubling factors such as higher risk profiles may be behind the recent lending boom, the industry could also just be returning to the historical average for loan growth following the "Great Panic" of 2008-2010.

There are a lot of retailers that are now looking to their local community to effectively prepay through gift cards to sustain themselves in the short term,” he said. They have strong balance sheets and the ability to lean in and lend, which is very important.”.

At recent Abrigo CECL Kickstart webinars, consultants demonstrated CECL implementation practices with an emphasis on the needs of community banks and credit unions. What if our lending footprint is very small and not affected by macroeconomic factors such as unemployment? Reasonable, defensible, data-based CECL models.

But researchers found troubling patterns in the ways SMEs access the capital they need, and it goes beyond issues of complicated lending processes or distrust of a bank. And the statistics, Wesleyan said, suggest that small businesses have gotten used to a lack of traditional bank funding following the 2008 financial crisis.

Section 4011 – Temporary Lending Limit Waiver. Section 4012 – Temporary Relief For Community Banks. Pursuant to the EGRRCPA, Bank regulators had announced the Community Bank Leverage Ratio at 9% of Total Assets. This section provides that Section 131 of the Emergency Economic Stabilization Act of 2008 (12 U.S.C.

Today, Australian FIs are facing increased pressure from regulators, especially when it comes to small business banking and lending. In May, the nation’s Big Four lenders offered testimony as part of a Royal Commission inquiry into small business banking, and all four admitted to wrongdoings related to their SMB lending practices.

Although there were early inklings of the technology dating back to 1991, it wasn’t until 2008 when Satoshi Nakamoto implemented it as the base component of bitcoin currency that it really took off. IBM and Sovrin have contributed the Hyperledger software and infrastructure to the open source community.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content