This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Find commercial real estate risks in the loan portfolio Sound risk management practices in commercial real estate lending help lenders manage CRE credit losses and protect the portfolio's profitability. LISTEN Takeaway 1 Effective CRE risk management involves adapting to changing market fundamentals to avoid excessive loan losses.

While we will cover the general lessons HERE , in this article, we wanted to focus on the root cause – how and why interest rate risk caused the second-largest bank failure in US history (Washington Mutual was the largest in 2008). Notably, most community banks’ duration risk is in the loan portfolio.

Here’s how four community banks are thriving in this environment. Clearly, community banks in the region have plenty of opportunities to do what they do best: forge deep and lasting relationships with their customers and communities. These include family-owned businesses, community businesses and operating companies.

Premium benefits packages, professional development and TLC during the pandemic—this year’s winners do everything in their power to keep their community bankers happy and fulfilled. We asked both leaders and staffers to tell us what makes their community banks stand out as employers. Key Community Bank: Leading by example.

Key Takeaways This recession is significantly different than the 2008 financial crisis, creating a unique credit environment for financial institutions. Now, banks and credit unions must determine how to safely and effectively manage risk in the portfolio while also driving growth at their institution.

In June of 2008 I gave a speech titled "The Death of the Community Bank" and in that speech I made predictions. Much like competitors nip at community banks' customers. Two percent opened an account at a community bank. And I had ING Direct as an example of who might be the lightkeeper's cat to the community bank.

The banking industry has seen a steady stream of media attention since 2008, much of it in the form of stories about data breaches linked to major retailers or mega banks’ profits. Two recent surveys addressing the community banking landscape have pointed to increasing regulations as the primary cause of stress for these institutions.

Community financial institution (FI) Cross River Bank is acquiring Seed , a small business (SMB) digital banking company, reports in Reuters said on Monday (June 24). Cross River Bank has partnered with a range of FinTech startups since its 2008 launch, including collaborations with Stripe , Coinbase and Affirm , reports said.

Working through any difficulty or crisis at your community bank won’t be a walk in the park, but it may lead to an experience for which you’re truly grateful. As a community banker, you’re either going through a crisis or you’re preparing for one. Manage loan portfolio relationships proactively after the loan is funded.

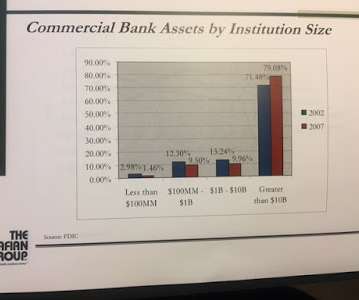

CRE Risk Background While ten years ago, community and regional banks use to make up some 55% of the CRE market, in 2023, these banks now compose approximately 72% (below). The risk here is that community banks continue to take on an above-average amount of CRE credit exposure. This article explores the risk and what to do about it.

Community bank customers will only have to agree to an irrevocable instant payment, and payment providers will route the payment to the fastest, cheapest, and most stable network. Machine learning financial management tools become more meaningful with increased payment data contained in the messages. Payroll can move to daily payment.

Not if you trust various Industry experts who predict that half of all board and senior management positions will turn over to fresh facesby the end of 2025. They communicate the reasons and rationale behind tough decisions to build trust. Everyone Ive met at Mikes bank focuses on mattering to customer, community and one another.

As with the 2008 market crash, the coronavirus has brought the issue of exposure management to prominence once again. Recent market volatility has sent shockwaves through the financial community and resurfaced some dark memories that most of us would prefer to forget. When the markets are.

While federal regulators only require this small number of banks to be subject to these particular stress tests, as outlined in the Dodd-Frank Act following the economic crisis of 2008, stress testing is becoming a critical part of financial institutions’ risk management strategies, regardless of their asset sizes.

Stress Testing | 7 minute read Key Takeaways Stress testing is an important component of sound risk management. Effective stress testing can benefit many different facets of lending, from risk management and strategic decision-making to capital adequacy and liquidity management. Stress testing and risk management.

Takeaway 2 Management reports, probability of default, and model validation topics were found in the top blogs for risk professionals. Takeaway 3 Updates on interest rate forecasting and best practices for managing CRE risk were among the most-read blogs. The FASB’s description of proposed changes can be found here.

I was at a strategic planning retreat a few weeks back where a colleague lauded the concept of bankers getting back to plain vanilla community banking. But if you read or watch interviews of CEOs of community FIs from 2008 forward, you will be bombarded with the message that they didn''t engage in the things that led to the collapse.

By 2008, there were a variety of failures as a result of liquidity – Bear Sterns, Lehman Brothers, and more. S&P Global estimates that in 2022, AOCI has reduced the tangible equity ratio at community banks (below $10B in assets) by an average of 1.99% (from 10.74% to 8.75%). However, community banks hold approximately 23.5%

As the Coronavirus circulates, Temasek Holdings Pte is instituting a company-wide wage freeze and requesting that senior management accept voluntary pay reductions for as long as one year.

2004-2008: 82.6% The emphasis for commercial credit risk management and evaluation is cash flow, fixed charges coverage, and working capital cycles. Digital engagement : CRE credit risk management tends to focus primarily on annual tax returns and rent rolls, while C&I lending relies on higher-frequency reporting.

In 2008, there were 7,061 FDIC-insured commercial banks in the U.S. For many community and regional banks looking to compete with larger financial institutions and grow their bank, the answer has been mergers and acquisitions. Cyber Complications for Vendor Risk Management. E-Commerce Merchants: A Hot Commodity in the Dark Web.

The fear of recession has decreased in 3Q, and the new primary concern shifts back to interest rate risk and deposit cost management. This article provides an update on pricing trends driven by our Loan Command aggregated community bank data and highlights some working pricing ideas. Total industry loans grew 5.1%

“… it’s not 2008.”. He went on to comment that since more than 70 percent of the regulatory agency’s operating budget consists of costs surrounding the exam process, “any reasonable suggestion regarding how to better manage the inexorable increase in these costs merits thoughtful reflection.”.

According to Intuit General Manager Alex Chriss, cash flow is a life-or-death factor for a company. ” In another statement, Euler Hermes Americas CEO and President James Daly said uncertainties and market risks have their own impact on organizations’ ability to manage cash flow, too. Fifty-two percent of U.S.

People facing charges include former community bank manager Carrie Tolstedt, former chief administrative officer Hope Hardison and former chief auditor David Julian, the sources told Bloomberg. The incident was among the biggest scandals in the banking industry since the 2008 crisis.

One of the key reasons for the complicated relationship – the term “frenemies” comes to mind – is that FinTech newcomers are demonstrating innovative approaches to traditional banking practices, including financial management services and money transfers, while older banks tend to be wedded to older systems. New tools for new FinTechs.

While the company will continue to operate in the asset management and general insurance spaces, Reliance shrunk its footprint by lowering its ownership in Reliance Nippon Life Asset Management from about one quarter to just over 4 percent. Last month Bloomberg reported that NBFCs in India have issued $1.5

Last year, community bank loan producers were faced with both record-low interest rates and a glut of deposits. But as they always do, they came through for individuals and businesses in their communities with a combination of personalized service and prudent risk management practices. First Community Bank of the Heartland, Inc.

It's what we did in 2008-10. Unlike 2008, banks were not the bane of our problems. In 2008, we were in the eye of the storm. Sure, community banks had little to do with liar loans or what was otherwise termed sub-prime. Community banks in particular. So they called around to their community bank.

Things went off the rails, not surprisingly, in 2008 — courtesy of the financial crisis. More businesses opened than closed — until 2008. In the aftermath of 2008, only 20 counties — most of them rimming major cities and tech hubs — drove 50 percent of small business formation. The mix of these businesses is also very different.

According to Intuit general manager Alex Chriss, cash flow is a life-or-death factor for a company. ” In another statement, Euler Hermes Americas CEO and President James Daly said uncertainties and market risks have their own impact on organizations’ ability to manage cash flow, too. 52 percent of U.S.

The 2008 financial crisis exposed significant weaknesses of relying on incurred losses. Credit Risk Management. 5 Inefficiencies Community FIs Must Resolve to Prepare for Economic Uncertainty. Any guess is better than modeling the average in the next 9-12 months. “A Learn More. C&I Loans. CRE Lending. Loan Pricing.

For the largest of American financial institutions – those that much of the public banks with for checking, mortgages and auto loans – stress testing regulations have been passed and executed to avoid a repeat of 2008. California is also a healthy state for banking – with 15 of 20 banks on the Western list in the Golden State.

Stress testing & deposit strategies in the spotlight The failure of Silicon Valley Bank offers other financial institutions the chance to reassess their approaches to and management of interest rate risk, liquidity risk, and credit risk. You might also like this whitepaper, "Inflation and rising rate's impacts on earnings and margins."

launched its own Faster Payments Service in 2008. The system would facilitate 24/7 year-round interbank settlements of faster payments and also provide a liquidity management tool to support transfers between Federal Reserve accounts. Community banks and credit unions also offered their backing. billion in 2018 to $26.9

Army Infantry Platoon leader who became a community banking manager. It’s no different in community banking. When I returned home from the deployment, the support I had from my community was clear—the same way Think Mutual Bank supports its local community. By Jeff Sabatke. It was 1 a.m. Paul, Minn.,

CPAs [(certified public accountants)] play a key role in the small business community as trusted business advisors,” said AICPA Vice President of Small Firm Interests Carl Peterson in a statement. The SBA and AICPA have been working together since 2008, the entities noted.

Community First Bank & Trust. Community First Bank & Trust had an extraordinary 2015. It was the culmination of efforts over the past four years to recover from the impacts of the downturn in the economy that began in 2008. The largest component of Community First Bank’s earnings in 2015 was a reversal of a $10.6

Fillz is a division of AbeBooks, a company purchased by Amazon in 2008. Fillz has been part of the AbeBooks community since 2006, so this was a difficult decision to make,” said AbeBooks’ Richard Davies. Fillz, an online tool for booksellers, is shuttering after 16 years, according to reports. AbeBooks acquired Fillz in 2006. “We

What this has to do with community bank investment management may not be readily apparent. The S&P 500 Index dropped 12.4%, which was the worst monthly stock performance since 2008. Belly of the curve matters to community banks. In fact, the tone is about to improve. More often, the two operate independently.

We consult to the mid-size and community banking space. The bank that didn’t dive into reverse swaps and other Wall Street shenanigans that caused so much pain back in 2008. By the way, don’t think that managers at community banks and credit unions are high-fiving each other because this occurred. They aren’t.

For one, Harman explained, SMEs that have a positive experience with an alternative lender will tell the others in the business community. While support from surrounding communities may be encouraging to a small business owner, it doesn’t always make the most financial sense. “Bank lending has still not recovered from 2008.

At recent Abrigo CECL Kickstart webinars, consultants demonstrated CECL implementation practices with an emphasis on the needs of community banks and credit unions. Once factors like the economy, new regulations, management changes, or even natural disasters are factored in, a greater allowance may be necessary. Keep me informed.

I recommend the following five mandates be on payments managers’ focus list this year: 1. Institutions that don’t have a payments manager should hire one. During the financial crisis in 2008, many financial institutions made the decision to sell their credit card portfolios entirely or convert them to agent relationships.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content