This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Find commercial real estate risks in the loan portfolio Sound riskmanagement practices in commercial real estate lending help lenders manage CRE credit losses and protect the portfolio's profitability. You might also like this podcast, "How to sleep easier at night about your capital and risk levels."

While we will cover the general lessons HERE , in this article, we wanted to focus on the root cause – how and why interest rate risk caused the second-largest bank failure in US history (Washington Mutual was the largest in 2008). Notably, most community banks’ duration risk is in the loan portfolio.

The banking industry has seen a steady stream of media attention since 2008, much of it in the form of stories about data breaches linked to major retailers or mega banks’ profits. Two recent surveys addressing the community banking landscape have pointed to increasing regulations as the primary cause of stress for these institutions.

Takeaway 3 Updates on interest rate forecasting and best practices for managing CRE risk were among the most-read blogs. Abrigo's most popular riskmanagement blogs over the last 12 months cover topics that continue to catch the attention of professionals and regulators. Which credit areas need routine "maintenance"?

While federal regulators only require this small number of banks to be subject to these particular stress tests, as outlined in the Dodd-Frank Act following the economic crisis of 2008, stress testing is becoming a critical part of financial institutions’ riskmanagement strategies, regardless of their asset sizes.

Stress Testing | 7 minute read Key Takeaways Stress testing is an important component of sound riskmanagement. Effective stress testing can benefit many different facets of lending, from riskmanagement and strategic decision-making to capital adequacy and liquidity management. Stress testing and riskmanagement.

2004-2008: 82.6% Credit risk : In C&I lending, at least part of the collateral is intangible. The emphasis for commercial credit riskmanagement and evaluation is cash flow, fixed charges coverage, and working capital cycles. 2010-2023: 137.3% trillion, Pruis said. Being ready to capture a share of the $1.7

Key Takeaways This recession is significantly different than the 2008 financial crisis, creating a unique credit environment for financial institutions. Economic downturns alter the credit memo's content and process to capture credit risk. More than six months after the coronavirus reached the U.S.,

In 2008, there were 7,061 FDIC-insured commercial banks in the U.S. For many community and regional banks looking to compete with larger financial institutions and grow their bank, the answer has been mergers and acquisitions. Lending & Credit Risk. Portfolio Risk & CECL. Learn More. Asset/Liability. Learn More.

CPAs [(certified public accountants)] play a key role in the small business community as trusted business advisors,” said AICPA Vice President of Small Firm Interests Carl Peterson in a statement. The SBA and AICPA have been working together since 2008, the entities noted.

Last year, community bank loan producers were faced with both record-low interest rates and a glut of deposits. But as they always do, they came through for individuals and businesses in their communities with a combination of personalized service and prudent riskmanagement practices. Photo by Linkes Photography.

Community-based institutions have unique circumstances (and personal viewpoints) that impact how they see the world in the future and what planning will look like for them. RiskManagement. Regulators are now ramping that back up, and model riskmanagement focused on portfolio risk is going to top the list.

Even if community businesses don’t end up utilizing the federally guaranteed loans , many small businesses have heard of SBA loans and want to explore them. During Abrigo’s recent ThinkBIG Conference, credit underwriting and loan portfolio riskmanagement trainer and consultant Michael Wear , CRC , of 39 Acres Corp.

Even if community businesses don’t end up utilizing the federally guaranteed loans , many small businesses have heard of SBA loans and want to explore them. During Abrigo’s recent ThinkBIG Conference, credit underwriting and loan portfolio riskmanagement trainer and consultant Michael Wear , CRC , of 39 Acres Corp.

Have we learned our lesson from the 2008 financial crisis? Technology Feature3 ManagementRiskManagementRisk Adjusted Operational Risk Credit Risk. How do we ensure it doesn’t happen again?

In the financial services sector, the threats posed by individual rogue traders, groups of disaffected employees and unhealthy risk cultures have highlighted the importance of conduct risk. While the 2008 foreclosure crisis highlighted conduct risk issues, the problem didn’t end there.

Here are some staggering numbers: Since the financial crisis of 2008, worldwide debt has increased by $70 trillion to $247 trillion, or 236% of world GDP versus 207% in 2008. Student debt has more than doubled from 2008 to $1.5 Dorothy has been with Penn Community Bank and its predecessor since November, 2004.

trillion in 2008. million at the end of December, 2007, before the crisis hit in 2008. million in December, 2008 and the peak occurred in October, 2009 at 21.4 Dorothy has been with Penn Community Bank and its predecessor since November, 2004. Weak readings on employment, housing data, and retail sales won’t stop them.

We have many examples, notably 2000-2001, 2006-2008, and 2019, when restrictive rates impaired growth and recession followed. DLJ 06/30/24 Dorothy Jaworski has worked at large and small banks for over 30 years; much of that time has been spent in investment portfolio management, riskmanagement, and financial analysis.

Another tool that was fairly effective in the years after 2008 was Forward Guidance, which involved Fed promises to keep rates low until specific dates in the future; this tool was one of Ben Bernanke’s faves. Dorothy has been with Penn Community Bank and its predecessor since November, 2004.

Although community banks did not lend to sub-prime borrowers in any meaningful way, did we participate? In many respects, community banks were caught in the cross-fire through the purchase of those mbs instruments – and subsequent trial through public sentiment. We took a serious reputational hit. Let those numbers sink in a bit.

It sounds like 2007 all over again, when people got tired of looking at LEI and then in 2008, all hell broke loose. DLJ 03/15/24 Dorothy Jaworski has worked at large and small banks for over 30 years; much of that time has been spent in investment portfolio management, riskmanagement, and financial analysis. Oh, brother!

This could be the biggest challenge since the 2008 financial crisis. Here's a sustainability crash course for banks and credit unions. The post Banks Can No Longer Ignore Climate Change (And Here’s Why) appeared first on The Financial Brand - Banking Trends, Analysis & Insights.

Back in 2008, the LHC started up with a bang and led to all kinds of new physics particle knowledge. DJ 01/11/19 Dorothy Jaworski has worked at large and small banks for over 30 years; much of that time has been spent in investment portfolio management, riskmanagement, and financial analysis.

Both spread inversions precede recession by 13 months (as in 2000 for the 2001 recession) to 26 months (as in 2006 for the 2008-2009 recession). DJ 07/16/19 Dorothy Jaworski has worked at large and small banks for over 30 years; much of that time has been spent in investment portfolio management, riskmanagement, and financial analysis.

Readers note: You can also view this post on Penn Community Bank's website. Dorothy Jaworski has worked at large and small banks for over 30 years; much of that time has been spent in investment portfolio management, riskmanagement, and financial analysis. Click here.

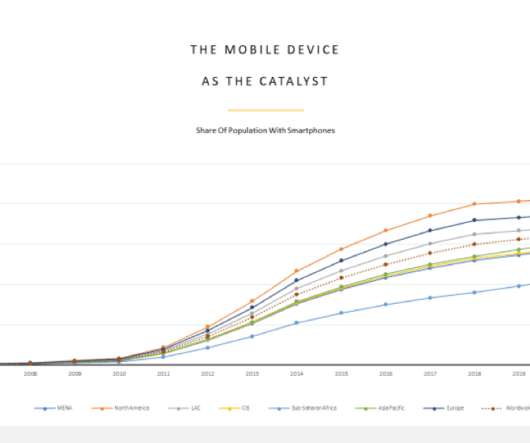

The introduction of the iPhone in 2007 – and the birth of the apps ecosystem a year later in 2008 –inspired an entirely new class of innovators, stating the 2010s with a brand-new toolkit. The last 10 years in payments and commerce have given us millions of dots to connect. 2020 Trendline Three: From The eWallet To The Everyday App Ecosystem.

The introduction of the iPhone in 2007 – and the birth of the apps ecosystem a year later in 2008 –inspired an entirely new class of innovators, starting the 2010s with a brand-new toolkit. The last 10 years in payments and commerce have given us millions of dots to connect. 2020 Trendline #6: The Global Game-Changer Of Voice.

Following the global COVID-19 outbreak, the collections & recoveries (C&R) community across Europe has jumped into action to safeguard customers, employees and wider stakeholders. This approach was particularly successful for Germany during the 2008-09 crisis, resulting in Germany only seeing a 0.9% Customer Forbearance.

If you withdraw your Ether, you get charged an interest rate determined by an open governance community. If you raised money from SoftBank, you have to take on large risk, while the banks will take another 5 years to touch real DeFi. (2) well, we know what 2008 looks like.

Stratyfy: Raised $12M, decision intelligence technology gaining traction, particularly in riskmanagement. Spring 2022 (San Francisco): Array: Credit and identity management platform, seeing increased adoption due to robust features and user-friendly interface. Finovate is currently an advertiser on this site.

Banks that are looking to enhance their riskmanagement practices should consider incorporating the concept of the velocity of risk into their enterprise-wide riskmanagement practices. Some risks occur slowly; others strike quickly and hard. Optimizing Risk. Luckily, nothing became of it.

Remember, it took the Fed seven years to raise rates from the zero bound after the Great Recession of 2008. Dorothy Jaworski has worked at large and small banks for over 30 years; much of that time has been spent in investment portfolio management, riskmanagement, and financial analysis. and unemployment was at 5.0%.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content