This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Artificial intelligence (AI) is poised to affect every aspect of the world economy and play a significant role in the global financial system, leading financial regulators around the world to take various steps to address the impact of AI on their areas of responsibility.

Maintaining regulatory compliance is a daunting task. Up to 200 regulatory changes occur every day, varying from large scale regulation like Dodd Frank, to minute changes to the font and size of footnotes in regulation text. Enter, IBM Watson Compliance. Confusion can become expensive in the compliance industry.

The financial crisis of 2008 and 2009 highlighted the need for timely data to identify and monitor liquidity risks at individual firms, as well as in aggregate across the financial system, especially with respect to intra-company flows and exposures within a consolidated institution.

First there was the financial crisis of 2008. Now, banks face what one financial regulator calls the “real game changer.” Then years of negative interest rates. Jesper Berg, the head of the Financial Supervisory Authority in Denmark, says the next big threat for banks is the rapid spread of big tech into financial services.

The banking industry has seen a steady stream of media attention since 2008, much of it in the form of stories about data breaches linked to major retailers or mega banks’ profits. Two recent surveys addressing the community banking landscape have pointed to increasing regulations as the primary cause of stress for these institutions.

While regulators had transparency and financial security in mind when introducing more stringent requirements for banks following the global financial crisis, financial institutions faced a sudden surge in the burden compliance. The Key To Compliance Is Data.

has strongly hinted that the agency she birthed in 2008 and opened for business in 2011 — the Consumer Financial Protection Bureau (CFPB) — should be given the authority to do even more. We don’t need more regulation. After all, The Big Three were regulated by the CFPB and the FTC, and look where that got us.

Facebook’s Libra project has renewed focus on how cryptocurrencies are regulated, with current rules on the sector patchy and varying from country to country. The Cost of Compliance. The projected 2020 cost of AML compliance across all U.S. financial institutions (77 percent) for AML compliance.

Will artificial intelligence help banks navigate the complexities of compliance more effectively? Against a backdrop where regulations have grown by leaps and bounds in the wake of the financial crisis, The Wall Street Journal reported that banks have taken on tens of thousands of new staffers tied exclusively to compliance.

The case in question goes back to 2008 when a Bulgarian wrestler was investigated for reportedly turning to drug trafficking. The fact that the bank let it continue until 2008, or even beyond, impeded or frustrated the detection of the money laundering activities,” the indictment read, according to Bloomberg.

Financial services providers that slack on regulatory compliance and fail to safeguard their operations against money laundering, terrorist financing and other criminal activities may face damaged reputations and significant fines. billion — 91 percent — of those penalties, while European regulators demanded $1.7 imposed a full $23.52

According to John Epperson, principal at Crowe LLP , that goes to show that the current approaches to regulatory and compliance technology ( RegTech ) aren’t working. Banks spent $100 billion on RegTech solutions last year, and $6 billion has been invested by venture capitalists since 2008. Common Concerns. Why RegTech?

Following on from my previous blog introducing the new year in the Fintech Innovation programme, I wanted to turn the focus onto the emergence of RegTech—technologies that address the challenge and cost of regulatory compliance. RegTech has two aims: increasing the effectiveness and the efficiency of compliance. Both are critical.

Following on from my previous blog introducing the new year in the Fintech Innovation programme, I wanted to turn the focus onto the emergence of RegTech—technologies that address the challenge and cost of regulatory compliance. RegTech has two aims: increasing the effectiveness and the efficiency of compliance. Both are critical.

The regulations will also hit Alibaba’s Ant Group, which took a beating last week after the government suspended its planned initial public offering (IPO). For example, the definition of “relative market” means that companies in a “dominant position” if they control more than 50 percent of the market would come under the new regulations.

Reports in Reuters on Tuesday (May 28) said UBS expects its regulatory costs to remain high in the years ahead after a decade of more stringent regulations leading to heavier, more costly burdens on banks. “That has tied up enormous resources.” “Why is this so significant?

The decade since the financial crisis of 2008 has been a challenging time for the financial services sector. Not only has the industry had to face the increased compliance and governance requirements that emerged as a result of new and tighter regulation intended to prevent a similar crisis in.

Today, governance, risk and compliance (GRC) is being transformed by not only rapidly-evolving regulatory standards and growing costs of non-compliance, but also by the clear and present need for greater GRC adoption/engagement – by the first line of defense – while delivering added value by empowering business users.

In the aftermath of the 2008 economic crisis, financial services regulators introduced a number of new measures to safeguard both the integrity and security of the financial system.

A series of regulations was established to encourage a safer, more transparent financial services environment following the 2008 financial crisis. Money laundering remains a significant problem in the financial services sector, though, despite the urgency brought about by 2008. A DIY Approach To AML/KYC.

They face the challenge of offering customers a smooth onboarding process while also remaining rigorous in know your customer (KYC) efforts, taking care to remain compliant with local anti-money laundering (AML) regulations that aim to keep criminals from using legitimate operations to move money illegally. About The AML/KYC Tracker.

Banks on Wall Street are talking to regulators about waiving rules regarding brokers working remotely while the coronavirus makes its way through New York, according to a report by Reuters. They’ve done this in the past around the 2008 financial crisis and 9/11. has been spearheading the industry response to the outbreak.

Abrigo's most popular risk management blogs over the last 12 months cover topics that continue to catch the attention of professionals and regulators. As regulators focus on interest rate forecasts used for interest rate risk management, remember that flattening, steepening, or inverting yield curves can influence your projections.

Earlier this month, the FASB considered and rejected further deferral of the CECL standard, initially issued in 2016 in response to the 2008 global financial crisis. Financial institutions that waited to begin adapting to the new regulations may find the thought of eleven months until compliance intimidating. CECL Regulation.

We had already identified that we wanted to grow out of being a point solution and become more of an end-to-end compliance and identity proofing platform,” Pointner said. “We The world saw this during the 2008-09 financial crisis, he pointed out, when fraud attempts doubled and, in some cases, tripled.

He was promoted to President and CEO in 2008. Bank Closed By Regulators Almost all bank closures happen on a Friday so that regulators can work all weekend to reopen the bank on Monday. In 2017, the bank was converted from its National Charter to a Kansas state-chartered bank and renamed Heartland Tri-State Bank.

A bill that would give regional banks a break on regulation was before the U.S. The bill also gives regulators more discretion in deciding when to require stress tests of capital adequacy for banks with between $100 billion and $250 billion in assets in the event of another crisis,” according to a summary of the bill in MarketWatch. “Tom

Today, IBM proudly accepted two distinguished RegTech Awards 2018 for our innovations within IBM Watson Regulatory Compliance: “Best AI Solution for Regulatory Compliance”. With these awards, what is most exciting is the recognition of the value we bring to clients in need of solutions for regulatory compliance and risk.

Learning from history, he referenced the lack of regulatory controls in derivatives and financial engineering before the 2008 financial crisis, and more recently, the unregulated growth of cryptocurrencies leading to the “Crypto Winter” of 2022.

As is the case today, albeit on a far smaller scale, the market crash of 2008 left millions unemployed and scrambling. New laws like California’s Assembly Bill 5 (AB5) and many others have also created new compliance hurdles for companies employing gig workers that must be managed.

Historically, banks are taking a reactive approach to risk: reactionary measures were largely behind financial institutions’ pullback from the small business lending market following the 2008 global financial crisis, for example. On top of that balancing act is the rising pressure of regulatory compliance, too.

The Dodd-Frank Wall Street and Consumer Protection Act was supposed to prevent another 2008 banking meltdown — and solve the problem of “too big to fail.” And those banks are going out of business — or merging with bigger players — largely due to the complexity and cost of compliance. billion annually in compliance costs.

AI is being applied to the world of regulation, or “RegTech,” and a new system can monitor the trading behavior of fund managers and even alert compliance bodies if questionable activity is detected. The UK’s Financial Conduct Authority issued a “call for input,” in 2015, and regulators are encouraging innovation.

Regulatory technology, or RegTech, was developed in the wake of the FinTech revolution and has been continuously expanding since the financial crisis of 2008. Experts predict it will rapidly advance the regulatory landscape by offering technological compliance solutions for the highly regulated financial services industry.

In a press release issued on Monday (June 25), the SBA announced a strategic alliance with the American Institute of Certified Public Accountants (AICPA) to help small businesses (SMBs) facing regulatory compliance and enforcement issues. The SBA and AICPA have been working together since 2008, the entities noted.

But Big Data lands new capabilities in the hands of corporate treasurers and other executives that yields active, real-time assessments of risks from multiple angles, from counterparties to compliance. A weak data management strategy could heighten the risk of non-compliance.

A recent report by Strategic Treasurer highlighted the roles Big Data and analytics have played in the progression of treasury management, both to mitigate risk, heighten forecasting capabilities and handle events like the 2008 financial crisis.

The 25% plunge -- the worst since July 2008 -- capped a tumultuous three days that shaved about €7.2 Wirecard AG fell the most in more than a decade on Friday after a report that a law firm found evidence of alleged forgery, the latest fraud allegations to beset the digital payments company. billion ($8.3 […].

Banks around the world are continuing to be penalized heavily for their inability to meet with ever-changing and complex financial regulations. For example, financial intelligence regulator Austrac handed gaming giant Tabcorp a fine of AUD 45 M (USD 35 M) for non compliance, the highest ever civil penalty in corporate Australian history.

To some, it may appear that the credit crisis is over — by the numbers, there’s more credit available now than there was in 2007 and 2008, just before the financial crisis hit. And regulators don’t like black boxes. One reason is fair lending compliance. Mapping “Fair”. Why is it so important to have a view into the black box?

’s Open Banking regulation made waves in the financial services market, and those effects have been felt far beyond the U.K.’s Today, Australian FIs are facing increased pressure from regulators, especially when it comes to small business banking and lending. ’s — and even Europe’s — borders.

The company is paying $75 million in penalties and restitution in connection with SEC allegations that its investment advisory arm overcharged customers it inherited in its Wachovia acquisition in 2008. The settlement is said to show the importance of conducting extensive compliance checks in a rapidly consolidating industry.

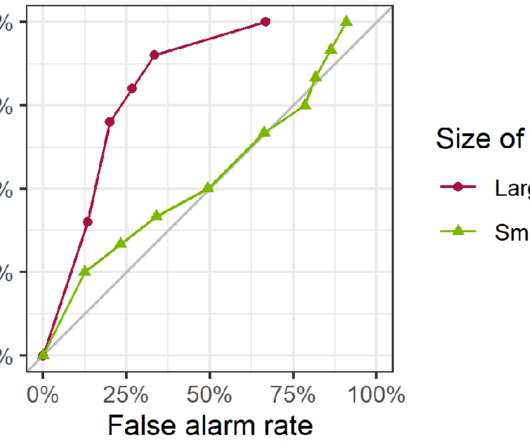

Do prudential regulations that work well for big banks work as well for small ones? This provides evidence that an efficient set of regulations for large banks might not be as efficient for small ones. Regulators would then need to think about whether a different set of regulatory requirements would be better for small banks.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content