This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In the wake of the 2008 global financial crisis, and banks' subsequent pullback from the small- to medium-sized business ( SMB ) lending arena, a slew of alternative lenders emerged onto the scene to fill the credit gap. What's just as important is to ensure that lending technology is flexible.

Ready to catch the next wave of lending growth? Commercial and industrial lending (C&I) will be the next big performance driver for banks and credit unions. You might also like this paper on how institutions can produce smarter, faster lending. C&I lending will be the next “bomb.”

and other nations around the world as a result of the global pandemic continues to draw comparisons to the 2008 financial crisis — so it’s only natural that analysts may turn to the past in an effort to predict what could lie ahead. “It comes in waves, there’s no doubt about it,” he said about the alt-lending boom.

From leveraging PPP technology to building relationships, reasons for boosting SBA lending are numerous. . Takeaway 1 SBA lending can expand your product offerings to help win deals with prospects and existing business customers or members. Why SBA Lending? Would you like others articles like this in your inbox? 1 and Sept.

‘Zombie lending’ occurs when a lender supports an otherwise insolvent borrower through forbearance measures such as repayment holidays and temporary interest-only loans. In a recent paper , I examine whether these lending practices contributed to the subsequent low output experienced by the euro area. Belinda Tracey.

The payday lending and debt collection industry is controversial, to say the least, and it is getting a day in court. As The Wall Street Journal reports, a racketeering trial that is currently taking place in New York may bring greater scrutiny to bear on how payday lenders operate. million people. million people.

The small- to medium-sized business (SMB) lending industry is used to adaptation, especially since the 2008 financial crisis, when legacy financial institutions (FIs) began pulling back and FinTechs and digital players stepped up in the space. Outdated Lending Practices Fail To Meet SMBs’ Current Needs .

India-based financial services provider Reliance Capital has announced it will exit the lending market. 30), Reuters reported , noting that the company is struggling to overcome “collateral damage” resulting from a slowing national economic and a broader “crisis,” the publication said, in India’s lending sector.

Lukies said that prior to the 2008 financial crisis, regulators and the like normally left banks to their own devices, as long as they didn’t mess it up so that people couldn’t pay their bills or go shopping. Before 2008, banks were making a lot of money from a lot of things,” noted Lukies.

We have a lot of predatory lending out here, which we want to regulate,” Geoffrey Mwau, director general of budget, fiscal and economic affairs at the country’s treasury, said on Thursday (May 24). Once the money is deposited, Kenyans can spend it anywhere in the country. Suri told the paper the kiosks act as debit cards.

It was the (initially) small FinTech startups that delivered a collective shakeup to the small business (SMB) lending industry. Their next target could be small business lending, and according to some experts, it’s fast approaching the market. New reports in Bloomberg on Wednesday (Oct. We’re starting to see that.”.

Payday and short-term lending is a contentious topic in the United States, particularly when it comes to its regulation. Most recently, Ohio capped off a 10-year regulatory project two weeks ago, with John Kasich’s signature on a new bill that will close loopholes in 2008 legislation to legally rein in short-term lenders.

And as reported in the Financial Times , banks that are relatively more dependent on lending activities to keep operations afloat are facing challenges that have not been seen since the financial crisis and recession of more than a decade ago. Cash crunches, of course, make carrying debt all the more burdensome.

Alternative small business lending firm Funding Circle has announced plans to launch in Canada. The company issued a press release Thursday (March 7) announcing it will add Canada to the list of jurisdictions in which it operates, which currently include the U.S., Germany and the Netherlands. Funding Circle’s U.K. market.

Recently a federal appeals court decided that the Consumer Finance Protection Bureau—a federal organization designed to safeguard against some of the pitfalls that led to the 2008 crisis—had been operating unconstitutionally, something which is certainly a blow to the agency itself and will no doubt have ramifications for how it Read More.

Reports by Financial Times said on Tuesday (May 24) that Wells Fargo vowed to continue to lend to businesses that have significant outstanding debt against the guidance of U.S. ” Reports said Wells has pursued greater market share in its non-retail banking operations since its acquisition of Wachovia in 2008. .

From leveraging PPP technology to building relationships, reasons for boosting SBA lending are numerous. . Takeaway 2 Far fewer financial institutions regularly participate in SBA (7a) lending than the more than 5,000 that joined the PPP. . Why SBA Lending? Want other articles like this on SBA loan origination in your inbox?

million SMBs operate across the country and account for 64 percent of new jobs. Only 35 percent of such businesses make it past their first decade in operation. SMB Lending Risks. Lenders are struggling to detect and stop these fraud attempts, with only 43 percent saying that they are very effective at identifying lending fraud.

In a recent paper we explore the effect on bank lending by combining data on exposure to negative rates with banks’ balance sheets, the Spanish credit register and firms’ balance sheets. This effect was especially strong for undercapitalised banks and lending to risky firms. Why might negative rates work differently?

The alternative small business lending market took home the biggest slice of cake this week with about $33.5 EZBob operates the Everline and EZBob online small business lending platforms, and CEO Tomer Guriel said in a statement that the funding “is proof of our game-changing technology and unique approach to business lending.”

The banking industry has seen a steady stream of media attention since 2008, much of it in the form of stories about data breaches linked to major retailers or mega banks’ profits. More than three-quarters of the bankers surveyed offered that anywhere between five and 20 percent of their total operating costs are driven by regulations.

In recent years, banks have even seen greater competition in the lending market from new FinTech players that can quickly approve loan applications and distribute funds to lenders. Some of the more prominent names in the marketplaces lending space include OnDeck, Kabbage and Orion First.

Credit risk operations, such as the allowance and stress testing, are not exempt. The 2008 financial crisis exposed significant weaknesses of relying on incurred losses. CRE Lending. Lending & Credit Risk. SBA Lending. How the Pandemic and PPP Have ‘Turbo-charged’ New Business Lending Strategies.

In a recent conversation with PYMNTS, Raghav Mathur, head of data science and analytics at Singapore-based Grab Financial Group , discussed the opportunities in data technology that can address the region’s most pressing SMB lending needs. In exchange, Grab gains greater visibility into SMB operations and performance. “By

Building trust with examiners became so important that when I was promoted to senior lending officer in 2005, I made it my mission that they wouldn’t uncover a problem I had not already identified. So, as you read this month’s lending issue, I encourage you to consider what steps you can take to be stronger and better.

There is growing talk, too, of FIs pulling back from small business loans as they did in the wake of the 2008 financial crisis. Interest rates' historic lows are adding pressure on small banks to continue operating, noted Shah. That's one of our biggest fears," he said. "We

According to the survey, while revenues grew for most, the percentage of firms operating at a profit remained unchanged from the previous year’s report. The 2008 financial crisis gave rise to the alternative lending market as a result of a massive gap in available capital, especially for small businesses and startups.

Financial institutions are in a constant balancing act: open up access to capital for borrowers to promote economic growth and financial inclusion and mitigate against the risk exposure lending produces — sometimes with disastrous implications for the global economy.

Is automation a missing link to a more productive and profitable commercial lending department? The 2015 Cornerstone Performance Report found significant reductions among mid-size banks in both monthly loans originated and outstandings per commercial lending full-time equivalent employee. – Reduced overhead and cost per loan.

In 2020, we will likely see financial institutions putting more emphasis on automating time-consuming, manual processes that bog down lending decisions. By automating these mundane, laborious tasks, lenders and credit analysts are then able to focus their time on the borrower or member and make faster, more efficient lending decisions.

Those read most often in the past year include several that offer practical advice for operating ALM and CECL models. Abrigo's most popular risk management blogs over the last 12 months cover topics that continue to catch the attention of professionals and regulators. The FASB’s description of proposed changes can be found here.

private and public lending markets are the world’s envy, with a wide availability of financing options for many capital seekers across the entire capital stack. Unfortunately, it is disruptive and costly when banks fail and Congress, regulators, and the public fret over the continued operation of the banking industry.

In the wake of the 2008 global financial crisis, new FinTechs surfaced to facilitate various forms of financing to small businesses as traditional banks pulled back from the market. While the world is one again in a precarious economic situation, this time around, bank lending has remained strong as a result of government programs.

has reached pre-2008 levels, meaning banks are facing risk that is elevated above what has been seen since the financial crisis. “If operating conditions in the U.S. banks’ direct leveraged lending risk is contained and mitigated,” noted the report. economy will remain largely unchanged during that time period. “U.S.

By the numbers , foreign firms will be able to own as much as 51 percent of domestic securities firms (including those in the fund and futures markets) operating in China, bumping the 49 percent cap up by two points. Now, total exposure to China, through lending, stands at $1.89 trillion at 2014’s end.

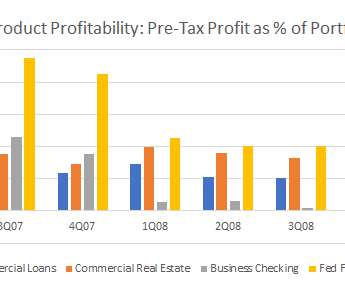

The much sought after "operating account." By the time the FF hit zero at the end of 2008, CRE was the last product standing. Two reasons, in my opinion: average balance per account, and operating expense per account. What does a "full relationship" mean? I thought, business loan plus a business checking account. CRE still wins.

The film opens in the wake of the 2008 financial crash: Fishwick’s customers are struggling to borrow from the high street, so he’s started lending them money. But to operate as a bank he needs a licence, and the Eton poshos regulating the banking sector decide he’s not the right sort of chap.

Guerrieri, Lorenzoni, Straub and Werning (2020) argue that while the lockdown is originally an (inflationary) negative supply shock because it keeps certain types of business from operating, the balance of the effects can resemble a (deflationary) demand shock under two conditions. Balance Sheets (Financial Assets Demand and Supply).

It’s a bold statement, considering that the lending space is still trying to articulate what, exactly, the financial inclusion problem is — and everyone else is still trying to figure out what, exactly, “machine learning” means and why it matters to them. First, many in the lending space may wonder, “What financial inclusion problem?”

“Main Street businesses depend on community and regional banks for the financing necessary to get started, sustain operations, manage cash, make payroll and create well-paying jobs,” the letter stated. According to reports, the Senate is expected to pass the legislation this week.

Consider the fact that the big players in Western banking, which had built up holdings in Chinese financial firms, had to sell their stakes in the aftermath of the 2008 financial crisis. At the same time, the lending environment is marked by bad loans. In one sense, there’d be a rebuilding going on.

billion from the GAM Greensill Supply Chain Finance investment fund, operated by GAM and Greensill. GFG Alliance told the Financial Times that it is “satisfied that we have ample access to capital and headroom within our range of available lending facilities to satisfy the needs of our businesses and their growth.”.

The DOJ investigation centered on whether LendingClub had – between January 2009 to September 2010 – misled its FDIC-insured loan originator, WebBank , leading the bank to underwrite over 200 loans that did not conform to the bank’s lending requirements. Attorney Alex Tse. “We The Response.

The Dodd-Frank Wall Street and Consumer Protection Act was supposed to prevent another 2008 banking meltdown — and solve the problem of “too big to fail.” Since the passage of Dodd-Frank, over 1,700 U.S. banks have disappeared.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content