This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Moody’s Investors Service reported Thursday (June 8) that credit card charge-offs — debts that are so delinquent that lending institutions have basically given up on collecting them — are at their highest rate since 2009 , possibly due to loosening lending standards. Capital One wasn’t far behind at 5.31 percent in 2016.

On balance, the literature is critical of loan forbearance in the corporate sector because of its potential to contribute to zombification a situation where bank lending keeps unproductive firms alive, resulting in lower aggregate total factor productivity. The Act boosted the aggregate capital stock by 1.4% on average over 201018.

Lending Club, which has been struggling to recover from loan errors and the departure of its Chief Executive (among other issues), has named Patrick Dunne, a veteran of BlackRock, as its new chief capital officer. Dunne is well known in financial circles and his appointment is seen as a boon to the beleaguered Lending Club.

This post investigates whether large and small banks in the UK and US differ in the cyclical patterns of capital positions and credit provision. The reforms aimed to ensure that banks have sufficient capital resources to absorb losses and reduce the cyclical effects of bank capital (and regulation) on the supply of bank credit in stress.

However, Tavares said the landscape is shifting, as LendingPoint and other alternative credit products lend their ears — and their money — to underserved populations. Burnside got his start in small business lending. It’s a very real situation in the U.S., which is where Dominican-born LendingPoint CSO Juan Tavares now calls home.

In some areas, the growth in sub-prime lending matches overall growth in the segment, with credit cards and personal loans as the best example. The sub-prime mortgage segment has also performed strongly in terms of delinquencies, in line with overall trends in the mortgage world since 2009. percent to 18.63 It never happened.

In a recent Sageworks webinar Robert Ashbaugh, senior risk management consultant at Sageworks, discusses High Volatility Commercial Real Estate (HVCRE) lending best practices. Ashbaugh goes on to demonstrate that the default rates for these loans did not peak until about 2009, and the ALLL did not increase until 2010.

When the economy crashed in 2008, and fully bottomed out in June 2009 credit across the board froze. While other forms of credit were showing signs of returned in 2014, SMB lending still trailed its 2007 peak by 17 percent. The good news is that the bad news wasn’t worse news — the economy recovered, albeit unevenly and slowly.

private and public lending markets are the world’s envy, with a wide availability of financing options for many capital seekers across the entire capital stack. However, the ordinary course of acquisitions and mergers provides a safe and orderly redistribution of capital from underperforming to outperforming managers.

The reports were positive: all 31 stressed banks “passed,” showing that they are stronger than they have been at any time since the tests began in 2009, the Fed reported. During examination time, regulators are increasingly looking at a bank’s stress testing processes and resulting capital plans.

The following is an excerpt from the Sageworks whitepaper "Optimizing Capital: Challenges and Opportunities for Financial Institutions". Yet all financial institutions face internal and external challenges that place demands on personnel, time and – perhaps most importantly – on capital.

Bank Innovation today released a beta of its relaunch, the most significant rebuilding of the site since its start in 2009. Let us know what you think of the rebuilt site by emailing info@bankinnovation.net.

Today, Bank Innovation releases its most significant redesign and relaunch since the site initially dropped online in 2009. We hope you love the new Bank Innovation. When we started Bank Innovation, while the crosswinds of the credit crisis were still swirling, we were the lone voice for innovation at banks.

We have undertaken our most significant redesign and relaunch since Bank Innovation initially dropped online in 2009. This beta officially kicks off today and marks a new chapter in the life of Bank Innovation. We hope you love it. When we started Bank Innovation, while the crosswinds of the credit crisis were still swirling, we […].

The DOJ investigation centered on whether LendingClub had – between January 2009 to September 2010 – misled its FDIC-insured loan originator, WebBank , leading the bank to underwrite over 200 loans that did not conform to the bank’s lending requirements. lending marketplace. The DOJ Finding. Attorney Alex Tse. “We

On this day in history in the year 2009, the world of payments and commerce was changed forever. No, we’re not talking about the launch of Square – that was in February of 2009. True in 2009. The skies parted, the Earth shook and the song of angels was heard from on high. Well, that’s how we remember it, anyway.

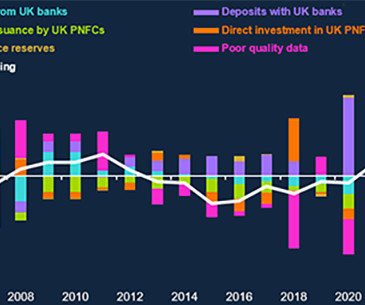

In our paper , we use balance sheet data for 118 UK banks to empirically investigate whether the asset compositions of banks involved in the UK QE operations reacted differently in comparison to banks not involved in the initial rounds of QE between March 2009 and July 2012. QE and bank lending. QE and central bank reserves.

Take Capital One, the credit card company, for starters. Earlier this month, Moody’s Investors Service reported credit card charge-offs — debts that are so delinquent that lending institutions have basically given up on collecting them — are at their highest rate since 2009, possibly due to loosening lending standards.

There is ample evidence that a monetary policy tightening triggers a decline in consumer price inflation and a simultaneous contraction in investment and consumption (eg Erceg and Levin (2006) and Monacelli (2009) ). Chart 2 shows that the shock also triggers a substantial and persistent contraction in private banks’ equity capital.

This includes global transaction services, small business services, commercial and small business lending, and the changing role of corporate treasury and its impact on meeting the needs of corporate banking clients. On the lending side, US commercial loan outstandings have more than fully recovered from the 2008-2009 financial crisis.

One key message stands out: banks that are more rooted in their market are much more likely to continue lending when faced with the economic fallout from such shock. Banks with access to central bank liquidity continued or even expanded their lending. A pandemic or natural disaster can impact lending in several ways.

In lending, in determining whether credit is likely to be repaid by a borrower, the devil is in the details. This translates into recurring net savings, which translates into an accumulation of capital, which can be used for repayment. What if the details are the wrong ones? The Two C’s .

Much of Wells Fargo’s jump can be attributed to its acquisition of corporate loans from GE Capital, reports noted. Figures from the Federal Deposit Insurance Corporation show that the lending sector has added $1.43 It marked the first time that banks added to these reserves since 2009, Bloomberg said.

“Delinquency rates have risen in part because lending to sub-prime borrowers increased significantly in recent years,” CreditCards.com’s senior industry analyst, Matt Schulz, said in the report. That brings with it a lot of risks, for both the banks and the consumer.”.

But, Passione noted, many of the players who are taking a pass on offering student lending and other forms of personal loans often aren’t doing so for lack of interest — but lack of ability via smart technology. Lending-as-a-Service. By offering a white label lending service, we are making those connections possible.”.

Alternative lending platforms integrating with providers of other financial services has become a new norm. Just look at SAP Ariba , which integrated PrimeRevenue’s supply chain financing into its spend management platform, or Reckon , a small business accounting platform that recently rolled out an SME lending feature thanks to Prospa.

Today, I read an American Banker article on how a multi-billion dollar bank is going to ramp up its business lending. To remind readers, in 2006 the OCC, Federal Reserve, and FDIC issued joint interagency Guidance on Concentrations in Commercial Real Estate Lending. They need a marketing person to title their reports.

The year was 2009, and it was rough for some, but a fertile ground for others. “I Kabbage is a data and technology platform that enables real-time lending. Our focus has always been on user experience and for them to get capital in less than ten minutes. The goal of all that money is, of course, to lend to small business owners.

Fragmentation is likely to have wide-ranging implications for the global economy, including increasing the volatility of capital flows and exposing gaps in the global financial safety net (GFSN). The GFSN consists of a set of financial instruments and institutions that act as insurance for countries facing sudden stops in capital flows.

After the Great Recession, financial institutions retained more capital to build in buffers to face uncertain times like this. During the crisis in 2009, the banking system saw shockwaves hit, causing a number of bank closures. Lending & Credit Risk. SBA Lending. Today’s situation is 180 degrees from that environment.

The real trick is to tie engaging consumer experiences to those cards, which is critical, as prepaid and reloadable cards continue to evolve — moving from plastic cards to mobile accounts that can adapt to an expanding portfolio of use cases, including payroll, online gambling or even consumer and business lending. Step back a bit first.

Since its founding in 2009, Artsy has grown to encompass more than 800,000 pieces of art by 70,000 different artists. The round was led by Avenir Growth Capital, with further investments by industry leaders in art, media and technology – some who have supported Artsy from the start and others who were just finding out about it.

But despite its market size, SMEs are struggling to get the working capital they need. Even with the SMEs that did not seek financing in the time period, the CFIB found that many of these companies expressed a need for capital anyway. percent in 2009, it still is significantly higher than levels seen in 2000 (10.5

In subscription and services-based revenue: Square’s Instant Deposit , its food delivery platform Caviar and its lending platform Capital brought in $65 million in revenue during the third quarter of 2017, and 84 percent year over year. Killer Stats. billion: Square’s gross payment volume for Q3 2017. $2

In a conversation with economist and author of “Matchmakers: The Economics of Multi-Sided Platforms,” David Evans, in 2009, Co-Founder and CEO Jack Dorsey initially hinted at ambitions of controlling both ends of the payments ecosystem with what he called a “more elegant” payments experience. And industry pundits fell in love. What’s Next.

This isn’t 2008 or 2009, when consumers were having a hard time paying their bills and small business owners were trying to keep the lights on. Small-dollar lending is one option. There seems little doubt that short-term lending and brief boosts to cash flows for consumers and small businesses will always stand as vital economic needs.

Net lending represents the overall surplus or deficit, and it is theoretically the same whether you look at it from the income or financial account viewpoint. Evolution of the net lending positions of households and corporates The pre-GFC era was a period of strong growth and low inflation , which coincided with a large expansion of credit.

The biggest announcement came as Magento Commerce, spun out from eBay two years ago, got $250 million from Hillhouse Capital, one of China’s largest investment firms. The new capital will help fund global expansion, with focus, as the name implies, on eCommerce. The implied valuation here is $700 million.

Software and apps and connected devices are disintermediating the POS checkout experience that has been retail’s cornerstone for more than 270 years using a device that, ironically, expanded digital payments acceptance for small merchants in 2009 with Square. All of these same forces are disrupting banking and lending.

He joined COB's board in 2009 after its $310 million recapitalization which was needed from a disastrous slew of losses incurred starting in 2008 as a result of awful credit decisions, leading to a 21% NPA/Asset ratio peak in 2010. Selection: Mitch Englert, EVP of Community Banking, Capital City Bank Group, Inc.

Here’s the bottom line: In the past six years (March 2009 to March 2015), the top 10 Internet banks have grown an impressive $175 billion in new deposits. Here’s the breakdown of these 10 banks in order of deposit growth: Deposits ($000): March 2009 Deposits ($000): March 2015 6-Year Growth. ($000). Think about this. billion in 2010.

The private equity firms that have backed the latest capital infusion are ones that are known for doing so as their investees get ready to go public. The Capital One data showed that such stepped-up activity will not occur in the next six to 12 months. vehicle recalls from 2009 to 2010. Just when is a matter of speculation.

This growth has created major opportunities in the payments space, and companies like Stripe — the payments unicorn valued at a masive $35B — are hungry to capitalize on them. Business lending and corporate cards. Most recently, Stripe has launched a Corporate Card and a Lending product geared towards small businesses.

For the third consecutive year, we worked with The New York Times to identify and rank the top 100 venture capital professionals from around the globe. Below are the detailed profiles of the Top 20 Venture Capital Partners. PROFILES OF THE TOP 20 VENTURE CAPITAL PARTNERS. Current Firm: First Round Capital (Founding Partner).

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content