This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The Federal Deposit Insurance Corporation ( FDIC ) gave the green light to an application from the FinTech firm Square to create a de novo industrial bank in Utah, the agency said on Wednesday (March 18). was formed in 2009 as a payment services provider to enable businesses to accept card payments. Square, Inc.

.” SNC (pronounced like the candy bar but without the “ers”) stands for the Shared National Credit Program, which, since 1977, has assessed risk in the largest and most complex credits shared by multiple regulated financial institutions. Loan reviews are completed in the first and third calendar quarters each year.

In the wake of regional bank failures, one potential answer to equity shorting and bank runs is having the FDIC increase deposit insurance. The regulators are considering three options: raising the limit above $250k, raising the cap for only certain accounts (such as banks’ business accounts), or eliminating the cap entirely.

With increasingly few exceptions, the ranks of the unbanked seem to be on the decline, according to new data released by the FDIC. According to FDIC data, unbanked American consumers peaked toward the end of the Great Recession in 2011 at 8.2 The percentage of Americans going without banking services fell to 7 percent in 2015 from 7.7

recorded its fourth bank failure this year — the first collapse of financial institutions since 2017, according to data from the Federal Deposit Insurance Corp ( FDIC ). Assets and deposits were assumed by Industrial Bank, a press release from the FDIC indicated. “On Approximately $500,000 in deposits exceeded FDIC insurance limits.

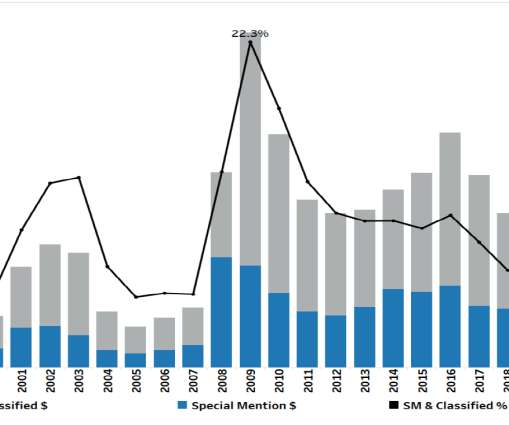

Ashbaugh’s presentation begins with a quick summary of why regulators care about HVCRE. Ashbaugh goes on to demonstrate that the default rates for these loans did not peak until about 2009, and the ALLL did not increase until 2010. That 13% represented 80% of the losses to the FDIC insurance fund. How did we get here?

The FDIC has nearly quadrupled its enforcement actions (“EA”) over the past three years. The productive view about the similarity of EAs is why haven’t we been doing some of the things required by regulators in the first place? Banking is a highly regulated industry, and has been since the Great Depression.

When the economy crashed in 2008, and fully bottomed out in June 2009 credit across the board froze. What is as true today as it was in the year 2009, she said, is small businesses aren’t starting, lasting, expanding and thriving — because of inadequate access to capital.

The year was 2009, and it was rough for some, but a fertile ground for others. “I Petralia remembers back to 2009 when the team was looking for a bank partnership. In a highly regulated sector, regulations are ever-evolving, which can implicate, limit and change relationships.

She hid them from the Board and regulators with assistance from unnamed co-conspirators." When the TDB shut them down and the FDIC investigators came in, they had to occupy the church next door because of the smell from the fire. The FDIC issued this guidance in June 2011. Well, not actually Pat.

And regulators are getting anxious. Reading between the lines, this bank is likely over the CRE guidance levels, and were probably getting grief from their regulators about it. To remind readers, in 2006 the OCC, Federal Reserve, and FDIC issued joint interagency Guidance on Concentrations in Commercial Real Estate Lending.

The DOJ investigation centered on whether LendingClub had – between January 2009 to September 2010 – misled its FDIC-insured loan originator, WebBank , leading the bank to underwrite over 200 loans that did not conform to the bank’s lending requirements. The DOJ Finding. In 2010, LendingClub added to its war chest with a $24.5

has been released from a consent order that the FDIC and the Montana Division of Banking and Financial Institutions had implemented in December 2009. Freedom Bank in Columbia Falls, Mont.,

The Economic Growth, Regulatory Relief, and Consumer Protection Act directs the CFPB to implement an exemption from the mandatory escrow account requirement for higher-priced mortgage loans under the Truth in Lending Act and Regulation Z for certain insured credit unions and insured depository institutions. Role of Supervisory Guidance.

The CFPB’s key findings are: Based on a comparison of data from 2009 with year-end 2021 data, the number of college credit card agreements, overall payments from issuers to IHEs, and open accounts continue to decrease. ED also stated that it “will monitor compliance and take corrective action to enforce these regulations when necessary.”.

Second, this can be accomplished only if the industry does not have too much influence over its regulators and if the regulators have the ability to hire, train, and retain qualified staff. Third, the regulators need adequate financial resources. My lesson learned to the regulators, read your past lessons learned.

The agencies are the Comptroller of the Currency, Farm Credit Administration, FDIC, Federal Reserve Board, and National Credit Union Administration. Recently federal agencies proposed revisions to the Interagency Questions and Answers Regarding Flood Insurance.

But regulators are not exactly on board. And more recently, Lending Club has a $185M acquisition of Radius Bank pending, though the lender’s $80M Q2 loss is not going to help ease regulators’ concerns. And going back a bit further, I’d put Suresh Ramamurthi and Suchitra Padmanabhan’s 2009 acquisition of $3.5M

When the economy came crashing down in 2009, The Peoples Bank was able to work with customers facing hard times. Regulation Review Committee, vice chairman. FDIC Advisory Committee on Community Banking, member. Both the regulators and Congress respect us for what we stand for,” he observes. “So Membership-Marketing.

Cryptocurrency regulation is on the horizon The ups and downs of the cryptocurrency scene have illuminated a need for guidance for traditional financial institutions. Takeaway 2 While these financial products are appealing, the lack of stability and consumer protections surrounding them are a concern for the FDIC. ? .

IMCRs When the financial crisis struck, and FIs began to falter, regulators were issuing regulatory orders (supervisory agreements, written agreements, cease & desist orders, and memorandum of understandings, collectively "ROs") faster than my daughters point out that I''m wrong. It has come from three places, in my opinion.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content