This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Interventions in corporate credit markets have featured prominently in the policy response to crisis episodes over the last two decades. First, we develop a search and matching model of the credit market where banks have incentives to forbear. Framework for policy evaluation We analyse the policy in four steps.

However, Tavares said the landscape is shifting, as LendingPoint and other alternative credit products lend their ears — and their money — to underserved populations. Burnside got his start in small business lending. Already the market was generating $1 billion in personal loans each month. “It Back to Basics.

The thinking is that diversification-induced lending leads to banking resiliency. We believe that while lending diversification leads banks to lend more in normal times (especially for banks over $50B in assets) and does benefit the general economy, community banks should be careful in how and where they choose to diversify.

The thinking is that diversification-induced lending leads to banking resiliency. We believe that while lending diversification leads banks to lend more in normal times (especially for banks over $50B in assets) and does benefit the general economy, community banks should be careful in how and where they choose to diversify.

In 2016, the market experienced a pullback as lenders slowed or stalled sub-prime originations,” Komos said. In some areas, the growth in sub-prime lending matches overall growth in the segment, with credit cards and personal loans as the best example. It shows the resiliency of the market.”. percent to 18.63 It never happened.

New rules aside, we were not that significant in the mortgage market anyway. So we opened the door, let the competition through, and we ceded the mortgage market to brokers, specialists, and the government. For example, volumes were down in my home state of Pennsylvania from 2009 through 2010, the latest year HMDA data is available.

private and public lendingmarkets are the world’s envy, with a wide availability of financing options for many capital seekers across the entire capital stack. We believe any change to the FDIC insurance coverage should aim to maintain and advance our credit markets.

As the market has shifted from 2009, almost every bank wants to grow, and they are receiving pressure to do that,” says Peter Brown, director of strategy and operations for the financial institutions division at Sageworks. Speed to market is critical,” Brown says. “An

Bank Innovation today released a beta of its relaunch, the most significant rebuilding of the site since its start in 2009. Let us know what you think of the rebuilt site by emailing info@bankinnovation.net.

When the economy crashed in 2008, and fully bottomed out in June 2009 credit across the board froze. While other forms of credit were showing signs of returned in 2014, SMB lending still trailed its 2007 peak by 17 percent. The good news is that the bad news wasn’t worse news — the economy recovered, albeit unevenly and slowly.

Today, Bank Innovation releases its most significant redesign and relaunch since the site initially dropped online in 2009. We hope you love the new Bank Innovation. When we started Bank Innovation, while the crosswinds of the credit crisis were still swirling, we were the lone voice for innovation at banks.

We have undertaken our most significant redesign and relaunch since Bank Innovation initially dropped online in 2009. This beta officially kicks off today and marks a new chapter in the life of Bank Innovation. We hope you love it. When we started Bank Innovation, while the crosswinds of the credit crisis were still swirling, we […].

The DOJ investigation centered on whether LendingClub had – between January 2009 to September 2010 – misled its FDIC-insured loan originator, WebBank , leading the bank to underwrite over 200 loans that did not conform to the bank’s lending requirements. The DOJ Finding. Attorney Alex Tse. “We The Response.

This marks the first time in history a peer-to-peer lending facilitator in Europe has listed Russian loans. Twino was founded in 2009 and currently sells loans from Georgia, Latvia, Denmark, Estonia and Poland. Low interest rates have been the norm in the global lendingmarket for the past few years.

Its analysis also found that the rise in alternative and marketplace lending options in the market has not yet made a significant impact on SMBs’ ability to access trade finance products. According to the FIs, the program has facilitated more than $30 billion in trade finance to SMBs across Asia since its launch in 2009. “As

is becoming a divided market, where some dreams come true and others must keep wishing and hoping. As reported in the Wall Street Journal , the housing lendingmarket has become a bifurcated one, with credit costs low in a phenomenally low interest rate environment. If the American dream is buying real estate, the U.S.

One key message stands out: banks that are more rooted in their market are much more likely to continue lending when faced with the economic fallout from such shock. Banks with access to central bank liquidity continued or even expanded their lending. A pandemic or natural disaster can impact lending in several ways.

The first was on the valuation of assets in six private funds, and the other was tied to loans made in 2009 to the former CEO and three of his family members. Lending Club is set to hold an annual shareholders meeting Tuesday (July 5th) after postponing the event three weeks ago. The toll has been swift and measurable.

As a result, we dropped rates to such a level that it wasn''t attractive to traditional CD customers and they began parking money in liquid savings vehicles, such as the money market account. But the chart below from recent Small Business Administration research, although using 2009 data, demonstrates a trend worth noting.

Beard will focus on launching new products for marketers and expanding Cardlytics’ advertiser relationships in his new role, while Johnson will help Cardlytics’ financial institution partners expand their loyalty programs in her new role. Johnson joins Cardlytics from SunTrust , where she was SVP and head of Consumer Direct Lending.

This includes global transaction services, small business services, commercial and small business lending, and the changing role of corporate treasury and its impact on meeting the needs of corporate banking clients. On the lending side, US commercial loan outstandings have more than fully recovered from the 2008-2009 financial crisis.

Today, I read an American Banker article on how a multi-billion dollar bank is going to ramp up its business lending. To remind readers, in 2006 the OCC, Federal Reserve, and FDIC issued joint interagency Guidance on Concentrations in Commercial Real Estate Lending. They need a marketing person to title their reports.

“Delinquency rates have risen in part because lending to sub-prime borrowers increased significantly in recent years,” CreditCards.com’s senior industry analyst, Matt Schulz, said in the report. Synchrony and Alliance Data are focused on the store-branded, private label credit card market.

The ability of financial institutions to make concessions and work to provide the markets with assurances is a direct result of their overall financial well-being, as well as their nimbleness. During the crisis in 2009, the banking system saw shockwaves hit, causing a number of bank closures. Lending & Credit Risk.

Dollar shortages in funding markets outside the United States have been a recurrent feature of the last three major crises, including the turmoil associated with the ongoing Covid-19 pandemic. As part of this swap operation the Fed lends US dollars to a foreign central bank, receiving the other country’s currency as collateral.

The $1 trillion level has been attained for credit card debt within the country, with that level not seen since early 2009, when the shockwaves of the financial crisis first were felt. Those two subsets of lending hit their own respective $1 trillion levels over the past few years. In the U.S., at least, debt is no four-letter word.

In recent years, market reports have shown that art as a business has seen a lot of consolidation, shrinking the overall market size – but one avenue is expanding, and that’s online. The market as a whole has gotten smaller, but the online market has grown,” Carey said. “The

After all, despite recent stock market woes, the economy remains relatively strong, with low unemployment. After all, despite recent stock market woes, the economy remains relatively strong, with low unemployment. Small-dollar lending is one option. The Situation. Cash Flow Help. So, what exactly is offered?

The real trick is to tie engaging consumer experiences to those cards, which is critical, as prepaid and reloadable cards continue to evolve — moving from plastic cards to mobile accounts that can adapt to an expanding portfolio of use cases, including payroll, online gambling or even consumer and business lending. Step back a bit first.

The inevitable end of the chip shortage will expand the pool of vehicles to choose from and lower transaction prices as the market moves toward some semblance of normal. In 2021, subprime delinquency rates hit the highest mark since 2009. Fewer cars are being sold, perhaps, but profits are reaching record highs. Until it isn’t.

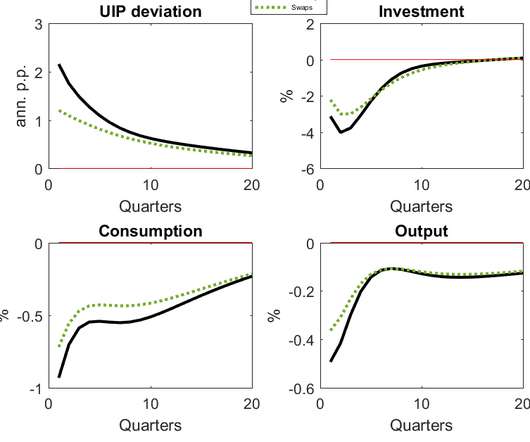

There is ample evidence that a monetary policy tightening triggers a decline in consumer price inflation and a simultaneous contraction in investment and consumption (eg Erceg and Levin (2006) and Monacelli (2009) ). They either assume frictionless financial markets, or consider frictions in firms’ demand for investment funding.

A few days later, one of the founding fathers of FinTech, Renaud Laplanche , was forced out of Lending Club, the peer-to-peer lender he founded in 2006, following scandals over loan disclosures and conflicts of interest. The really interesting, though less juicy, story is what got Lending Club into trouble. Again, it hasn’t worked out.

But despite its market size, SMEs are struggling to get the working capital they need. percent in 2009, it still is significantly higher than levels seen in 2000 (10.5 Nearly half of Canada’s SMEs have applied for some form of financing in recent years. percent) has declined since a high of 19.3 But according to the CFIB, only 0.1

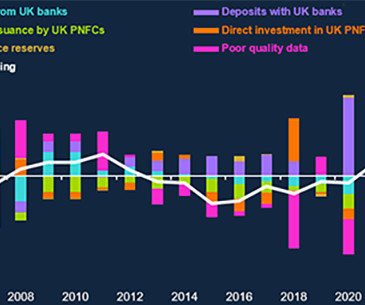

Net lending represents the overall surplus or deficit, and it is theoretically the same whether you look at it from the income or financial account viewpoint. Evolution of the net lending positions of households and corporates The pre-GFC era was a period of strong growth and low inflation , which coincided with a large expansion of credit.

Survival depends upon how well the incumbents anticipate a future beyond the one they entered the market to disrupt — and how prepared they are to change their strategy to disrupt their once-disruptive ways of doing business. All of these same forces are disrupting banking and lending. Disruptors Being Disrupted.

Since the Credit Card Accountability Responsibility and Disclosure Act passed in 2009, Paradis and Youakim said, credit card companies are legally prohibited from marketing to college students with no credit history. Not charging interest for lending out money sounds like a losing proposition for a company focused on consumer finance.

Big banks have been in the driver’s seat on growing their market share in retail, while paring down branch networks. Meanwhile, Wells plans to close 450 branches by 2019, BofA has closed 1,600 branches since 2009, and Chase closed 365 since 2015. Digital: The New Must-Have. The Transformation of Delivery.

Alt Lending. Yes, alt lending has the distinction of being on our Fizzle list ever since we started keeping count. combined with softening demand in developing markets, have cut into sales. Stay tuned. Keep the streak alive! It’s why everyone is looking to the cloud. Sizzle or Fizzle? The Blue Coat IPO.

So, while McKelvey lost out on that $2,000 sale — he and his (friend) and Co-Founder Jack Dorsey — the founder of Twitter — did end up with a $17 billion idea (Square’s market cap at the time this piece went to press). Square has come a long way from being an mPOS solution for cash-based glass blowers and farmers market purveyors.

As of the last PYMNTS/InfoScout report on in-store mobile wallet usage, and particularly for the longest running general purpose mobile wallet in the market, Apple Pay, 19 out of 20 users who could use a mobile wallet don’t. The marketing doesn’t matter — the problem the solution solves does.

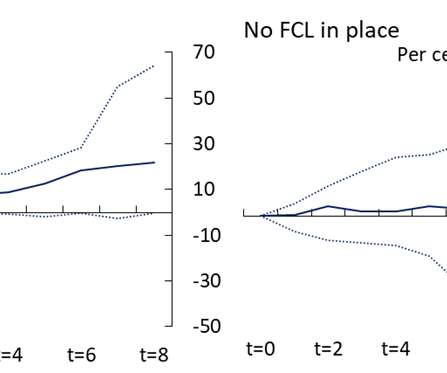

It includes countries’ foreign reserves, Regional Financing Arrangements (RFAs), central bank swap lines, and IMF lending. The country’s commitment to good policies, the Fund’s endorsement, and the access to IMF resources that accompany this, send a reassuring message to markets.

The Covid-19 shock had a big impact on stock markets worldwide. Using a newspaper-based Equity Market Volatility (EMV) tracker Baker et al (2020) show that no previous infectious disease outbreak, including the Spanish Flu, has impacted the stock market as powerfully as the Covid-19 pandemic. How do firms shore up on liquidity?

The company’s market capitalization, which after declining to less than $600 million in the 2009 recession, has now grown to almost $3 billion. This was a terrific combination of two education-focused cooperatives across both Southern and Northern California markets. Best of luck in the next chapter, Chris!

Yet while the demos and screen shots at events like Finovate have provided fascinating fodder regarding the future of digital banking, the FACTS show that these buzz-worthy players have had infinitesimal impact on market share. Niche players Everbank and CIT use Internet deposits as cheap funding for commercial finance and lending activities.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content