This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Ready to catch the next wave of lending growth? Commercial and industrial lending (C&I) will be the next big performance driver for banks and credit unions. You might also like this paper on how institutions can produce smarter, faster lending. C&I lending will be the next “bomb.”

On balance, the literature is critical of loan forbearance in the corporate sector because of its potential to contribute to zombification a situation where bank lending keeps unproductive firms alive, resulting in lower aggregate total factor productivity. in 2010 corresponds to the law depressing average interest rates by 40% in that year.

And in lending, with the financial crisis in the rearview mirror, a decade on, invention – okay, innovation – has become a hallmark, at least in some corners. But a standstill in the credit markets created a vacuum for a bit, at least along traditional lending conduits. Necessity is the mother of invention. Mortgages ?

Europe’s Financial Stability Board ( FSB ) said on Friday (June 7) that higher bank capital requirements, which were put on the books during the financial crisis, will remain. Reuters , citing the regulator, reported it found the negative impact on small business lending was short in nature, and that there is no need to change the rule.

Metro Bank CEO Daniel Frumkin said the deal gives his company a strong base for addressing its “strategic ambition” to expand into unsecured lending. The bank had been set to rapidly expand its branches and beef up its mortgage lending. RateSetter, founded in 2010, said it is “the U.K.’s

Federal bank regulators work together to design Comprehensive Capital Analysis and Review (“CCAR”) stress tests that are designed to ensure that even in the case of a severe recession, significant banks can lend to households and businesses. As repeated by federal bank regulators, the required economic scenarios are not forecasts.

Following the recent financial crisis, the Basel Committee of Banking Supervision (BCBS) set out to “strengthen global capital and liquidity rules with the goal of promoting a more resilient banking sector.” The three pillars include maintaining minimum capital requirements, a supervisory review process and market discipline.

Europe’s Financial Stability Board said Friday (June 7) that higher bank capital requirements put on the books during the financial crisis will remain. When the banks were required to increase their capital back in 2010 they argued it would hurt their ability to keep up their lending pace. In January the U.K.

The Financial Stability Board says Basel III rules have not led to a squeeze of the small business bank lending market, according to reports on Friday (June 7). The FSB announced Friday the findings of its analysis of Basel III regulations on the small business lending space.

The issues, sources said at the time, could be attributed to problems in how CAN Capital reported delinquencies among its SME borrowers, leading the platform to breach agreements with major lenders, like Wells Fargo. It all stems back to 2010 or so, when CAN Capital launched ambitious growth plans to enter into new markets.

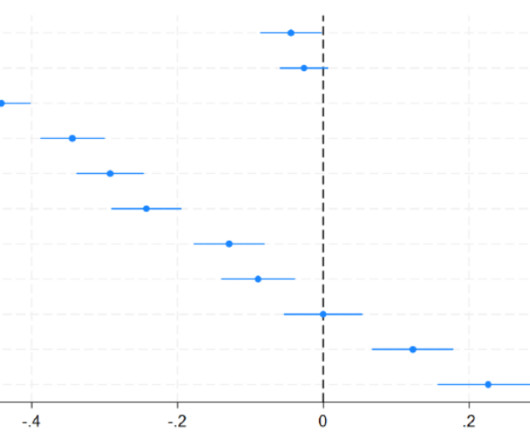

This post investigates whether large and small banks in the UK and US differ in the cyclical patterns of capital positions and credit provision. The reforms aimed to ensure that banks have sufficient capital resources to absorb losses and reduce the cyclical effects of bank capital (and regulation) on the supply of bank credit in stress.

We continue to evaluate capital options and are excited about our industry position,” CEO Anthony Hsieh told Bloomberg. the San Francisco-based peer-to peer lending firm and OnDeck Capital, the New York-based online small business lending company, which went public at the time were already trading down, Housing Wire reported.

Authorities imposed greater capital requirements and other risk mitigation rules on financial institutions after taxpayer bailouts of banks in the EU and elsewhere around the globe during the financial crisis about a decade ago. Regulation is also linked to a decline in profitability among the banks between 2010 and 2016, the report found.

In a recent Sageworks webinar Robert Ashbaugh, senior risk management consultant at Sageworks, discusses High Volatility Commercial Real Estate (HVCRE) lending best practices. Ashbaugh goes on to demonstrate that the default rates for these loans did not peak until about 2009, and the ALLL did not increase until 2010.

The company revealed the funding from an array of backers including National Australia Bank, Royal Bank of Canada, Portag3, and Exhibition Capital. Existing investors CRV, Social Capital, BDC IT Venture Fund and BDC Capital, OMERS Ventures, HarbourVest and OurCrowd also participated, Wave said.

Even some of the more successful CUs have had to curtail lending. The numbers highlight the worst year for the industry, which is fighting with rising regulatory and tech costs, since 2010. Eight credit unions closed in 2018, and they affected an estimated 14,000 people with a collective £25 million in savings.

Toward the start of 2018, analysts began to highlight the potential for venture capital (VC) to embrace the B2B business model. and India drove a surge in FinTech venture capital funding in 2017, and Accenture Financial Services Senior Managing Director Julian Skan pointed to the B2B business model as a significant presence in this trend.

The FDIC paper The Entry, Performance, and Risk Profile of De Novo Banks published in April 2016 reports that the number of de novo bank failures and acquisitions annually has drastically declined since 2010, primarily due to the fact that new bank formations have become nearly inexistent. A low interest rate environment 2.

The unit handles the bank’s corporate lending, M&A advisory services and capital raising operations. It has fallen from the number-two spot in the industry, which it held between 2010 and 2013. The bank’s current Asia-Pacific President Matthew Koder is slated to replace Meissner, according to reports.

Her answer: lack of capital. But in strategic planning retreats that I moderate, community financial institutions insist that they lend to small businesses. The second chart shows the primary sources of capital. Given a community FIs lending proclivities, one would assume that small businesses borrow to finance a building.

The DOJ investigation centered on whether LendingClub had – between January 2009 to September 2010 – misled its FDIC-insured loan originator, WebBank , leading the bank to underwrite over 200 loans that did not conform to the bank’s lending requirements. In 2010, LendingClub added to its war chest with a $24.5

The number of pawn shops in China has doubled to 8,500 since 2010, and the average loan amount has climbed to around $26,000. As of now, the country’s insurance and banking regulator is beginning to draft new rules aiming to toughen up oversight in the pawn shop lending industry, according to sources cited by Bloomberg.

A drop in car loan totals this past quarter indicates that rising delinquencies and threats of litigation are conditioning banks to lend with more caution. percent in 2010. percent in 2010. However, banks aren’t so confident, at least when it comes to car loans. percent in October and a peak of 25.5

According to an announcement , the firm raised $63 million from backers in a funding round led by Victory Park Capital and existing supporters. IZettle has expanded its presence across Europe and Latin America since its 2010 launch and has similarly introduced new services for its SME clients.

This includes global transaction services, small business services, commercial and small business lending, and the changing role of corporate treasury and its impact on meeting the needs of corporate banking clients. On the lending side, US commercial loan outstandings have more than fully recovered from the 2008-2009 financial crisis.

Strategic Horizon and Capital As mentioned, the problem that bank’s often run into when it comes to strategic planning is their time horizon is too short. The fundamental problem is a bank’s implied average life of capital is long, some 18+ years, but their strategic horizon is too short – likely under three years.

In an interview with American Banker earlier this month, Trustar CEO Shaza Andersen said the institution could open its doors as early as this June, with plans to raise up to $50 million in initial capital, the publication said. In a report published last year, the U.S. have emerged to do. have emerged to do. . have emerged to do.

Here, we highlight some of last year’s most successful loan producers in the areas of agriculture, commercial and consumer/mortgage lending. The score combines the average of the bank’s percentile rank for lending concentration and for loan growth over the past year in each lending category. By Ed Avis. Methodology. AGRICULTURE.

We examine the findings from several market reports on small business access to capital, lending, growth and employment. That figure represents a 30 percent increase in borrowing among these SMEs compared to 2010 and a 70 percent increase compared to 2006 figures. billion in loans were taken out by small U.K.

The 2020 Census quantified the growth many residents were already sensing: Austin grew by 33% between 2010 and 2020, earning it the rank of fastest-growing large metro. ANB does “traditional lending in every aspect,” Edlund says, but commercial loans make up the majority of its loan portfolio.

In my previous blog post, I discussed how COVID-19 is impacting the auto lending industry. Today, I want to provide some specific strategies your financial institution can deploy in order to supplement auto loan originations and increase loan volume.

is strong, with the majority citing new technologies, an improving economy and favorable lending conditions as factoring into why they believe today is a great time to be in their position. Researchers pointed to the perception of higher risk among these borrowers as one factor playing into the gap of small business lending.

Economists and government officials continue to cite lack of lending activity as a key contributor to our economic malaise. Much of the standoff revolves around real estate secured lending. of total assets at March 31, 2010 (see link below). dropped 24% from 2007 through the first quarter 2010. Are these more reliable?

Capital rotation is to HELOCs and away from autos. Within autos, the capital rotation is for new cars over used cars. Consumer Credit – Cards There is a shift of capital occurring to the prime tiers of cardholders. Utilization has increased to 22% but materially below the 27% spike in 2010.

For example, a contraction in mortgage lending could reduce consumption by lowering house prices and reduce investment by slowing new housing construction. Figure 3 displays our baseline estimates for a one standard deviation contraction in mortgage lending (67 basis points). standard deviation contraction in mortgage lending.

What if our lending footprint is very small and not affected by macroeconomic factors such as unemployment? It can be challenging to model forecasts for institutions with small lending footprints. Stress Testing: Managing Capital Levels and Credit Risk. A straightforward single or two-factor model can suffice. Keep me informed.

Chart 2 shows that the shock also triggers a substantial and persistent contraction in private banks’ equity capital. This model can solve the comovement puzzle and match the empirically observed rise in credit spreads alongside a sharp decline in bank’s equity capital. The importance of supply-side financial frictions.

Alex Pollack, a resident fellow at The American Enterprise Institute, had a sobering editorial in the March 3, 2010 American Banker. That Act did not permit national banks to lend on real estate. It remained at that level for nearly three decades when real estate lending began its meteoric rise to today’s levels.

Community banks cannot afford to ignore the staggering pace of lending adoption by both individuals and businesses using digital-only platforms from various nonbank technology-based specialty lending firms. Competing and beating FinTech’s digital-platform lenders. By Jonathan Rowe. Core deposits also come at much lower costs.

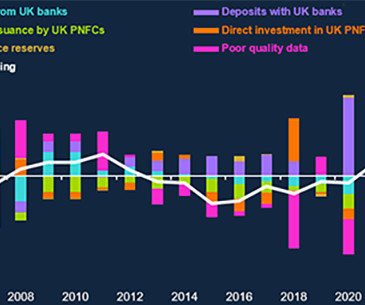

Net lending represents the overall surplus or deficit, and it is theoretically the same whether you look at it from the income or financial account viewpoint. Evolution of the net lending positions of households and corporates The pre-GFC era was a period of strong growth and low inflation , which coincided with a large expansion of credit.

The biggest announcement came as Magento Commerce, spun out from eBay two years ago, got $250 million from Hillhouse Capital, one of China’s largest investment firms. The new capital will help fund global expansion, with focus, as the name implies, on eCommerce. By 2010, Conversica had developed AVA — the automated virtual assistant.

ICBA warns of risks of online marketplace lending models. Online marketplace lenders are a new form of nonbank specialty lending that uses technology platforms to allow Wall Street and individual investors to directly fund loans to consumers and small businesses. Lend exclusively over online peer-to-peer platforms.

capital appreciation and dividends. The lion''s share of their growth, profitability, and capital have come since their re-branding to Open Bank in 2010. share at the end of 2010. Not so over the three years I have been keeping track. This, naturally, eliminated many of the smaller, illiquid FIs. BofI Holding, Inc.

As we scale, it’s becoming increasingly important that we have direct relationships with regulators,” said Jacqueline Reses, who leads Square Capital and will be the chairman of the bank. Square already has an SMB lending arm – Square Capital – which it operates through a deal with Utah-based Celtic Bank.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content