This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

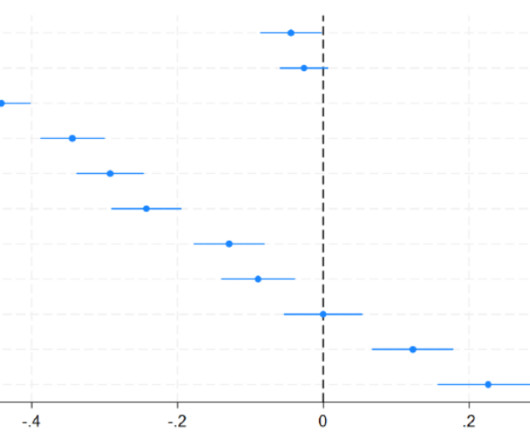

This post is an example of issues considered under the Prudential Architecture Theme which focuses on the evolving regulatory structures and fresh strategic issues for regulators and supervisors. Loan forbearance features prominently among those interventions by lenders and/or regulators. For example, a coefficient of about -0.4

Federal bank regulators work together to design Comprehensive Capital Analysis and Review (“CCAR”) stress tests that are designed to ensure that even in the case of a severe recession, significant banks can lend to households and businesses. As repeated by federal bank regulators, the required economic scenarios are not forecasts.

Nonbank lending – also known as “ shadow banking ” – has seen its assets hit $52 trillion, despite the fact that the sector poses significant risks. In fact, the country’s regulators have gotten tough in recent years, causing outstanding loans in the sector to fall to ¥61.3 While the U.S. trillion ($9.1

securities regulator is having trouble with rating agencies because it doesn’t have the tools or specific knowledge it needs to analyze huge amounts of rating data, according to a report from Reuters. Those entities and their elevated ratings of mortgage-backed securities, analysts say, were gasoline for the U.S. housing bubble fire.

If the CFPB was so concerned about fees charged by banks, perhaps they should perform an analysis of over regulation that is a key contributor to fees charged by banks? Regulators must not have read that article. What do regulators think will happen? I cannot lay the sole blame at the feet of regulators.

The Financial Stability Board says Basel III rules have not led to a squeeze of the small business bank lending market, according to reports on Friday (June 7). The FSB announced Friday the findings of its analysis of Basel III regulations on the small business lending space. Some regulators aimed to mitigate that impact.

Interest rates plummeted as the Fed held the federal funds rate at zero in the hopes of stimulating lending in an environment where credit went from dangerously free-flowing to dangerously non-existent in the span of a few months. The New Subprime Lending Path. Citigroup’s auto lending unit has been nearly entirely sold off.

One of the topics continually making headlines in banking today is the cost of regulation. A popular opinion, brought to the forefront last week by a Harvard University report , is that these regulations are imposing a significant burden on small financial institutions such as community banks and credit unions.

Online consumer lending – in a variety of forms – has grown explosively over the last decade. In 2010, digital lenders originated $249 million in unsecured personal loans, and by 2016 that number had grown ninety-fold. So how did one branch of the Fed end up on such a different page from their counterparts? Cleveland’s Dark Outlook.

The Association for Financial Markets (AFME) in Europe wants regulators to curb the development of aggressive bank regulation, according to Reuters reports on Thursday (April 12). Analysis found the annual cost of regulation costs $37 billion for 13 banks combined, amounting to 39 percent of total capital markets expenses in 2016.

Klein The Federal Reserve Board indicated it is scrutinizing mortgage loan pricing models that comply with Regulation Z but nonetheless, in the view of the Board, significantly increase fair lending risk. Fair Lending Mortgages disparate impact LO Comp Rule mortgage lending origination' here and here.

Reuters , citing the regulator, reported it found the negative impact on small business lending was short in nature, and that there is no need to change the rule. When the banks were required to increase their capital in 2010, they argued it would hurt their ability to keep up their lending pace. In January, the U.K.

percent of lenders were unprofitable — the largest number since 2010. Banks like Chase and Wells Fargo have set about tightening the reins on their lending practices, looking to minimize the risk during the times of economic uncertainty. billion, Reuters wrote. Banks saw a $1.2 percent increase in commercial and industrial loans.

In a recent Sageworks webinar Robert Ashbaugh, senior risk management consultant at Sageworks, discusses High Volatility Commercial Real Estate (HVCRE) lending best practices. Ashbaugh’s presentation begins with a quick summary of why regulators care about HVCRE. How did we get here? What are HVCRE loans?

Even some of the more successful CUs have had to curtail lending. The numbers highlight the worst year for the industry, which is fighting with rising regulatory and tech costs, since 2010. Eight credit unions closed in 2018, and they affected an estimated 14,000 people with a collective £25 million in savings.

Reuters , citing the regulator, reported it found that the negative impact it had on lending on small companies was short in nature and as a result, there is no need to now change the rule. When the banks were required to increase their capital back in 2010 they argued it would hurt their ability to keep up their lending pace.

branches and agencies of foreign banks indicated that most are forecasting tougher standards for all types of lending due to an increased expectation of default as risk tolerance drops along with the value of assurances. . Proposed changes would loosen those regulations. Demand is expected to stay steady.

CFPB 1033 open banking requires financial firms to ease personal financial data access for consumers CFPB first proposed the rule in the Federal Register on October 31, 2023, accepted public comments on the regulation though December 29, 2023, then issued its final rule November 18, 2024.

Researchers said about 72 percent of market volume in 2016 can be traced back to demand for lending options among startups and small businesses, up from 50 percent the year before. Peer-to-peer businesses lending was 2016’s largest alternative finance market segment, which saw 36 percent year-over-year growth.

High street lender recently failed to convince regulators it could be trusted to hold less cash against its mortgage risks Metro Bank is considering raising hundreds of millions of pounds from investors, weeks after the high street lender failed to convince regulators it could be trusted to hold less cash against its mortgage risks.

The number of pawn shops in China has doubled to 8,500 since 2010, and the average loan amount has climbed to around $26,000. As of now, the country’s insurance and banking regulator is beginning to draft new rules aiming to toughen up oversight in the pawn shop lending industry, according to sources cited by Bloomberg.

That’s because as the panel of experts assembled at Innovation Project 2017 last week at Harvard pointed out, the consumer who makes use of short-term lending: Likes them, Needs them and. Those regulations as currently proffered, they said, dictate the products on offer, which in turn limits the degree to which they can be innovated.

I’m thinking of [the refi wave] more like a partial offset to [lending margin] pressure, as opposed to a meaningful earnings boost.”. Transactions fees from refinancing won’t be sufficient to offset the lower lending margins, analysts said.

These concerns are often dismissed by consumer advocates with the argument that banks and credit unions will increase their small-dollar lending if other providers leave the market due to interest rate caps. Among the services examined by the GAO in the report is small-dollar lending.

The authority would require a change in legislation, but Kraninger argues that it would help the agency spot wrongdoing more quickly, especially when it comes to fair lending practices. Whistleblowers would only be paid if their tips led to penalties against perpetrators. “We

In addition to the fine, the regulator will charge Grab $3,500 daily until it rectifies the situation. We maintain our position that we have complied fully with the Competition Act 2010,” a Grab spokeswoman told the news outlet. MyCC decided that Grab used its marketplace position to thwart any competition.

Specifically, the report examines how the CFPB has (i) managed the reorganization of its Office of Fair Lending and Equal Opportunity and related risks during 2018, (ii) monitored and reported on its fair lending performance, and (iii) used new HMDA data fields to analyze and support its fair lending activities. Background.

Financing of all sorts was on the downswing, and SMB owners began dipping into their own piggy banks before seeking a lending agreement. The Economic Growth, Regulatory Relief and Consumer Protection Act loosened some of the regulations on small financial institutions, including community banks whose customers included many small businesses.

The DOJ investigation centered on whether LendingClub had – between January 2009 to September 2010 – misled its FDIC-insured loan originator, WebBank , leading the bank to underwrite over 200 loans that did not conform to the bank’s lending requirements. In 2010, LendingClub added to its war chest with a $24.5

The reforms aimed to ensure that banks have sufficient capital resources to absorb losses and reduce the cyclical effects of bank capital (and regulation) on the supply of bank credit in stress. Additionally, regulators in various jurisdictions have been trying to create simpler (but not weaker) regulatory frameworks for small banks.

Many of those schools are now being investigated by the CFPB for potentially fraudulent lending practices. As ACICS has repeatedly and accurately explained, the accreditation process simply has no connection to a school’s private student lending practices.”. Put simply, this post-hoc justification is a bridge too far!”

In today’s mixed up, muddled up, shook up world, a business model that encourages — and even desires — some level of repossession can provide substantial profits to the lender (depending on state regulations). Currently, lenders can typically get more money from the sale of a repossessed vehicle at auction than is owed by the borrower.

Economists and government officials continue to cite lack of lending activity as a key contributor to our economic malaise. Much of the standoff revolves around real estate secured lending. of total assets at March 31, 2010 (see link below). Regulators are slightly schizophrenic on the subject. Are these more reliable?

Codes of conduct are on the rise, and have a focus on reputational risk as well as on harassment When more than 1,300 lending bosses, regulators and MPs descended on Grosvenor House hotel on Park Lane in London for a black-tie dinner in late February, they arrived informed.

Mortgage borrowers are also a very different group than they were nine years ago at the outset of the financial crisis — in part because of tougher lending standards mandated by federal regulators. And the shift in mortgage lending mirrors a shift in the lending picture in general when it comes to who holds the majority of U.S.

Government Accountability Office (GAO) analyzed lending among community financial institutions (FIs) between 2001 and 2017, and concluded that these FIs “are important sources of credit to small businesses.” In a report published last year, the U.S. have emerged to do. . have emerged to do.

Perhaps the most significant practical impact of SCALE is that by introducing it, regulators have clarified that financial institutions have the space to bring in external information like peer information for their computational estimates. It can be challenging to model forecasts for institutions with small lending footprints.

For example, a contraction in mortgage lending could reduce consumption by lowering house prices and reduce investment by slowing new housing construction. Figure 3 displays our baseline estimates for a one standard deviation contraction in mortgage lending (67 basis points). standard deviation contraction in mortgage lending.

2155, directs the CFPB to implement an exemption from the mandatory escrow account requirement for higher-priced mortgage loans (HPMLs) under the Truth in Lending Act (TILA) and Regulation Z for certain insured credit unions and insured depository institutions. This time period would also apply to the current exemption.

Regulators, investors, and other stakeholders will be watching and listening for updates on the impacts of the accounting change. We were able to go back and gather all the necessary data points for the cohort methodology back to 2010, which will give us a full decade of data by the implementation date,” she said. Learn More.

ICBA warns of risks of online marketplace lending models. Online marketplace lenders are a new form of nonbank specialty lending that uses technology platforms to allow Wall Street and individual investors to directly fund loans to consumers and small businesses. Lend exclusively over online peer-to-peer platforms.

Community banks cannot afford to ignore the staggering pace of lending adoption by both individuals and businesses using digital-only platforms from various nonbank technology-based specialty lending firms. Competing and beating FinTech’s digital-platform lenders. By Jonathan Rowe.

When the Truth in Lending Act became law in 1969, the Federal Reserve Board soon thereafter promulgated its implementing regulation, Regulation Z. The Fed subsequently began using Official Staff Commentaries for the other consumer finance regulations that it was charged with interpreting.

An industrial bank is an FDIC-insured depository institution that is generally subject to the same banking laws and regulations as any other bank charter type, with the important exception of the Bank Holding Act of 1956. Square already has an SMB lending arm – Square Capital – which it operates through a deal with Utah-based Celtic Bank.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content