This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Last Friday, February 12, while many bankers were preparing for a long 3-day weekend or perhaps making preparations for Valentine’s Day celebrations, the Federal Reserve Board released the hypothetical scenarios for its 2021 bank stress tests. The Federal Reserve has both a Baseline Scenario and a Severely Adverse Scenario.

The COVID-19 pandemic has challenged the economic and labor markets, impacting all businesses regardless of their size. If your organization is looking to capitalize on cloud technology in 2021, here are a few trends to keep in mind. The Public Cloud Market Will Surge.

Their flexibility, low premia and underlying leverage appeal to all market participants ranging from conservative investors hedging against intraday market volatility to aggressive traders speculating for quick profit generation. The improved market conditions have encouraged both market participation and innovation.

The migration of the procurement and purchasing process to seller platforms and digital marketplaces will be a driving force into 2021, B2B payment leaders agree, and this trend will drive further change in both payer and payee expectations. For some B2C firms, that meant expanding into the B2B market.

Thus far in 2021, as of this writing, there have been 27 SPAC IPOs, according to the site, which have generated $6.6 In only one example noted in this space, as reported this week , tech startup Social Finance (SoFi) is closing a merger deal with blank-check firm Social Capital Hedosophia Holdings Corp. billion in gross proceeds.

The market turmoil of 2020-2021, along with an unprecedented surge that has renewed a focus on retail investors, has pushed direct investing platforms into the spotlight. However, during the pandemic we witnessed the union of social (media, communities and group action) and capital (saving and trading) as….

Two deals that were very much needed in the market were Candescents (the artist formally known as NCR Voyix) acquisition by Veritas Capital in September for $2.45 Fast forward to September, and in steps Veritas Capital. Together, both deals show that digital isnt hitting a lull, but rather ramping up speed for future growth.

B2B FinTech startups have stepped into 2021 with a bang, as industry players raised more than $910 million in combined funding. With the funding, Yesler plans to invest in its marketing and engineering teams. In a statement, the company's Group President Suhail Sameer said the debt capital will be key to its lending operations.

Takeaway 1 Financial institutions that invested in technology in 2020 are using it to increase the loan portfolio in 2021. Growing loans, earnings are banks' top challenges in 2021. The top banking challenges in 2021 are growing loans and earnings, according to Independent Banker’s recent 2021 Community Bank CEO Outlook survey.

The Office of the Comptroller of the Currency (OCC) recently released the economic and financial market scenarios that will be used in the upcoming stress tests for covered institutions. Equity market volatility, as measured by the Chicago Board Options Exchange Volatility Index (VIX), declines in 2022 by about 6.5 to hover around 2.50

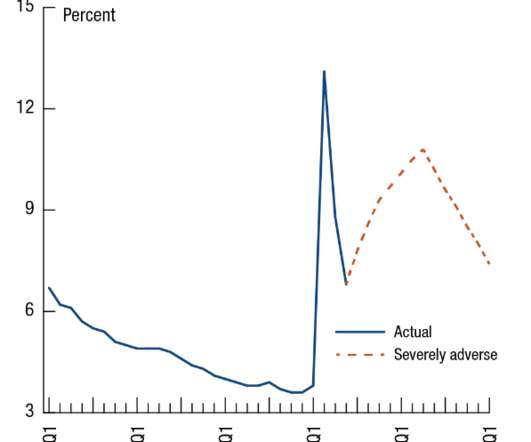

The Fed’s Comprehensive Capital Analysis and Review (“CCAR”) stress tests are designed to ensure that large banks can lend to households and businesses even in a severe recession. The 23 large banks tested remained well above their risk-based minimum capital requirements. Test Results.

Two deals that especially took us by surprise were Candescent’s (the artist formally known as NCR Voyix) acquisition by Veritas Capital in September for $2.45 Fast forward to September, and in steps Veritas Capital. Together, both deals show that digital isn’t hitting a lull, but rather ramping up speed for future growth.

The front office is screaming down to the Settlement Office, “Operations, we need more capital!” Any operations team that has dealt with a stock loan trading desk can contest the inherent friction between providing more available securities to the desk and reliance on settlement cycles and market constraints.

A combination of relatively hawkish July FOMC minutes and softer global economic reports gave risk markets a slightly negative tone last week. The more hawkish Fed view showed up in the currency markets as the U.S. The labor market continues to recover as initial jobless claims continue to decline. Last Week.

The volatility in rate markets last week was one for the ages. The week was a tale of two markets. The first was the continuation of the punishing rally that has burned shorts and frustrated yield chasers.

The week began with the continued unwinding of the massive, long-dated Treasury short positions that have roiled the markets and, in large part, caused the 10-year to revisit technical lows in yields, getting as low as 1.41% on Tuesday. Then, October CPI came on Wednesday, and the market went from student body right to student body left.

Both risk and Treasury markets spent most of last week guessing what Fed Chairman Powell was going to say when he spoke at the annual Fed summit at Jackson Hole, WY, then reacting to the actual address on Friday. Chairman Powell provided what can be called a “dovish taper”.

In the rates markets, more and more participants have begun to accept as fact that the inflationary pressures being experienced in all corners of the economy and most of the world aren’t going away anytime soon. It was a tale of two worlds last week.

While equities rallied Monday after the steep selloff on Black Friday, you could feel that the market was spooked and ready to sell-off. Yet another wild one, last week. The week started with further angst over the new COVID-19 variant, Omicron.

The Treasury market survived another supply deluge as the Treasury auctioned off approximately $180 billion in debt (two-year, five-year, and seven-year). Last Week: Last week saw the resumption of the rotation trade in equities as large-cap value stocks outperformed small-cap and growth stocks.

Last week, 2s-30s flattened 20 basis points as the market began to price in inflationary pressures lasting for a period that is more than transitory. Another wild week as we continue to live in “interesting times”. The Treasury yield curve steepening theme suddenly reversed course.

Equity markets decided to look at the glass as half full, last week—keying in on initial reports that the Omicron Covid variant might be very contagious but not as lethal as Delta—and got their rally on. The tech-heavy NASDAQ managed to defy the narrative that it trades with positive interest rate duration, heading up 3.6%

Last Week: In an action-packed week, the equity markets continued the big equity rotation trade where the high-flying “Big Tech” and “Fintech Disrupter” stocks lost more ground to value stocks, such as banks. A good example of the activity could be found in two Exchange Traded Funds.

Meanwhile, Friday’s huge non-farm payroll miss sent shivers through risk markets. The Commodity Research Bureau Raw Material Index ended the week less than one percent from its all-time high.

Impervious to bad news, such as the spread of the “Delta Variant,” further Fed speak on tapering, warnings of impending doom from market sages, and continued signs of inflation, the stocks party on. Last Week: Equities continued to grind higher with the S&P 500 managing to set new all-time highs every day of the week.

While 2020 started out as a difficult year for Municipal Bonds, those investors that were nimble and not ruled by fear, ended up having a good—if not a great—year. The spike in Municipal Yields during the first quarter ended up being a significant buying opportunity for individual bonds and structured products.

Robinhood Markets , the popular stock trading app, is working with Goldman Sachs for its initial public offering (IPO) preparations, which could value the company at $20 billion, Reuters reported. The IPO could come out next year, Reuters reported, citing sources, who also said the exact timing would be subject to market conditions.

The municipal bond market took a wild ride in the first half of the year to near-historic levels of richness versus Treasuries that is rarely seen, and the environment is ripe for the second half of the year to take it even further.

Understanding broad market trends and the specific forces affecting bank and credit union portfolios can guide institutions decisions while helping them prepare for examiner scrutiny of CRE risk , according to a recent Abrigo webinar, Being strategic with your CRE. Senior housing and aging office buildings add to the pressure.

The sell-off in rates has been orderly, so far, as we have not seen much forced duration selling yet from the mortgage market. The 10-year Treasury jumped 13 basis points, while the two-year remained firmly anchored.

How can community financial institutions thrive in 2021? Acquisitions allow organizations to spread costs across a larger asset base, recognize synergies within business lines, reduce staff, and consolidate branches in overlapping markets. Community Bank Outlook: Challenges and Opportunities in 2021 and Beyond. SBA Lending.

The combined company, to be led by Metromile CEO Dan Preston , will have a pro forma marketcapitalization of approximately $1.3 Investors Social Capital, Hudson Structured Capital Management, Miller Value, Clearbridge and Mark Cuban have committed to investing $160 million through a private placement of INSU II Class A common shares.

Notable market participants such as Jeff Gundlach and David Einhorn disagree. On Wednesday, the Federal Reserve FOMC meeting showed a Fed that has every intention to let the economy run hot, even as inflationary readings pick up. The Fed views the spikes we are seeing in commodities and other production inputs as “transitory.”

There is a lively debate about whether and how capital regulations for banks and insurers should be adjusted in response to climate change. Incorporating climate-related risks into the capital regime will require a reliable methodology to measure these risks. Marco Bardoscia, Benjamin Guin and Misa Tanaka.

It appears that real money buying and fast money short-covering of Treasuries has abated as supply continues to flood the market. The Treasury conducted massive two-year, five-year, and seven-year auctions, which were received fairly well.

Independent Banker’s annual listing top-performing community banks of 2021 alongside interviews with some of the winners. On the next pages, you’ll find our listings of the top-performing community banks of 2021 alongside interviews with some of the winners. Capital Community Bank. Illustration by Eight Hour Day.

The highlight of the week was the July FOMC meeting and announcement. Importantly, there was some language change that acknowledged the continued progress made by the economy and that they are now actively looking at the data to decide when to begin tapering.

Another week, another new all-time high for stocks. Equities plunged at the beginning of the week. The S&P 500 dropped 1.6% on Monday as risk assets reacted to the very real risk of the COVID-19 Delta variant causing havoc and snuffing out the recovery.

Last Week: Another strong week for equities as new all-time highs were set yet again for the S&P and NASDAQ. President Biden’s inauguration went off without a hitch and some confidence rose that the new administration will attack the virus with a more coordinated federal effort and aggressively push the $1.9 trillion stimulus-relief package.

Treasury auctioned off three-year, 10-year, and 30-year notes for a grand total of $126 billion in new issuance. The highlight was the stupendous showing of the 10-year note on Wednesday. The new note stopped through pre-auction yield three basis points, while all the measures of auction performance were very solid. year-over-year increase.

While the major stock indices continued to grind higher and Treasury yields drifted in a very tight range, last week was still quite interesting. Retail investors, the new 800-pound gorilla, drove their new love interest, AMC, up 83% for the week. At one point on Tuesday, the stock was up over 140% from the prior week’s close.

It was quite an ugly week for just about everything but oil and bitcoin. Stocks were down sharply, giving their worst monthly performance since March 2020. High-Yield corporate debt showed some signs of weakening as well. It feels like the world is waking up to the real possibilities of stagflation.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content