This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

How can community financial institutions thrive in 2021? Community banks provide unique and important banking services for their customers, but they also face significant obstacles. Takeaway 1 Community banks play an important role in the economy and their communities, but they face significant obstacles.

Takeaway 1 Financial institutions that invested in technology in 2020 are using it to increase the loan portfolio in 2021. Growing loans, earnings are banks' top challenges in 2021. The top banking challenges in 2021 are growing loans and earnings, according to Independent Banker’s recent 2021Community Bank CEO Outlook survey.

With consumer expectations seeming to evolve faster every year, community banks could consider partnering with a fintech to keep up with technological innovation. Swashbuckling, nimble, well-funded and unapologetically entrepreneurial, fintechs are offering innovations that allow community bankers to dream big in a host of ways.

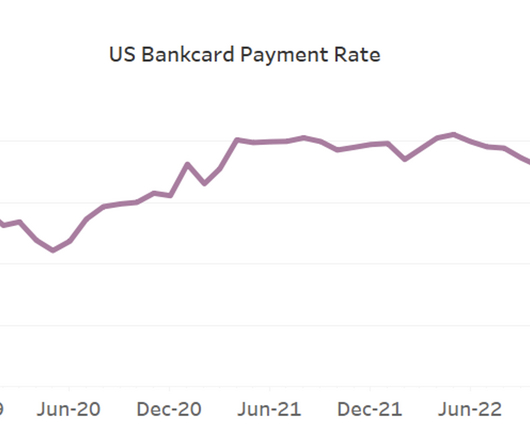

Deposit costs and liquidity remain a challenge for some community banks as competition for core funding remains intense. The graph below compares the liquidity ratio for community banks (under $10B in assets) and banks over $100B in assets. This deposit and loan repricing mismatch caused NIM pressure at community banks.

Over three quarters of community banks did not close a single branch, Wipfli survey reveals Community Banking Feature3 Feature RiskManagement Branch Technology/ATMs Financial Research Payments.

Community banks have a choice about addressing the problem: Remain vulnerable or be vigilant. Fraud and cybercrimes continue to increase, causing challenges for community banks. But there’s plenty community banks can do to meet this challenge. Fraud and cyber attacks are on the rise, and at great expense to the industry.

If 2020 was the year no one expected, 2021 was a year of resetting expectations. Between a smoldering pandemic, the divisive political landscape and strong, albeit uneven, growth, there was a lot to account for in 2021, and some uncertainty remains. Janet Silveria, Community Bank of Santa Maria. What changes will 2022 bring?

Takeaway 2 Examiners' focus is on riskmanagement related to products and services , especially those involving complex technologies like AI. First, they must evaluate whether their institution is prepared to insert AML riskmanagement procedures into the transaction process to match the speed FedNow can offer.

However, community financial institutions can incorporate the new scenarios for their own stress tests to help determine how their capital levels will fare in severe economic situations. Prudent stress testing as a riskmanagement tool helps the enterprise see where the potential pitfalls are in their plans.

Measuring Interest Rate Risk Can Vary by Institution Interest rate risk measurement plays a key role in ensuring an institution's safety and soundness. Would you like other articles on asset/liability management in your inbox? FDIC) noted in its 2021Risk Review. FDIC) noted in its 2021Risk Review.

Takeaway 3 Community banks have seen less volatility in noninterest income, and many are still eyeing growth across the category. Lawmakers and the regulatory community have taken notice of the increase in bank service charges and fee income and have responded, specifically regarding overdraft fees. Community banks target growth.

But impulse buying – whether at home or in business – can result in waste, so think carefully about areas of your bank or credit union that could benefit next year from a small investment as 2021 draws to a close. Indeed, deposit levels to transaction accounts among community banks exploded 74% to $896.5 Credit RiskManagement.

Small business lending is also a prominent line of business for many financial institutions, especially those driven by a mission to help their communities thrive. While small business loans inherently benefit business owners, they also benefit communities, according to 2021 research for the SBA.

Generally, small business loans benefit business owners, they also benefit communities, according to 2021 research for the SBA. Starting with loans originated in January 2021, delinquency rates begin to fall and even dip below historical averages. At the same time, 59% pursued credit to meet operating expenses.

The OCC, FDIC, and Federal Reserve Board have issued a guide that is intended to assist community banks in conducting due diligence when considering relationships with financial technology (fintech) companies (Guide). Riskmanagement policies, processes, and controls. Legal and regulatory compliance.

If the system is not efficient and manual data entry contributes to increased risk, a greater headcount is not the solution. The benefits of a user community Businesses always pursue growth and improvement. However, many clients evaluated an internally developed system before ultimately acquiring loan review automation.

The root cause of Silicon Valley Bank’s (SVB) failure is poor riskmanagement – plain and simple. Bankers need to understand and manage their business on the fair value of assets and liabilities instead of managing their business on net interest margin and the amortized historical cost of assets and liabilities.

From economic forecasts to company culture, there were important takeaways for all community financial institutions. . Millennium Bank, like many community financial institutions, is heavily concentrated in commercial real estate (CRE). Drive Growth. Understanding the current state of banking and future expectations.

Small business lending is also a prominent line of business for many financial institutions, especially those driven by a mission to help their communities thrive. While small business loans inherently benefit business owners, they also benefit communities, according to 2021 research for the SBA. economic ecosystem.

In June 2021, the White House released the first rendering of the National Strategy for Countering Domestic Terrorism 1 , a strong indicator that it is time for us all to be paying closer attention to this matter. See Part I: Implications for Community Financial Institutions. Stay up-to-date on the latest FinCEN priorities.

The flow of approvals is good news for community financial institutions that have been working since late March to provide $525 billion in funding to U.S. Community financial institutions with less than $10 billion in assets had provided nearly half of all PPP funding by the time the program closed Aug. Lending & Credit Risk.

They are routinely experiencing processes that add costs, delay turnaround times, and can lead to inconsistency in pricing and riskmanagement. Many community bankers expect a recession will start by at least mid-2021, according to the most recent Community Bank Sentiment Index.

Even if community businesses don’t end up utilizing the federally guaranteed loans , many small businesses have heard of SBA loans and want to explore them. During Abrigo’s recent ThinkBIG Conference, credit underwriting and loan portfolio riskmanagement trainer and consultant Michael Wear , CRC , of 39 Acres Corp.

Even if community businesses don’t end up utilizing the federally guaranteed loans , many small businesses have heard of SBA loans and want to explore them. During Abrigo’s recent ThinkBIG Conference, credit underwriting and loan portfolio riskmanagement trainer and consultant Michael Wear , CRC , of 39 Acres Corp.

Early adopters are earning prestige while investors and a hoard of community banks explore the opportunity to tap into this new source of revenue. While customer relationships are being redefined by fintechs, there will always be a place for community banking. Now is the time to create a BaaS strategy.

Last year, community bank loan producers were faced with both record-low interest rates and a glut of deposits. But as they always do, they came through for individuals and businesses in their communities with a combination of personalized service and prudent riskmanagement practices. Photo by Linkes Photography.

When it comes to supporting outliers in the Las Vegas community, Lexicon Bank knows how to play its cards. Lexicon Bank didn’t wait long to make a splash, sponsoring the 2021 World Series of Poker. But as a community bank that is there to serve the gaming hub of Las Vegas, Lexicon Bank welcomes these players with open arms.

The paper, “ Bank Monitoring with On-Site Inspections," will be presented later this month at the Community Banking in the 21st Century Research and Policy Conference. As of the fourth quarter of 2021, banks had total construction lending of $403 billion, the study said. Stay up to date on credit risk. Lending & Credit Risk.

The ABA stated in its October 2021 State of Digital Lending report that “baby boomers, who until 2020 lagged in digital adoption, upped their online game, with 68 percent skipping human interaction to make a decision about banking products, up from 55 percent before the pandemic.” Lending & Credit Risk. Portfolio Risk & CECL.

It has become crystal clear that digital transformation is now the largest technology initiative for regional and community financial institutions. Maybe this is the new reality for community bankers, but Cornerstone Advisors is seeing little evidence that they’re serious about implementing a comprehensive digital strategy.

AmTrust recently worked with one community bank client that was the target of a ransomware attack that shut down its branches for two weeks. One of the biggest benefits of a cyber policy, especially for a smaller community bank, is access to experts,” says Gentile. That has been the exact opposite of my experience.

Effective fraud riskmanagement includes detection and fraud monitoring that should consider customer or member history and behavior. billion was lost to fraud through social media between January 2021 and June 2023. At the same time, it is important not to deter clients from using digital banking methods for daily transactions.

In a recent Fortune survey, 55% of corporate executives said they expect to return to 2019 capital spending levels sometime in 2021. Community-based institutions have unique circumstances (and personal viewpoints) that impact how they see the world in the future and what planning will look like for them. RiskManagement.

For 2023, banks need to prioritize interest rate riskmanagement and credit accuracy as a top priority. Many community banks have an inherent strategic advantage in bringing a new product to market faster than a national bank, yet they squander their position. That market share has come mainly from regional and community banks.

Banks and credit unions had to fundamentally change their delivery, support and relationship management models at scopes and speeds that were unheard of. And how did community banks and credit unions respond to the COVID craziness? Expect more cost-driven MOEs in 2021! Bad things about the banking industry. Bravo Brett and team!

Not the financial industry’s “Troublemakers ” – those regional and community banks, credit unions and supporting fintech entrepreneurs who continue to engage customers and communities and find niches that keep the grassroots of our country’s financial system alive and kicking. We are in awe. Seriously in awe.

In a recent survey by the National Association for Business Economics, 74% of economists who responded expect a recession by the end of 2021. Regulatory communities and auditors want to see that CECL and stress testing remain as consistent as possible across the organization. According to economists, a recession is looming.

Comments on the RFI must be received by June 1, 2021. Augmenting riskmanagement and control practices. The agencies observe that the potential risks associated with using AI are not unique to AI, such as creating operational vulnerabilities and consumer protection risks (fair lending, UDAAP, privacy).

But as the prevalence of security breaches grows, so do the opportunities for community banks to position themselves as guardians of their customers’ personal data through compliance, technology and relationship building. By Katie Kuehner-Hebert. Data privacy and security is a hot topic and is only getting hotter. Bob Hickok.

From TBML to BNPL to NFTs, 2021 found fraud and financial crime professionals dealing with a plethora of new challenges and criminal schemes. Darryl Knopp wrote: For banks with their own BNPL offering, a multi-layered approach to riskmanagement and fraud protection is critical. Here are excerpts.

Sam Weller joined us in November, 2021 and has a strong financial background. The 10-year US Treasury ended 2021 at a yield of 1.51%. At the end of 2021, the 2-year US Treasury was yielding.73% However, after a strong Q4 2021, where real GDP grew +6.9%, this negative growth rate may be a sign of things to come.

in real final sales, which is very weak compared to +8% to +9% in the first two quarters of 2021. 3% in January, which was the first monthly decline since the beginning of 2021. in the fourth quarter of 2021. GDP for all of 2021 was +5.7%, following a year of decline in 2020 of -3.4% The CPI started 2021 at +1.4%

from November 2021 to November 2022) and the unemployment rate is expected to rise to 4.6% For example, the average interest rate on credit cards accruing interest in Q4 2022 was 20.40% compared to 16.44% in Q4 2021 (Source: Federal Reserve G.19 compared to December 2021 with average monthly spend staying flat.

Maybe everyone will forgive the Fed and people like myself in 2021 for initially thinking inflation would be “transitory” because of supply shocks. DLJ 06/30/24 Dorothy Jaworski has worked at large and small banks for over 30 years; much of that time has been spent in investment portfolio management, riskmanagement, and financial analysis.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content