This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

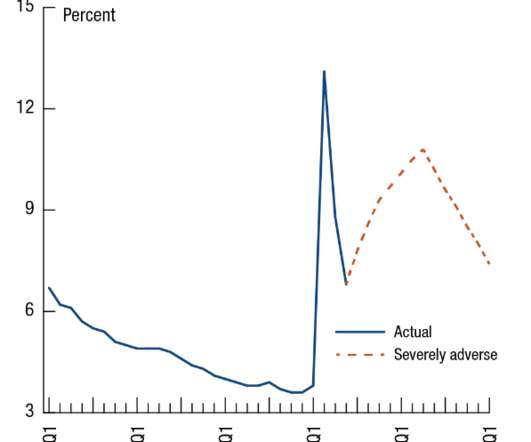

Federal bank regulators work together to design Comprehensive Capital Analysis and Review (“CCAR”) stress tests that are designed to ensure that even in the case of a severe recession, significant banks can lend to households and businesses. As repeated by federal bank regulators, the required economic scenarios are not forecasts.

Short Capital? SVB Financial had Tier 1 risk-based capital of 15.40% as of December 31, 2022, over 80% higher than the 8.50% regulatory required ratio. Including reserves, the parent company had Total risk-based capital of 16.18%, more than 50% higher than the required ratio of 10.50% for large banks. Tier 1 leverage 8.11

The Stress Test Scenarios for Big Banks Are Useful for Smaller Institutions' Own Tests Banking regulators recently released the 2022 scenarios for upcoming stress tests by the biggest banks. The 2022 stress test scenarios provide a blueprint for community banks and credit unions to get started on their own stress tests.

Speaker: William Hord, Vice President of ERM Services

The end result is the ability to streamline your allocation of capital and resources. August 11, 2022 at 11:00 am PDT, 2:00 pm EDT, 7:00 pm GMT In this webinar, you will learn how to: Outline popular change management models and processes. Organize ERM strategy, operations, and data. Determine impact tangents.

With 100+ public banks reporting, we have more than a representative sample to see 2Q 2022 bank earnings trends and derive some operational insights on bank performance. We used the S&P Global database, earnings releases, and investor calls to gather the first hundred banks releasing 2Q numbers as of 8/2/2022.

Blog posts to help your asset/liability management (ALM) staff strategize for the future These ALM posts were the most popular in 2022. Navigating a rising-rate environment, leveraging core deposit strategies, and pricing loans effectively were top of mind for asset/liability management (ALM) staff in 2022. For rookies and experts.

The Fed’s Comprehensive Capital Analysis and Review (“CCAR”) stress tests are designed to ensure that large banks can lend to households and businesses even in a severe recession. The 23 large banks tested remained well above their risk-based minimum capital requirements. Test Results.

Following CompatibL’s recent win at Risk.net’s Markets Technology Awards 2022, Alexander Sokol spoke about the advantages of the new machine learning models for portfolio validation and risk management. It aims to reduce the reliance on pre-pandemic historical data and to help capital markets firms manage their market risk more effectively.

In 2020, the Federal Reserve found that large banks were generally well-capitalized under a range of hypothetical events. The Fed’s Comprehensive Capital Analysis and Review (“CCAR”) stress tests are designed to ensure that large banks are able to lend to households and businesses even in a severe recession.

Seeking additional arrows in their quiver against large bank failures, on October 14, 2022, the Federal Reserve Board (FRB) and Federal Deposit Insurance Corporation (FDIC) published an Advance Notice of Proposed Rulemaking (ANPR). Current Capital Requirements. The current long-term debt calibration for U.S.

It’s 2022, and it seems all the rage in media and digital asset news is surrounding non-fungible tokens (NFTs) and the Metaverse. And today, OpenSea, an NFT marketplace that launched in 2017 and completed a Series C funding round for $300 million in January 2022, is valued at $13.3 Let’s put that in context.

In 2022, FTX broke ground on its new headquarters in Nassau, the country’s capital. In April 2022, Nassau, the capital of the Bahamas, hosted the invitation-only Crypto Bahamas Conference. Attracting Crypto Corporations. Crypto Conference.

We had shock and awe in the bond markets last week as Fed presidents and governors took to the airwaves stating they were amenable to multiple 50 basis point hikes at the remaining meetings in 2022 and beyond. Louis Fed President James Bullard when he called for one 50 basis point hike in 2022.

In rates, a 100% probability of four FOMC rate hikes in 2022 is priced into the front of the yield curve with some, like Goldman Sachs, predicting a hike at every meeting starting March 16 or seven in total. Last week was simply brutal. Meanwhile, the Treasury yield curve flattened as signs point to a slowing recovery.

Devoted to continuous advanced technology research and product innovation, CompatibL is proud to be recognized as one of the world’s best providers of risk management solutions, advanced analytics, and model validation services that help capital markets organizations better understand and reduce financial risks.”.

There is a lively debate about whether and how capital regulations for banks and insurers should be adjusted in response to climate change. Incorporating climate-related risks into the capital regime will require a reliable methodology to measure these risks. Marco Bardoscia, Benjamin Guin and Misa Tanaka.

According to the Federal Deposit Insurance Corporation (FDIC), in 2000, there were 8,000 commercial banks in the United States, but as of March 2022, that number had dwindled to 4,194 operating physical bank branches. Another example is Eno , Capital One’s virtual assistant.

The combined company, to be led by Metromile CEO Dan Preston , will have a pro forma market capitalization of approximately $1.3 Investors Social Capital, Hudson Structured Capital Management, Miller Value, Clearbridge and Mark Cuban have committed to investing $160 million through a private placement of INSU II Class A common shares.

What changes will 2022 bring? And as local economies continue to stabilize and many challenged industries bounce back, 2022 may be the year community bankers put the rubber to the road by revisiting goals and turning them into action items. What will drive profit in 2022? Janet Silveria, Community Bank of Santa Maria.

Current investors Bessemer Venture Partners, Runa Capital and Acton Capital Partners also took part. Mambu said it is also embarking on a hiring spree, with plans to double its payroll to over 1,000 by 2022. TCV led the latest round of financing, with Tiger Global and Arena Holdings contributing additional dollars.

Banks & credit unions recognize the importance of new deposits After years of consistent deposit growth, financial institutions have faced a shift recently, with deposits declining since 2022. Consider: Cash management services that help businesses optimize their working capital. How can they attract and retain new depositors?

First Capital Bank. TriState Capital Bank. So that’s where the capital to start New Haven Bank came from.”. TriState Capital Bank. Beacon Community Bank. Charleston. First Bank. Burkburnett. Bank of San Francisco. San Francisco. Haverhill Bank. Laurinburg. Sullivan Bank. Chickasaw Community Bank. Oklahoma City.

An entrepreneur with a background in accounting and finance, CEO and chairman of the board Thomas Swenson set up Montana Business Capital Corporation in 1998 with a focus on job creation and economic development lending. What do community bank employees reveal about their workplaces and the industry more broadly in 2022? Methodology.

According to Worldpay’s 2018 Global Payment Report, mobile payments usage globally will grow to 28 percent in 2022 ¹. The post Business software solution providers can capitalize on payments integrations now appeared first on Accenture Banking Blog. Merchants therefore need to adapt. 1 Worldpay.

In May 2022, CBOE expanded S&P 500 options expiration days from three to all five weekdays. Intraday risks are not captured explicitly under the Pillar 1 market risk regime, and thus the Pillar 1 market risk capital requirement may not be sufficiently prudent for institutions engaging in zero-day options trading.

Some providers are capitalizing on the concept by launching new services that offer access to premium content such as newspapers and magazines in exchange for a monthly fee. subscription box market by 2022 is £1b.

For non-PBEs with a calendar year fiscal year, the standard is effective January 1, 2022 and the standard should be applied in financial statements and regulatory reports for the quarter ended March 31, 2022. How will CECL impact GAAP and regulatory capital? Non-PBE: December 15, 2021. the incurred loss method).

GET the list of 2022 fintech 250 companies. Below are a few highlights from the Fintech 250 Class of 2022. All but one of this year’s insurance winners were also featured in our inaugural Insurtech 50 , published in June 2022. Accel is second with 29 companies in its portfolio, followed by Ribbit Capital with 27.

Last week, the financial markets took hits from all directions. On the inflation front, March CPI and PPI came in at levels not seen since the late 1970s to early 1980s. On the war front, the conflict continued to rage as we move closer to direct engagement with Russia by announcing to deliver more and heavier weapons to Ukraine.

Last week was marked, once again, by extreme volatility. The violence of Russia’s war in Ukraine intensified while sanctions against Russia and its major industries continued to ramp up.

It was another week for the ages. On Thursday, the January CPI reading came in much higher than expected (and expectations were pretty high) with price pressure hitting just about every part of the economy. at day's end.

It is hard to imagine anybody went home for the weekend happy. The rout in both the equity markets and the bond market continues to pick up intensity. Global inflation continues to build as the supply of just about everything needed to make the world clothed, sheltered, and fed is experiencing major problems.

It was another wild and crazy one last week as the markets dealt with the dueling narratives of a flight to quality, risk-off reaction to the growing Ukraine crisis in Europe, and continued inflation pressures at home. We ended the week focused on the former as stocks sold off hard.

Last week was highlighted by carnage in the long end of the Treasury yield curve as both Federal Reserve Vice-Chairwoman Lael Brainard and Kansas City Federal Reserve Bank President Esther George took to the airwaves to say that the Fed would be reducing its $8+ trillion balance sheet very soon.

It was another wild rollercoaster ride for the financial markets in the holiday-shortened week as equities, corporate debt, and risk-free rates reminded me of Evelyn Cross (Faye Dunaway) in the 1974 classic, Chinatown, “Hard landing, soft landing, worst is over, still more to come, long rates capped, still have a long way to run, etc.”.

Equities and credit sensitive bonds jumped sharply last week leaving investors wondering over the long weekend if the worst is over or whether it is a chance to exit at higher levels. The “good” news over the week was that both the U.S.

Last week was marked once again by extreme volatility. On Wednesday, we had the Fed FOMC statement and presser. Stocks and credit risk assets were soothed by Chairman Powell’s words that his aggressive inflation fighting monetary policy wouldn’t bring on recession.

The best way to describe last week is, “the week of the hawk." On Thursday, the Bank of England became the first of the major central banks to raise policy rates 25 basis points with four members of the BOE’s committee calling for a 50-basis point hike.

It was a terrible, horrible, no-good week as nearly every asset class (save the USD against any other currency) took its turn to get pummeled. The combination of inflation and growth concerns thrashed stocks and just about all fixed income products spread off U.S. Treasuries.

Last week was dominated by the increasing aggressiveness of the Russian invasion of Ukraine along with the advancement of additional sanctions on Russia by the West. If Putin didn’t know who owns the machine that makes the money go around, he certainly found out last week.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content