This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Since that blog was published, the FDIC has issued an update on its Restoration Plan for the Deposit Insurance Fund (DIF). The Federal Deposit Insurance Act (FDI Act) requires the FDIC Board to adopt a restoration plan when the DIF’s reserve ratio—the ratio of the fund balance relative to insured deposits—falls below 1.35

Banking Trends from the FDIC's 2Q Report Net interest margin reached a new record low, but positive signs emerged in lending. Summary of the Latest FDIC Quarterly Profile. FDIC) released the latest Quarterly Banking Profile recently, and it has some helpful information on industry trends. Banking Data. Interestingly, 64.1%

SVB Financial had Tier 1 risk-based capital of 15.40% as of December 31, 2022, over 80% higher than the 8.50% regulatory required ratio. December 31, 2022 SVB Financial Bank Required Ratio CET1 risk-based capital 12.05% 15.26% 7.00% Tier 1 risk-based capital 15.40 Note the 56% increase in 2022. Short Capital?

The Stress Test Scenarios for Big Banks Are Useful for Smaller Institutions' Own Tests Banking regulators recently released the 2022 scenarios for upcoming stress tests by the biggest banks. The 2022 stress test scenarios provide a blueprint for community banks and credit unions to get started on their own stress tests.

According to the Federal Deposit Insurance Corporation (FDIC), in 2000, there were 8,000 commercial banks in the United States, but as of March 2022, that number had dwindled to 4,194 operating physical bank branches.

Seeking additional arrows in their quiver against large bank failures, on October 14, 2022, the Federal Reserve Board (FRB) and Federal Deposit Insurance Corporation (FDIC) published an Advance Notice of Proposed Rulemaking (ANPR). Email regs.comments@federalreserve.gov.

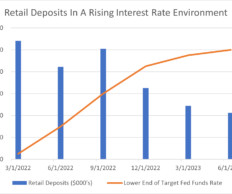

Retail Deposits Defined The FDIC classifies retail deposits as demand or term deposits placed within an FDIC-supervised institution by a retail customer or counterparty, excluding brokered deposits. The most significant quarterly drop (in the fourth quarter of 2022) was just over 5 percent.

In various press releases, the Federal Deposit Insurance Corporation (FDIC) has highlighted that an estimated $16.3 billion of the total cost incurred from the failures of Silicon Valley Bank (SVB) and Signature Bank was designated for safeguarding uninsured depositors. Commencing with the first quarterly assessment period of 2024 (i.e.,

On December 13, 2022, the FDIC issued a request for comment on a proposal to modernize the regulations governing use of the FDIC’s official signage and advertising of FDIC-insured status by insured depository institutions (IDIs), and to clarify regulations issued.

The FDIC has filed motion to dismiss the lawsuit filed in July 2023 in a Minnesota federal district against the FDIC and its Chairman seeking to invalidate the FDIC’s supervisory guidance on charging multiple non-sufficient funds (NSF) fees for the same unpaid item. See out prior blog here. Continue Reading

Using FDIC data for 2021, we calculated a lender score out of 100 for each community bank. But as they always do, they came through for individuals and businesses in their communities with a combination of personalized service and prudent risk management practices. By Ed Avis. Methodology.

On August 19, 2022, the FDIC issued cease and desist letters to five crypto companies, alleging they made false and misleading statements about FDIC deposit insurance and demanding immediate corrective action. According to the FDIC’s press release , “[b]ased upon evidence collected., Part 328, Subpart B.

Meet Model Risk Management Expectations Updates to the FDIC Risk Management Manual should steer institutions toward a model that manages risk and drives growth. FDIC Update. Last April, the FDIC released an Interagency Statement titled Model Risk Management (MRM) for Bank Models and Systems Supporting BSA/AML Compliance.

On July 25, 2022, the FDIC issued Financial Institution Letter (FIL)-34-2022 announcing updates to Chapters 1 and 4 of its Formal and Informal Enforcement Actions Manual (Manual). The Manual includes updates to the minimum standards for the FDIC’s termination of cease-and-desist and consent orders.

The FDIC has issued new supervisory guidance (FIL-40-2022) on multiple non-sufficient funds (NSF) fees arising from the re-presentment of the same unpaid transaction. In the guidance, the FDIC addresses potential risks arising from multiple re-presentment NSF fees, risk mitigation practices, and the FDIC’s supervisory approach. .

The full compliance date for the final rule is January 1, 2022. The FDIC issued a new Financial Institution Letter ( FIL-23-2021 ) last week in which it announced that, to facilitate implementation of the final rule, it has added a Brokered Deposits webpage to the Banker Resource Center on its website.

However, in the current rising interest rate environment in the United States since 2022, loan rates have adapted more rapidly than deposit rates. In table form, transaction account balances declined by almost 30% in the second quarter of 2022 as interest rates began to rise, later moderating in the latter half of the year.

In a letter sent earlier this month, the Bank Policy Institute, the American Bankers Association and the Independent Community Bankers of America (the “trade groups”) have asked the FDIC for more time to comment on the agency’s proposal , published in the Federal Register on December 21, 2022, to update its existing regulations governing use and misuse (..)

In the March 2023 issue of Consumer Compliance Supervisory Highlights , the FDIC discusses consumer compliance issues identified by its examiners during supervisory activities conducted in 2022 involving referral arrangements, trigger leads, servicemember protections, and fair lending compliance. Compliance Issues.

The CFPB has published its Spring 2022 rulemaking agenda as part of the Spring 2022 Unified Agenda of Federal Regulatory and Deregulatory Actions. Even the two items that appeared as long-term actions in the Fall 2021 agenda, artificial intelligence and mortgage servicing, no longer appear in the Spring 2022 agenda.

The Federal Deposit Insurance Corporation (FDIC), the National Credit Union Administration (NCUA), the Board of Governors of the Federal Reserve System (FRB), and the Office of the Comptroller of the Currency (OCC) have put out a joint statement addressing many frequently asked questions about the new standard. Non-PBE: December 15, 2021.

As indicated by the CFPB, the Circular was issued in connection with the FDIC’s issuance of a final rule implementing the Federal Deposit Insurance Act’s (FDIA) prohibition on false advertising through the misuse of the FDIC’s name or logo or making knowing misrepresentations about deposit insurance coverage. . FDIC Final Rule.

On the liability side of SVB’s $173B in deposits at the end of 2022, approximately 97% were uninsured and above the $250k in FDIC protection threshold. at the end of 2022, with $2.4B That fact makes the bank’s deposits less sticky and subject to outflow at any sign of insolvency.

The FDIC has issued a final rule that establishes a new framework for analyzing whether deposits made through deposit arrangements qualify as “brokered deposits” and amends the methodology for calculating the interest rate restrictions that apply to less than well capitalized insured depository institutions (IDIs). Brokered Deposits.

FDIC-insured “Problem Banks” list has been increasing over the past two years. The Data on Bank ROE As shown in the graph below, community bank industry average ROE declined to 10.38% in Q1/24 from 12.63% in the prior quarter, and the number of banks reporting negative ROE in Q1/24 increased to 237 from 91 in 2022.

FDIC-insured banks and savings associations earned $59.7 billion in the first quarter of 2022, a 22.2% The post FDIC: Increase in provision expense drives bank net income down appeared first on ABA Banking Journal. decrease from the year prior, the agency reported yesterday in its Quarterly Banking Profile.

The FDIC approved a final rule to increase initial base deposit insurance assessment rates by 2 basis points until the Deposit Insurance Fund (DIF) achieves the FDIC’s long-term goal of a reserve ratio of 2% of insured deposits. The FDIC’s long-term goal for the reserve ratio of insured deposits. Source: FDIC.

2022 Planned Roadmap. Imagine the complexities that will abound when structured notes, which are notes that have a built-in derivative, begin to peg their principal and interest payments to the value of a stablecoin.

The Q1 2023 compliance date is near for smaller SEC-reporting financial institutions and private or not-for-profit banks and credit unions, and progress is decidedly mixed, according to the Abrigo 2022 CECL Survey. Most bankers (86%) indicated they’ve moved beyond data collection in 2022, even if they haven’t yet adopted the standard (i.e.,

The FDIC has issued the March 2022 edition of Consumer Compliance Supervisory Highlights which includes a description of some of the most significant consumer compliance issues identified by FDIC examiners during consumer compliance examinations conducted in 2021. Fair lending.

The 2022 clarity promised by the “roadmap” presumably will supersede, once issued, Interpretive Letter #1179, which appears to function as a general stop-gap until the 2022 publications hopefully provide more detail regarding exactly how banks can attain compliance.

As a point of reference, the S&P US BMI Bank Total Return Index for the five years ended December 9, 2022 was -1.21%. As of or for the year-to-date September 30, 2022, the Company had $3.1 billion in total assets at September 30, 2022, fueled by organic growth and acquisitions. Silvergate Capital Corporation (NYSE: SI) #2.

We estimate that approximately another 500 use hedging programs that keep the derivative off balance sheet (thus not reportable by FDIC). Notably, the two banks with zero or near zero swap notional at the end of 2022 are now defunct institutions (First Republic Bank and Silicon Valley Bank). Only 304 banks (or 6.7%

banking regulators (the “2022 Joint Notice” or the “Proposal”). 2022 Joint Notice: Under the Proposal, banks would continue to utilize a facility-based delineation for assessment areas, but the geographic requirements for delineating these areas would be based on bank size. 2022 Joint Notice.

After moving alone in 2020 to reform its Community Reinvestment Act (CRA) regulation, the Office of the Comptroller of the Currency (OCC) has joined the Federal Deposit Insurance Corporation (FDIC) and Federal Reserve Board in issuing a joint notice of proposed rulemaking setting forth proposed amendments to their regulations implementing the CRA.

Cross River Bank recently found itself in hot water with the FDIC when the agency declared that the bank engaged in unsafe or unsound banking practices in relation to its compliance with fair lending laws and regulations, specifically the Equal Credit Opportunity Act and the Truth-in-Lending Act. In effect, Cross River is in time out.

A major step in this direction is the European Union Markets in Financial Instruments Directive II (EU MiFID II) Regulation requiring financial firms to incorporate sustainability preferences into their advisory and portfolio management processes since 2022.

When it comes to comprehensive loan review, loan officers should get familiar with FDIC regulatory expectations, examine their processes, and consider what tools and resources can support their review process while meeting regulatory expectations.

Of that group of users, the Federal Trade Commission (FTC) reports that since the beginning of 2021 through the first quarter of 2022, more than 46,000 people have reported losing over $1 billion in crypto scams. Of course, crypto is not insured by the Federal Deposit Insurance Corporation (FDIC) and is a risky investment.

You might also like this webinar: "Is inflation the big gift to your 2022 earnings?". Noninterest income drove 20% of community banks' net operating revenue in 2019, down from 22% in 2012, according to a recent FDIC study. Community banks have seen less volatility in noninterest income over time.

regulatory authorities may be less lenient about bank accounting and reporting errors stemming from old technologies — like spreadsheets — particularly for repeat offenses. Banks could see 500% higher fines for errors stemming from outdated, problematic methods. So predicts Bikram Singh, chief executive officer of Brunswick, N.J.-based

We examine all FDIC-insured commercial banks and S&L associations over the last three decades and plot COF versus short-term rates. The OCC published in January 2022 that the banking system currently holds $3T in “excess” deposits (about 17% of total deposits).

Based on the futures market, the Federal Reserve is expected to raise the Fed Funds rate to 3.00% at its December 2022 meeting. We examine the roughly four thousand FDIC-insured commercial banks and S&L associations over the last four decades. The Fed will also aggressively shrink its balance sheet to tame unwanted inflation.

The lawsuit takes issue with the agency's 2022 guidance on nonsufficient funds fees, a hot-button topic in the banking industry. The FDIC is asking a judge to dismiss the case, arguing that the plaintiffs lack standing to sue.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content