This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Preparing for 2023 While communitybanks have until 2023 until they must comply with CECL, there is likely less time than expected. . 2023 CECL Deadline? Each quarter represents an opportunity to refine the CECL model prior to 2023. The time is now to ensure you are ready for January 1, 2023.”

Communitybank cost of funds is jumping up. As shown in the graph below, the net interest margin (NIM) for communitybanks declined 22bps in Q1’23. The question is – what will happen to communitybank’s cost of funds from here? SP Global also forecasts deposit beta for the industry in 2023.

Of the largest 250 banks, 90% are using interest rate swaps, and because these largest 250 banks hold 83% of all loans, interest rate hedging tools are widely used in approximately 75% of the loan marketplace. The market expects deposit betas to increase through 2023 and 2024.

On September 7, 2023, the FDIC released its banking profile. This quarterly publication provides a comprehensive financial results summary for all FDIC-insured institutions (4,645 commercial banks and savings institutions insured by the FDIC). While banks under $10B in assets comprise 97.8%

As rates stay high, concerns about credit risk and borrower health are top of mind for bank and credit union leaders, especially as it relates to lending to small businesses. Longer working capital cycles drive line utilization Businesses are holding inventory longer (81 days in 2023 vs. 72 in 2019) and extending receivables (31 to 41 days).

People want to be a part of something bigger than themselves, and communitybanks provide that opportunity. Communitybanking is about serving the greater good. As community continuators, we are part of something bigger than ourselves. I wish everyone a merry Christmas and a prosperous 2023.

2022 will go down as one of the worst years for communitybank loan mispricing when viewed on a spread basis. Rapidly rising rates crushed performance as many banks held a fixed rate constant and/or booked a fixed rate loan at a misguided level. Banks had tight spreads on loans with 1.2

Be recognized as one of communitybanking’s best employers. ICBA Independent Banker ‘s Best CommunityBanks to Work For award is your chance to show job hunters and current staff why your communitybank is an unbeatable place to build a career. Click to nominate your bank. Leadership.

Banking regulators announced they intend to rescind the 2023Community Reinvestment Act final rule in light of pending litigation. The post Banking regulators to rescind 2023Community Reinvestment Act rule appeared first on ABA Banking Journal.

Bank leaders must feel like Rocky Balboa after 15 rounds with Apollo Creed. Just think of what the industry dealt with in the last 12 months: The brunt of the unprecedented scope and pace of Fed rate hikes hit home, and banks have seen an.80 million (that’s right million) of financial donations and support to the community in 2025.

However, in 2023, loan prepayment provisions will be essential tools for commercial banks. Loan prepayment provisions lower prepayment speeds (especially in a stable or declining interest rate environment) and drive higher return on assets (ROA) for banks. Prepayment penalties on loans always drive value.

In this article, we quantify commercial loan pricing trends from our Loan Command data that will hopefully help communitybanks price more effectively and win more profitable business. On the interest rate risk side, banks put more fixed rates on their books in 2024 compared to 2023.

This article provides an update on pricing trends driven by our Loan Command aggregated communitybank data and highlights some working pricing ideas. A combination of credit concerns and funding pressure have most communitybanks focusing on their existing customers and moving away from new transaction-orientated clients.

of digital banking customers said they switched to digital banking because of the pandemic. Source: 2021 Provident Bank survey. These days, there’s a lot to contend with as a communitybank, from changing consumer behaviors due to the pandemic to uncertainty surrounding the economy and inflation. Quick stat.

Teaching staff these KYC tips to make clients feel more comfortable In 2023, KYC procedures must both support CDD compliance and make sure your institution is a welcoming place for all customers. Takeaway 2 In 2023, KYC should both strengthen your AML program and personalize services to support clients' individuality and value.

A potential economic slowdown, slower rate rises, an inverted yield curve, and deposit stress likely make 2023 a trying year compared to 2022. Banks will need to balance these short-term challenges with longer-term strategic goals. Financial pressure will be greater, and bank margins will be higher.

In a previous article ( here ), we discussed why commercial loan prepayment protection would be a critical return on asset (ROA) driver for communitybanks in 2023. We outlined the four main reasons why prepayment provisions increase profitability for banks.

This regime is now changing, and communitybanks need to position their lending and deposit portfolios for a period of monetary tightening. Short-term rates are also likely to continue to climb through 2023. Banks that have avoided, or can reduce, their holdings of riskier assets as much as possible will outperform.

Top 20 Deposit-Rich Industries Using the data we have, we looked at some major industries that have above-average balances that communitybanks have had success with in the past. The post The Top 20 Deposit-Rich Industries for 2023 appeared first on SouthState Correspondent Division.

” This is why digital banks and fintechs—led by Chime and PayPal—captured nearly half of all new “checking” accounts opened so far in 2023. 3) Product pricing There’s a value disconnect in banking. government as a “significant” threat to the banking industry. The savior?

Financial institutions work to meet Q1 2023 CECL deadline A CECL implementation survey by Abrigo found progress by financial instittuions is mixed ahead of the upcoming deadline. . Takeaway 1 10% of banks and credit unions have completed CECL adoption, according to Abrigo's CECL implementation survey. Conclusion. Learn More.

I’ve always been a glass-half-full guy, and though 2023 is expected to be a challenging economic year, it also brings opportunity. We simply need to remember what makes us special as community bankers, and with that as our foundation, we can embrace this season of change in four primary ways: 1. Priorities for a successful 2023.

There is a rash of bank consent orders that either were just made public or are about to become public that everyone is talking about and have noticeably put a damper on communitybanks’ enthusiasm for BaaS. Given that the SEC is not far behind, environmental reporting was also common cocktail party content.

Deposit costs and liquidity remain a challenge for some communitybanks as competition for core funding remains intense. The graph below compares the liquidity ratio for communitybanks (under $10B in assets) and banks over $100B in assets. Communitybanks do have a few strategies for mitigating COF pressures.

Stevens’ novel, The Lies About Truth , that captures our ethos heading into 2023: “If nothing changes, nothing changes. I believe 2023 will continue our industry’s forward momentum as our members position themselves to be the agents of change that find and champion new opportunities. You want change, make some.”

ITMs and VTMs are popular retail banking innovations among communitybanks. What’s on the horizon for retail banking? We spoke with two communitybanks that have ramped up their services to meet—and exceed—the changing expectations of customers. So how are retail banks meeting this challenge?

On September 20, 2023, the Federal Open Market Committee (FOMC) left its benchmark rate unchanged, but it would be a mistake to conclude that the committee did not send a strong message about the projected path of future interest rates. in 2023 and slightly higher in 2024.

households were unbanked in 2023, according to the FDIC’s National Survey of Unbanked and Underbanked Households, which also explored bank account access trends and cryptocurrency adoption. The post FDIC: Percentage of unbanked households dropped slightly in 2023 appeared first on ABA Banking Journal. Roughly 4.2%

Conclusion We have always been keen on outlining practices that lead to higher performance for communitybanks. Implementing some of these loan pricing and structuring best practices can be politically sensitive, but better-informed bankers lead to higher-performing banks.

While the pace of bank regulatory changes has diminished from a few years ago, several issues will either become effective or likely develop in 2023. Communitybanks must continue to stay focused on regulatory discussions and remain nimble to respond to proposals and address requirements quickly and accurately.

Federal Trade Commission (FTC) reported consumers lost more than $10 billion to fraud alone in 2023. Think about it: when a fraudster targets a small business owner or when an individual’s life savings are wiped out, it doesn’t just hurt the bank—it devastates families and communities. It’s about relationships.

As communitybanks navigate this process, there are plenty of resources available to answer questions and provide guidance. Three sources of information on FedNow As communitybanks look to take advantage of this new opportunity, they seek resources to help them navigate the journey.

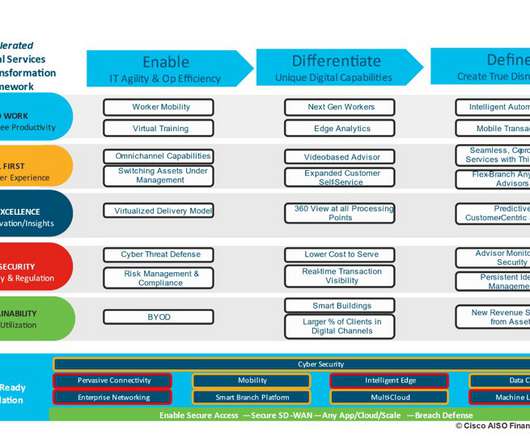

Whether a communitybank or a credit union, regional insurer, or multi-national financial institution, cross-functional engagement with champions, key influencers and ultimate decision-makers also helps to eliminate silos inherent in the financial services industry. Accelerated Digital Transformation Framework.

However, communitybanks, in particular, face challenges in quantifying risk and applying compliance measures using a risk-based methodology, Brewer said. To succeed against fraud, more banks and credit unions must also focus on internal fraud prevention training. Check fraud will also place fresh demands on compliance teams.

Research by S&P Global shows increased borrowing and declining credit conditions could push up costs substantially CommunityBanking Feature3 Feature The Economy Financial Research Financial Trends

The total number and value of small-business and small-farm loans made by financial institutions subject to the Community Reinvestment Act declined in 2023 compared to the previous year, the banking agencies reported.

The most-read lending & credit blogs in 2023 Probability of default, CECL model validation, and stress testing were among Abrigo's top blogs on ALM, CECL, and portfolio risk this year. download NOW Takeaway 1 The most popular blog posts on the Abrigo site reflect many of the priorities communitybanks and credit unions had in 2023.

Banks have ceased using LIBOR to price assets and liabilities after 2021. The remaining LIBOR cash and derivative instruments will continue until June 30, 2023. An index representing overnight rates and term structures is fundamental to communitybanks that sell products with multiple payment periodicities. Daily SOFR.

Merchants & Marine Bank and City National Bank have launched separate initiatives to support small businesses and local communitiesCommunityBanking Feature3 Feature Small Business Customers People Consumer Compliance

As the end of the year draws near, banking journalist and analyst Paul Davis joins the ABA Banking Journal Podcast to discuss the bank mergers and acquisitions outlook for 2023. The post Podcast: The communitybank M&A outlook for 2023 appeared first on ABA Banking Journal.

Firm deadline for CECL implementation set As expected, the FASB agreed to uphold CECL’s 2023 implementation date. You might also like " CECL Streamlined: A Webinar Series for 2023 Adopters". Takeaway 1 The FASB agreed to uphold the 2023 implementation date for those that haven’t yet adopted the CECL standard. Learn More.

FedNow can be another positive differentiator for our nation’s communitybanks, but we must be ready for this real-time service and its 24/7/365 requirements.”. By mid-2023, we will be able to begin offering this solution to our customers. So, with FedNow’s launch on the horizon, what can communitybanks do to prepare?

Fintech startups looking for funding in 2023 are finding that it isn’t as easy as it was a few years ago. CommunityBanks as Venture Capitalists In fact, not all providers of venture capital are venture capitalists. Increasingly, banks are filling the void created by VCs. billion in capital into fintech startups in 2023.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content