This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

During the webinar, experts shared data and insights about CRE lending trends and offered advice for managing related risks. However, office properties struggled to attract lenders, with their share of CMBS issuance shrinking to under 8% by late 2024, compared to 20% in early 2023.

Abrigo's most popular whitepapers and checklists on lending and credit risk Abrigo experts' insights on CFPB 1071, loan policies, and risk ratings were popular with banking professionals. Watch NOW Takeaway 1 Abrigo's experts produced many pieces on lending and credit risk to provide strategies and tools to help banking professionals.

While significantly more efficient than mailing forms to the SBA, there are some shortfalls to E-Tran, and a vendor can help Loan submission platform Leveraging E-Tran for increased SBA lending The U.S. Understanding the role of E-Tran in SBA lending is the first step for banks and credit unions to ensure smooth loan processing.

The most-read lending & credit blogs in 2023 Probability of default, CECL model validation, and stress testing were among Abrigo's top blogs on ALM, CECL, and portfolio risk this year. download NOW Takeaway 1 The most popular blog posts on the Abrigo site reflect many of the priorities community banks and credit unions had in 2023.

Takeaway 2 Readers in 2023 were most interested in getting information about preparing for exams, learning about stress testing, and seeing how peers manage loan review. Indeed, regulators and management alike focused on these risks more and more in 2023 following the failure of Silicon Valley Bank and repeated rate hikes.

The same framework should be in place to improve technology used by regulators in efforts to strengthen supervision throughout the industry, the think tank also says. billion by 2023, up from an estimated $4.5 The risk and safety lines with AI in China in the finance sector appear to be blurring. trade war.

You might also like this webinar: "CECL implementation FAQs: Progress as 2023 approaches" listen Takeaway 1 The National Credit Union Administration emphasized interest rate, liquidity, and credit risk as main concerns. Some credit unions discussed the expected effects of CECL adoption in 2023 in a separate section of their plans.

Fraud trends for financial institutions to watch for in 2023 Financial institutions should not expect a slowdown of any of 2022’s fraud trends. Be on the lookout in 2023 for the following trends identified by the FBI. No fraud decrease likely for 2023. Current economic indicators do not bode well for fraud stabilization in 2023.

Financial institutions work to meet Q1 2023 CECL deadline A CECL implementation survey by Abrigo found progress by financial instittuions is mixed ahead of the upcoming deadline. . In many cases, financial institutions adopting CECL for the 2023 deadline are tracking ahead of where SEC registrants were as they faced a 2020 deadline.

Scottdale, Arizona was chillier than normal this week, but that didn’t prevent bankers from having heated discussions about 2023 at this year’s Acquired or Be Acquired conference, hosted by Bank Director. However, most bankers were optimistic that deals would pick up later in 2023 and that the chances of a raging 2024 are strong.

DOWNLOAD Takeaway 1 The effective date of the CFPB's new rule based on Section 1071 of the Dodd-Frank Act is June 28, 2023. Takeaway 2 Reporting tiers and their deadlines are based on the number of covered transactions to small businesses that a lender originated in 2022 and 2023. But compliance deadlines are tiered.

Perficient provides risk management to more than 500 financial services organizations, many of whom have multiple bank regulators. Often an organization will have a state-charted non-member bank, which has the FDIC as its primary federal regulator.

Federal bank regulators work together to design Comprehensive Capital Analysis and Review (“CCAR”) stress tests that are designed to ensure that even in the case of a severe recession, significant banks can lend to households and businesses. As repeated by federal bank regulators, the required economic scenarios are not forecasts.

Impact on Consumers The implications of the CFPB’s regulation on open banking will be enormous for consumers, banks, and data providers. Without open banking, consumers struggle to switch between bank deposit and lending offerings. Traditionally, banks hoarded financial data, sharing it sparingly on a need-to-know basis.

Find commercial real estate risks in the loan portfolio Sound risk management practices in commercial real estate lending help lenders manage CRE credit losses and protect the portfolio's profitability. office buildings with a vacancy rate over 95% declined to 60% in Q2 2023 from 63% in Q1 2020, or pre-pandemic.

The most-read portfolio risk blogs in 2023 Probability of default, CECL model validation, and stress testing were among Abrigo's top blogs on ALM, CECL, and portfolio risk this year. Abrigo's most popular risk management blogs over the last 12 months cover topics that continue to catch the attention of professionals and regulators.

For the $10B$50B crowd, 2D model use dropped from 60% to 50% in 2023. During the 2008 financial crisis, our regulators directed us to charge down certain residential lot loans. Here are the results of the most recent survey: For banks under $10B in assets, only 5% used a 2D model in 2024 (down from 15% historically).

I’ve always been a glass-half-full guy, and though 2023 is expected to be a challenging economic year, it also brings opportunity. I encourage you to join us and lend your voice to supporting these and other advocacy efforts, which will shape the policy landscape. Priorities for a successful 2023. My Top Three.

If the CFPB was so concerned about fees charged by banks, perhaps they should perform an analysis of over regulation that is a key contributor to fees charged by banks? Regulators must not have read that article. What do regulators think will happen? I cannot lay the sole blame at the feet of regulators.

Holding these assets can impact profitability because banks can’t lend those funds out or invest them at higher rates. The Credit Card Competition Act of 2023 could negatively impact banks’ ability to generate interchange fees and reduce the amount of capital they issue, however. Commercial real estate loans. 5) The political element.

The regulators are considering three options: raising the limit above $250k, raising the cap for only certain accounts (such as banks’ business accounts), or eliminating the cap entirely. With the collapse of First Republic Bank, the 2023 total of failed bank assets is now a new annual record – as shown in the graph below.

invalidating the payday lending rule) was incorrect. For example, if the CFPB’s mortgage regulations are vacated, mortgage lenders would have to immediately modify annual disclosures and borrowers could rescind transactions that had relied on regulatory disclosure exceptions.

A federal judge late last week ordered a stay on the August 2019 compliance date tied to the “ payday lending rule ” mandated roughly two years ago by the Consumer Financial Protection Bureau (CFPB). The bill, known as Senate Bill 2023, is co-sponsored by Senator Toi Hutchinson and Michael Frerichs, state treasurer.

The compliance deadline, however, depends on the firm’s total receipts from calendar years 2023 and 2024. Impact on consumers Without open banking, consumers struggle to switch between bank deposit and lending offerings. The ruling demands action from all non-depository firms (e.g.,

Takeaway 3 Utilize regulatory guidance to understand regulators' expectations, which are likely to include consistent stress testing. In a recent Abrigo webinar, four experts weighed in to pinpoint the following areas for focus and improvement in 2023. Get to know regulator expectations and priorities. Cultivate talent.

Wake of 2023 bank failures Federal Housing Finance Agency review prompts reform The Federal Home Loan Bank (FHLB) system faces potential changes in its structure, operations, and mission that could affect financial institutions. These FHLBs continued to lend to the member banks despite clear deterioration of their financial status.

Takeaway 2 The rule is aimed at tracking small business credits to enforce fair lending laws and ID and support women- and minority-owned small businesses. The regulation, expected to be finalized in weeks, outranked BSA/AML rules, beneficial ownership requirements, and current expected credit loss (CECL) obligations.

The FHFA announced that Fannie Mae and Freddie Mac will require mortgage servicers to maintain certain fair lending data elements, including the borrower’s age, race, ethnicity, gender, and preferred language. The fair lending data must be stored in a searchable format, and must transfer with servicing throughout the loan term.

Download now Takeaway 1 Under current federal law, banks and credit unions face federal prosecution and penalties if they provide services to legal marijuana-related businesses. Takeaway 2 Considering the urgent need for a legislative solution, the SAFE Banking Act of 2023 could bridge the gap between state and federal marijuana laws.

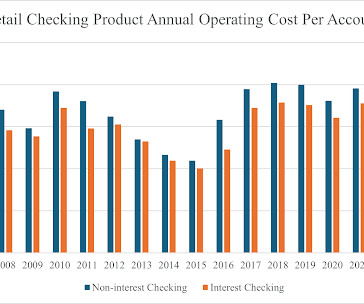

Retail banks respond to the Federal Reserve’s short-term interest rate adjustments with corresponding changes in lending and deposit rates. Transaction Accounts Regulators classify transaction accounts under the Monetary Control Act of 1980 and the Federal Reserve Regulation D for federal reserve requirements on deposit liabilities.

Takeaway 1 Signs point to increased loan modifications and loan workouts, and regulators have urged financial institutions to work prudently with borrowers. . Meanwhile, regulators are focusing fresh attention on prudent credit risk management of loans, especially CRE, and loan modifications in general. CRE loan accommodations.

Year Of Secured Loans Retail lending grew by 16% to 5.2 Secured loans led the way: home loans, the largest retail lending category, rose by 18% (up from 14% last year) and gold loans surged 56%, marking the fastest growth across all categories. RBI regulations on transparency in charges created awareness but reduced issuer profits.

A gap institution is a financial institution that does not have a federal functioning regulator, such as a state-chartered credit union. million civil money penalty for willful violations of the BSA and its implementing regulations. FinCEN assessed a $1.5

Takeaway 1 Banks and credit unions moving to CECL in 2023 understandably want to know how Q factors will compare with current practices. is a popular topic among bankers, especially those with a 2023 CECL implementation date, according to Zach Englert, a CECL Consultant with Abrigo’s Advisory Services. Implementing CECL in 2023?

Consistently rated a top industry event by attendees, ThinkBIG brought together 650 people from banks, credit unions, and partners in 2023. Attendees staying at the resort can take advantage of two world-class golf courses, tennis or pickleball, or escape to the Tierra Luna Spa, a Forbes 2023 four-star Spa Award Winner.

The Stress Test Scenarios for Big Banks Are Useful for Smaller Institutions' Own Tests Banking regulators recently released the 2022 scenarios for upcoming stress tests by the biggest banks. It’s important to note that these scenarios do not represent a forecast by the banking regulators. Related Subhead. doing very well in 2022.

Experts answer CECL questions from 2023 adopters Participants in Abrigo's CECL Kickstart webinars asked consultants their questions leading up to the 2023 CECL implementation date. Takeaway 3 With good organization and some expert assistance, financial institutions will have a defensible model by 2023. Models for Success.

Last week, JPM released its 84-page 2023 shareholder letter and 364-page annual report. Road trips, client meetings, briefings, and visits to call centers, branches, and regulators allow leaders to observe and assess the bank and the market. The bank holds the #1 market share for multifamily lending.

Key Takeaways An SEC filer with a 2020 CECL deadline recommends starting ASAP on implementation -- even if your deadline is 2023. Regulators, investors, and other stakeholders will be watching and listening for updates on the impacts of the accounting change. Assess data before selecting your methodology or methodologies. Get started.

A gap institution is a financial institution that does not have a federal functioning regulator, such as a state-chartered credit union. million civil money penalty for willful violations of the BSA and its implementing regulations. FinCEN assessed a $1.5

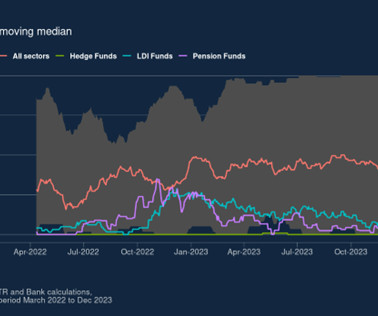

In this post, we use novel Securities Financing Transaction Regulation (SFTR) data to highlight new, and corroborate previous, stylised repo haircut facts. Dealers include prime brokers and other banks that typically extend cash lending to NBFI clients that rely on the bilateral gilt repo market for their liquidity and collateral operations.

What Will Auditors and Regulators Expect with CECL Accounting? A panel of CECL accounting experts described how auditors and regulators are viewing various aspects of implementation. . Takeaway 2 Auditors and regulators don't have preconceived expectations about how CECL reserves might change for an institution.

While UK support will continue through 2023, and possibly into 2024, we can expect to see it provided on a more targeted basis as governments face rising debt burdens as a proportion of GDP. Here are my three predictions for risk management and customer treatment in 2023. The challenge will be further exacerbated as an estimated 1.4

trillion nationally) are on pace to surpass student loans as the second-largest debt category in 2023. In announcing this request, “Enhancing Public Data on Auto Lending,” the CFPB stated: Financial markets and policymakers have long had access to granular mortgage data that has provided insight into patterns in lending and risk.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content