This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Communitybanks’ use of swaps (banks’ primary tool to hedge interest rate risk on loans) has increased substantially over the last ten years. The market expects the current inverted yield curve to remain through much of 2024 (based on long-term interest rates and the expected rate cuts in 2024).

Takeaway 2 Abrigo advisory expert Susan Sharbel offers insights into where your bank should focus its resources to manage interest rate risk, Takeaway 3 Practical steps for preparing your ALM program for rate changes include updating and validating risk models regularly, conducting tests, and reviewing portfolios. Upcoming exam?

Our recognition as the #3 communitybank in the state by GOBankingRates in 2025 reflects our commitment to Growing, Together with the communities we serve. Yet, the banking industry is at a turning point. My goal is to convince you to approve a pilot program that will cement our position as a leader in communitybanking.

In the 4 th quarter of 2024, commercial loan pricing has materially changed. In this article, we quantify commercial loan pricing trends from our Loan Command data that will hopefully help communitybanks price more effectively and win more profitable business. In 2024, approximately 16% were fixed rates.

Speaker: Brian Muse-McKenney, Chief Revenue Officer & Matt Simester, Cards and Payments Expert

In this new webinar, Brian Muse-McKenney of Episode Six and Matt Simester of Payments Consultancy Limited will explore the challenges regional and communitybanks have faced in implementing tailored credit card programs with flexible payment options as a tool to attract and retain the next generation of customers. Save your seat today!

Of the largest 250 banks, 90% are using interest rate swaps, and because these largest 250 banks hold 83% of all loans, interest rate hedging tools are widely used in approximately 75% of the loan marketplace. The market expects deposit betas to increase through 2023 and 2024.

Panelist Roxanne Chance-Chin , BSA Officer at the Bank of Tampa, urged financial institutions to stay alert to the cumulative effects of economic cycles and be prepared for potential rapid shifts in credit quality. The panel addressed the negative perception of compliance in communitybanking, advocating for a shift in perspective.

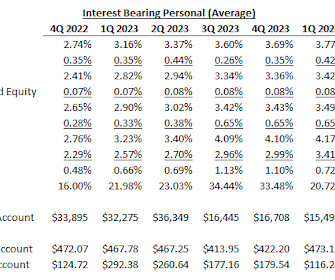

Bankers must understand the relationship between money supply and their bank’s COF. Even if the Fed does not increase the Fed Funds rate or even decreases the rate in the future, continued QT is expected to put pressure on the cost of funding in 2024. The graph below shows COF for the same three groups of banks.

Communitybank cost of funds is jumping up. As shown in the graph below, the net interest margin (NIM) for communitybanks declined 22bps in Q1’23. The question is – what will happen to communitybank’s cost of funds from here?

Since our last update on pricing and credit HERE , commercial loan pricing trends for the first quarter of 2024 continue to be driven by the perceived increase in credit risk, tighter credit supply and banks’ need for wider margins. percentage points bringing forward looking LGD to 44% of the average communitybank loan amount.

As a point of reference, the S&P US BMI Bank Total Return Index for the five years ended December 6, 2024 was 34.55%. 2 Northeast Bank (NasdaqGM: NBN) Northeast Bank is a full-service bank headquartered in Portland, Maine that had $3.9 billion in total assets and seven branches at September 30, 2024.

As rates stay high, concerns about credit risk and borrower health are top of mind for bank and credit union leaders, especially as it relates to lending to small businesses. Early 2024 figures show a dip in DSCR to 4.62x. However, recent data from Abrigo shows that privately held companies across the U.S.

A recent Wall Street Journal nailed the title— Main Street Banking Model Is Being Squeezed —but missed the mark on the cause. Commenting on the Q1 2024 profit declines for many community and regional (i.e., government as a “significant” threat to the banking industry. The savior? Getting there won’t be easy.

trillion globally in 2024. Connect with an expert Common fraud schemes Check fraud Check fraud is one of the most concerning fraud trends for communitybanks in 2025. This is a nearly 10% increase in complaints received and a 22% increase in losses and thats just fraud that was offically reported.

Given this new signal, communitybanks need to analyze what this interest rate environment means for their business model and how to maximize performance. The question is how will this interest rate development affect communitybanks’ performance, and what must communitybanks do to remain profitable?

Amid persistent inflation and core deposit competition, community bankers expand their pools of funding sources, according to the Conference of State Bank Supervisors’ 2024communitybank survey. The post Cost of funds shoots to top of community bankers’ concerns in 2024 appeared first on ABA Banking Journal.

The banking industry reported an aggregate net income of $66.8 billion in the fourth quarter of 2024, according to the FDICs most recent Quarterly Banking Profile. In addition, the agency ended reporting on the aggregate assets of institutions on the Problem Bank List.

In two recent articles, we reviewed the banking industry’s deposit behavior with regard to cost of funding earning assets (COF) ( HERE ), and we compared how communitybanks’ COF behaves relative to national banks in a rising interest rate cycle ( HERE ). A graph for SouthState Bank appears below.

Online account opening remains the wild west for most communitybanks. This was the background as I attended Bank Director's Acquire or Be Acquired (AOBA) conference. Berkshire Bank, a $12.3 billion in asset bank based in Pittsfield, Massachusetts, launched Berkshire One for online customers. Makes sense.

The bigger risk to communitybanks’ business model is not a moderate recession induced by aggressive interest rate increases by the Federal Reserve. The yield curve impact is having a negative effect on bank profits. Banks reluctant to commit to fixed-rate terms beyond two or three years are disadvantaged.

An inverted yield curve, continued bank failures, and the desire to manage risk and offer clients higher service are all factors that are driving more communitybanks to adopt a loan hedge program. Communitybanks do this profitably by turning transactional accounts into relationships.

An inverted yield curve, continued bank failures, and the desire to manage risk and offer clients higher service are all factors that are driving more communitybanks to adopt a loan hedge program. Communitybanks do this profitably by turning transactional accounts into relationships.

Deposit costs and liquidity remain a challenge for some communitybanks as competition for core funding remains intense. The graph below compares the liquidity ratio for communitybanks (under $10B in assets) and banks over $100B in assets. Communitybanks do have a few strategies for mitigating COF pressures.

The banking industry’s cost of funds (COF) is highly correlated to short-term interest rates. However, as of Q2/22, the average communitybank’s COF has risen only a few basis points. The COF over the past five quarters is shown for three asset peer groups: banks under $1B (3.5k The Data on Cost of Funds.

Bloomberg recently announced that it will shut down its BSBY index on November 15, 2024. We published various articles comparing communitybank alternatives to LIBOR (such as SOFR, Ameribor, Fed Funds, and Prime). Historically, communitybanks have hesitated to adopt derivatives for several reasons.

Financial Markets Update – Second Quarter 2024 A dream vacation! That and getting consumed by Euro 2024 and Copa America soccer and of course, the Phillies. In July 2024, we will mark two years of inversion between the 10-year Treasury and the 2-year Treasury yields. for 2024 and 2.0% It was so beautiful and lots of fun.

A resilient economy and the potential for interest rate cuts could infuse further bullish sentiment into markets and bolster the shares of small lenders.

However, we would like to identify one important macroeconomic variable that will affect the banking industry regardless of the makeup of the legislative and executive branches of the US government. Regardless of who wins, our national debt will continue to increase, and communitybanks should be prepared for its consequences.

Bankers are hopeful that several factors could strengthen profits next year, including higher loan demand and more stable funding costs as the Fed holds the line on — or even lowers — interest rates.

Credit union acquisition of banks doubled their pace in 2024, hitting a record high of 22 announced deals. The post ABA DataBank: Credit unions buy record number of banks in 2024 appeared first on ABA Banking Journal.

Communitybanks are striving to increase loan yield and maintain their cost of funding (COF). We have created and used a novel structure to take advantage of the inverted yield curve to allow communitybanks to increase net interest margin (NIM) and fee income on these existing fixed-rate loans.

Financial Markets Update – Third Quarter 2024 I had a fantastic September traveling to France and Luxembourg with my sisters. Between December, 2022 and March, 2024, M2 declined on a y-o-y basis, which was the first time that has happened since 1931 to 1933. trillion for fiscal 2024 compared to -$1.7 6 Money Stock report.

However, communitybanks, in particular, face challenges in quantifying risk and applying compliance measures using a risk-based methodology, Brewer said. To succeed against fraud, more banks and credit unions must also focus on internal fraud prevention training. Check fraud detection efforts will continue.

We recently conducted a small sample poll, and out of 21 banks, budgets were down an average of 14% for this year. In this article, we partner with Gartner to look at 2024 key IT metrics and provide strategic insight into how much your bank should be spending on IT. Usually, a bank spends about 8% of its revenue on IT.

Many banks budgeted some six rate cuts in their 2024 asset-liability plans last year that never materialized. How should communitybanks think about their balance sheets, product offerings, and client demand in this pivot? The graph below compares the December 2020 and the December 2024 FOMC DOT plots.

In our previous article ( HERE ), we reviewed the banking industry’s cost of funding earning assets (COF), and we compared how communitybanks’ COF behaves relative to national banks in a rising interest rate cycle. The market anticipates about $3 trillion in total balance sheet reduction by the end of 2024.

Communitybanking highlights in 2024 included strong deposit growth at a Los Angeles-based digital-only bank, continued regulatory scrutiny of banking-as-a-service arrangements, along with a transformational deal in the Old Dominion.

billion people – will likely be using online and mobile banking services by 2024. Add in generational preferences for digital products, as well as the stricter regulatory requirements and oversight that national banks face, and it becomes clear that the effort to refresh big, old banks will be no easy task.

We estimate that the average contractual loan commitment for term credit at communitybanks has decreased from just under five years in 2022 to just under three years currently. Communitybanks should carefully consider the prudence of such a strategy from both a risk and revenue perspective.

This year’s Jack Henry Connect was a remarkable event that captured the spirit of communitybanking while embracing the continuously shifting world of technology.

This year, 90 banks made American Banker's 12th annual Best Banks to Work For ranking. The leaders of these institutions share how they keep their employees happy.

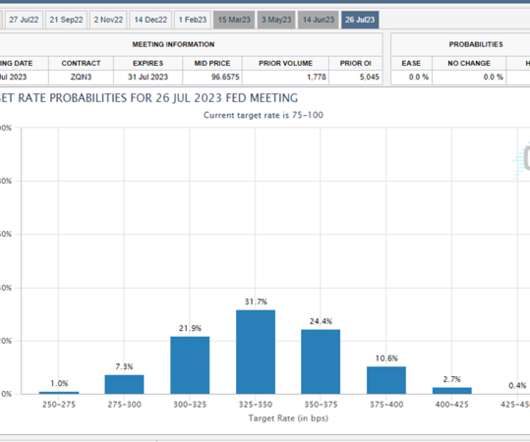

The Fed’s Dot Plot now shows a 5.625% terminal fed funds rate in 2023 and a 4.75% rate at the end of 2024. Equally important are the Fed’s 2023, 2024, and 2025 projections for inflation, GDP, and unemployment – all pointing to a hotter economy for a longer period.

The ABA Foundation named seven banks as 2024Community Commitment Award winners. Raul Valles of Dallas Capital Bank in Texas to receive the George Bailey Distinguished Service Award.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content