This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As we progress through 2025, the banking industry is set for substantial transformation driven by several key trends. Digital transformation will remain a powerful force, with advancements in AI and machine learning enabling unparalleled operational efficiencies and hyper-personalized customerexperiences.

The insurance industry in 2025 is at a pivotal point, with key digital insurance trends leading the charge in transforming how carriers operate and interact with customers. Carriers must innovate, adapt to these changes, and leverage new technologies to maintain a competitive edge.

The recent digital ordering surge is anticipated to continue well after the pandemic ends, with another study finding that digital will represent a majority of QSRs’ sales by 2025. Shake Shack On Leveraging AI, ML To Drive CustomerExperience. For more on these and other stories, check out the Trackers News & Trends section.

35 B: Expected value of the global call center software market by 2025. Data: $775 M: Predicted losses due to account takeovers at call centers by 2020. 71 percent: Share of digital media consumers who planned to cancel their subscriptions within one year after just one month of service.

Strategies to help banks attract new deposits Banks and credit unions planning for 2025 agree that attracting and retaining deposits remains a top priority. To succeed, banks must carefully balance competitive offerings with cost control while leveraging technology and relationship-building strategies to attract new deposits.

For example, in the next year, does the bank want to focus on making its employees more productive or enhancing customerexperience. In 2025, banks evolved in managing their goals and objectives through use cases. Few community banks have the resources to accomplish both, and both are sizeable efforts.

By 2025 — less than a decade later — it’s projected to reach $27,238.6 The second trend is closely tied to the first: As technological awareness and product choice expand, AI-based startups have proliferated to deliver to the industry the capabilities it needs to meet the rising expectations of the consumer base.

Bridging Business and Technology In my piece for BAI, Smartly Connecting Business and Technology to Unlock Banking Value, I highlighted a critical barrier to innovation: the disconnect between business and technology teams. As we move into 2025, the industry will continue navigating these tensions. Whats Next?

It also analyzes how focusing on the customerexperience can help prevent such fraud in the first place. Friendly fraud has also been on the rise because many customers now need only to tap their mobile apps to dispute charges, and fighting chargebacks by proving payments are valid can be cumbersome and costly for restaurant operators.

The idea, according to Senior Vice President of CustomerExperience Shea Jensen, is that “shopping today may not always mean going to a store and looking at a vast amount of inventory.” The estimated valuation of the global connected retail market by the end of 2025 is $82.31

Governments may not be known for keeping up with cutting-edge technology, but that doesn’t mean they don’t take note of the trends — especially when it comes to tools for collecting revenue. percent between 2018 and 2025, a number of local governments are adopting the technology to accept fines and taxes more easily.

The sharing economy is projected to reach more than $300 billion in global revenue by 2025, yet identity verification provider Jumio found that one in five adults using sharing services feel insecure. Governments and organizations around the world are also seeking biometrics identity verification technology to authenticate credentials online.

Prediction: A $100+ billion bank will acquire a smaller BaaS-focused bank in 2024 to accelerate its entry into the BaaS market and then bolster that acquisition by adding a healthy dose of technology, compliance and business development resources to the BaaS bank. The “employee experience” will be an area of focus. money) is.

“Kroger is excited to enter Florida to redefine the customerexperience through our industry-leading partnership with Ocado,” said Rodney McMullen, Kroger’s chairman and CEO. Its model is being duplicated in Groveland and will continue in cities across the U.S., the release said.

and about an 80%+ return spent on reducing customer churn, increasing lifetime value and/or helping cross-sell. In comparison, investments in new technology or new business lines pale in comparison to other strategic investments due to the time and effort it takes to get a business line off the ground.

Key Takeaways At many financial institutions, a substantial share of the IT budget is tied up in technology infrastructure and maintenance and cannot be used for new initiatives. Technology spending priorities. Banks spend about 7 percent of revenues on information technology, the report’s authors estimate.

The future of financial services will be shaped by the ability of financial institutions to extract and deliver more customer value from data. The convergence of mobile, cloud, and IoT technologies continues to create new opportunities for institutions to deliver personalized and contextual financial services.

It would do that by using technology, design, and data science to provide a customerexperience that would generate its publicity. As a result, the Average Cost to Serve Per Active Customer dropped 20.4% They underinvest in pre-purchase advertising and overinvest in the customerexperience.

billion by the year 2025, according to researchers. The company plans to use the money grow into Asian markets and invest more in AI and behavioral analytics technology, according to CEO Rob Mullen. The eCommerce experiences that the company provides include chatbots, selectors, carousels and calculators, among other things.

It’s a way for banks to speak with each other, and it started to be phased in during the first quarter of this year with the goal of a complete conversion by 2025. Enhanced CustomerExperience: With its rich data capabilities, banks can offer better services to their customers.

Call centers are starting to move away from KBA as new technologies emerge. ATO attempts are on the rise in these facilities, especially as bad actors gain access to newer technologies. Biometrics, which verify customers’ identities through different factors inherent in their voices, are particularly useful for call centers.

Banks are depending on the cloud to build better systems for the future, but legacy technology is holding 62% of them back. Continued adoption of GFT’s approach to reimagining banks’ current technology with core digital solutions moved the company up 14 spots this year, ranking #35 and earning recognition as a “Fast Track Fintech.”.

In a survey by Zynstra , some 65 percent of retailers said they pegged mobile payments as their top priority for in-store technology, Chain Store Age reported. In addition, mPOS systems can provide smoother customerexperiences and allow retailers to make better staffing decisions, according to the PYMNTS May mPOS Tracker.

Delivering a better customerexperience is not the only way for banks to gain a competitive advantage. This question encompasses the actual product (or service) itself, the quality of the customerexperience in acquiring and using the product, and the pricing of the product. What : CustomerExperience is Not a Strategy.

Such insights can also help firms improve customers’ experiences and lower operational costs. . These businesses’ strategies are often hamstrung by legacy fraud solutions that rely on data warehouse technology. Role Of Human Analysts. This is a problem that can be easily remedied.

A 2020 Accenture report – ‘Securing the Digital Economy: Reinventing the Internet for Trust’– forecasts that nearly $350 billion could be lost by the financial services industry to cybercrime by 2025. Financial firms have been using data to gain insights and deliver competitive services. 2) Cisco Zero Trust.

Evolution in technology has always had a big impact on how people live their lives, but this phenomenon has arguably been more pronounced in the 21 st century than at any other time in human history. billion by 2025. Could digital wallets reinvent the customerexperience? million in 2016 to US$38.8

This growth is reflected across all areas of retail as online shopping becomes more popular with consumers, forcing even more traditional retailers — such as those that sell luxury products — to craft an online experience. By 2025, online luxury sales are expected to triple, leading to an anticipated $91 billion in sales, one report noted.

Meanwhile, technology changes continued at a breakneck pace, with generative AI the biggest topic around management tables. The specifics are unclear, but bankers recognized that this will be an absolute game-changing technology in future years, and delivery will change in ways we can’t even conjure yet.

As technology advances and consumer expectations shift, staying ahead of these trends is crucial for success. Payments Trend #1: AI-Driven Payment Innovations The landscape of payments and financial services in 2025 will be marked by groundbreaking innovations and user-centric designs powered by Generative AI (GenAI).

Certainly brand, technology and unique assets like patents play a huge role in what drives a company’s overall price-to-book value or “intellectual capital.” It also includes the health of the culture and how it positively impacts customer loyalty and performance. What’s noticeable? price-to-book value. If so, which ones?

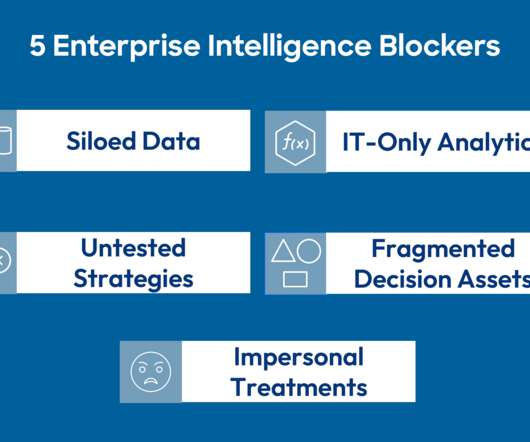

Enterprise intelligence that powers digital customerexperiences has never been more advanced — so why are 70% of digital transformations floundering? Accenture says that 85% of companies have a digital transformation effort underway; IDC projects that companies will spend another $10 trillion between now and 2025.

The pandemic shift to digital onboarding that increasingly uses intelligent automation will provide banks with cost savings of over $460 million over five years, and improve customerexperience.

We estimate that in five major retail banking businesses (consumer finance, mortgages, SME lending, retail payments and wealth management) from ten to 40 percent of revenues (depending on the business) will be at risk by 2025, and between 20 and 60 percent of profits, with consumer finance the most vulnerable.” A more digital business.

I had my phone with me and wondered if contactless payment technology would help me pay for a bucket of driving range balls. I was thinking to myself, “There is no way this bolt-on technology contraption is going to work.” And as with any emerging technology, there are inherent risks that should be understood.

During 2021, we saw the optimization of the customerexperience top the agenda within organizations. For fraudsters, this sharp and hasty shift to digital and the intense focus on customerexperience has opened doors. Globally, it’s expected to be the cause of losses to online payment fraud reaching $206 billion by 2025.

And finally, operationalizing the insights at scale to create bespoke, “in moment” customerexperiences. Simulation allows anyone to experiment with hypothetical scenarios and accelerate both learning and innovation. Applying advanced analytics and machine learning techniques. Adding in business constraints.

From healthcare to education to entertainment to manufacturing, technology innovators are stepping forward to help answer that question. In some cases, the technological changes inspired by Covid-19 will come in the form of an acceleration of existing trends — for example, industrial automation and contactless payments. Teletherapy.

The major themes of fraud, artificial intelligence (AI), expansion of instant payments, open banking, and regulation were particularly relevant to your roles as executives, risk managers, compliance officers, and technology leaders. More states require greater disclosure and control over what banks and card processors can charge.

Now, with the addition of kiosks, the burger chain is turning its eye to customerexperience and choice. According to PYMNTS’ Kiosk and Retail Report, a USA Technologies collaboration , the U.S. Overall, revenue from “intelligent vending machines” is projected to reach almost $12 billion by 2025, noted the report.

According to Goldman Sachs , machine learning and artificial intelligence (AI) will enable $34 billion to $43 billion in annual “cost savings and new revenue opportunities” within the financial sector by 2025. Bank’s offerings, advisors could quickly provide relevant information, enhancing the overall customerexperience.

The inability of banks to effectively do relationship- and market-driven pricing put an undue burden on customer acquisition and retention efforts. A Republican administration in 2025 might alleviate some of the regulatory pressure, but—for the longer term—the U.S.

The company has another hook that differentiates it from competitors: technology. Amazon recently rolled out an online research tool called the Amazon Pet Profile to help customers better understand their pets’ needs and deliver tailored content to make the shopping experience more friendly and efficient.

Key topics covered in this post: Regulatory compliance & CFPB 1071 Managing profitability for interest rate dynamics Continued risk in CRE Small business lending opportunities Top-of-mind topics for lenders and credit risk professionals As financial institutions enter 2025, the lending and credit risk landscape is evolving rapidly.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content