This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In the July Digital-First Banking Tracker® , PYMNTS explores the latest in the world of digital-first banking, including the long-lasting effects brought on by the pandemic, the shifting attitudes surrounding ATM use, and how the digitalbanking development field is reaping dividends from the financial industry’s sea change.

Consumers moved to digitalbanking in droves during the early months of the COVID-19 pandemic — it appears they are not moving back. Consumers pivoting to online banking are also more concerned over the privacy and security of their data, especially as fraud volumes creep up —and financial regulators are taking notice.

The latest PYMNTS Digital-First Banking Tracker , a collaboration with NCR Corporation , unclouds a blurry picture where 70 percent of consumers in a recent survey reported visiting a bank branch in the past month, and yet foot traffic keeps dropping as digitalbanking climbs. Solving the Branch Conundrum.

The new digitalbanking solution offers flexible tools to help people manage their finances when they have multiple income streams coming in from contract work and freelance gigs. workforce by 2027. “Unfortunately, some traditional institutions aren’t adapting.

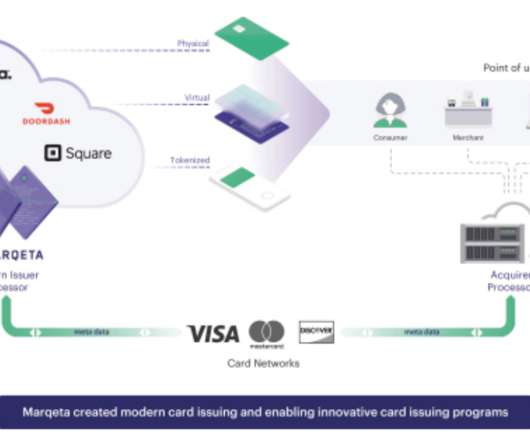

Digitalbanks : Square uses Marqeta for its cash app and merchant debit card. . Under the current agreement with Sutton Bank, Marqeta earns 100% of the interchange fees. Marqeta pays Sutton Bank a fixed percentage of each transaction. The partnership expires in 2027 and renews in 2-year terms.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content