This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Adhering to Payments Card Industry (PCI) Data Security Standards (DSS) is an unavoidable requirement for any and all eTailers that accept card payments, but a surprising number of firms are not up to speed on these standards. The need for digital security has never been more paramount than during the COVID-19 crisis.

Consumers pivoting to online banking are also more concerned over the privacy and security of their data, especially as fraud volumes creep up —and financial regulators are taking notice. Banks are continuing their ongoing movement to the cloud even as data and security questions continue to grow. Around The Cloud Banking World.

ATMs have come full circle — starting life as the best tech innovation the public had ever seen (from banks), then becoming utterly routine, and to the present day — when ATMs are suddenly sexy again. Innovations like easy PIN authentication turn a debit card into a valid ID when using the ITM.

percent by 2027, when it will reach a total valuation of $87.6 As the demand for digital payments surge, however, the systems that used to keep them secure are falling short. The pandemic is driving consumers online to shop and pay, and expansion of the payment gateway market shows no signs of slowing.

In May 2007, Voice Commerce, the voice biometrics company he founded in 2003, launched VoicePay, the consumer-facing application of the company’s secure voice-initiated transactions processing platform. that resulted in the reduction in the number of clearing banks to four, the incredible rise in FinTech innovation in the U.K.

By the year 2027, the expectation is that those costs will have swelled to $6 trillion annually or roughly $17,000 per citizen or 19 percent of the GDP. We securely store over 18 petabytes of sensitive data — this is a significant amount of data that we’re dealing with every day,” she said. Healthcare in the U.S.

trillion by 2027, and more than half of all eCommerce shoppers buy from merchants abroad. Merchants must also develop strategies for mitigating the frictions that go along with sending and receiving funds across borders, such as fraud and data security risks, exchange rate volatility and chargebacks.

Among traditional players, some of the more innovative companies are leveraging their large customer bases to incorporate this technology into their portfolios, thus allowing customers to engage in transactions that would otherwise become out of reach, both for the customer and the financial institution. In another example, Santander U.K.

workforce by 2027. Freelancer marketplaces like Toptal will need to keep a close eye on industry changes and be ready to provide the latest swift, secure options to their talent pools. Many professionals, largely driven by the appeal of flexibility, are meanwhile choosing to become independent workers.

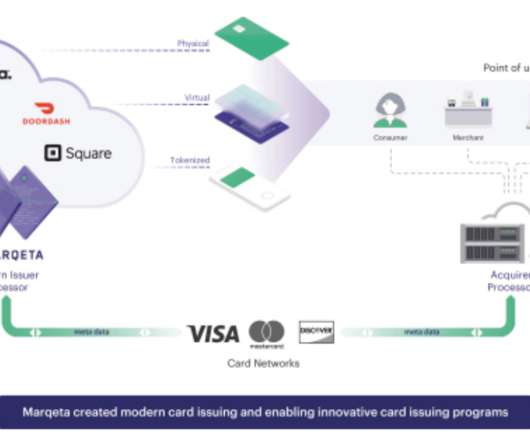

Creating a modern payments ecosystem in an industry that’s been slow to innovate . First, the acquirer-facing side of payments, which allows merchants to accept payments, has seen significantly more innovation over the last decade than the issuer-facing side, which allows businesses to customize card products for their end users.

The ISO 20022 standard, which will be the global standard for payments, securities, collateral, and trade finance, will increase payment accuracy and delivery while reducing fraud. Banks with open banking ambitions should adopt this language standard to increase interoperability, efficiency, security, and customer experience.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content