This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Manual back-end steps bog down loan approvals Financial institutions can make financial analysis, risk rating, pricing, and other steps for processing small business loans less painful. Among large banks, 42% currently use financial technology in small business lending, compared to 30% of small banks, according to the FDIC.

Increasing efficiency of compliant AML investigations To boost AML program productivity and keep pace with evolving compliance demands, financial institutions should focus on strategic operational improvements paired with the smart use of technology. See tailored AML/CFT solutions that can improve your compliance. Learn more 1.

The five federal agencies are: the Consumer Financial Protection Bureau (CFPB), the Federal Deposit Insurance Corporation (FDIC), the Federal Reserve Board (Fed), the National Credit Union Administration (NCUA) and the. Textual analysis. Office of the Comptroller of the Currency (OCC).

Reduce approval layers According to the FDIC, 73% of banks have at least three levels of approval for small business loans. Simplify underwriting criteria and eliminate unnecessary documentation. 62% even require board approval. Removing excessive approval layers can significantly speed up loan decisioning.

In various press releases, the Federal Deposit Insurance Corporation (FDIC) has highlighted that an estimated $16.3 billion of the total cost incurred from the failures of Silicon Valley Bank (SVB) and Signature Bank was designated for safeguarding uninsured depositors. Commencing with the first quarterly assessment period of 2024 (i.e.,

Account for the details before your FDIC bank acquisition Consider these tips for assessing your institution and a to-be-acquired institution for a smooth integration You might also like this webinar, "Valuation and purchase accounting: Navigating the changing M&A landscape."

The Federal Deposit Insurance Corporation (the “FDIC”) has published a request for information in the Federal Register (the “RFI”) seeking comment on approaches it uses, or is considering using, to analyze the effects of its regulatory actions and rulemaking. The format and presentation of regulatory analysis.

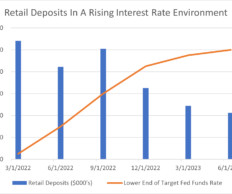

Retail Deposits Defined The FDIC classifies retail deposits as demand or term deposits placed within an FDIC-supervised institution by a retail customer or counterparty, excluding brokered deposits. 2Q 2022, first quarter 2023) and upward (3Q 2022) far more sharply than retail deposits.

This analysis helps both current and potential clients understand the resilience of different deposit types to rising interest rates. Transaction Accounts Regulators classify transaction accounts under the Monetary Control Act of 1980 and the Federal Reserve Regulation D for federal reserve requirements on deposit liabilities.

The FDIC has issued the March 2022 edition of Consumer Compliance Supervisory Highlights which includes a description of some of the most significant consumer compliance issues identified by FDIC examiners during consumer compliance examinations conducted in 2021. Fair lending.

billion transactions for potential suspicious activity and screened more than 157 million transactions for compliance with applicable sanctions requirements. As Standard Chartered noted to BuzzFeed in the wake of the FinCEN files report: "In 2019 we monitored more than 1.2

One issue raised in the RFI is “to what extent should the CFPB be consulted by the FDIC when considering the convenience and needs factor and should that consultation be formalized?”. Whether the FDIC finds these arguments persuasive is yet to be seen.

You might also like this on-demand webinar, "Navigating uncertain times: Strategies for effective risk management and compliance." Dynamic scenario analysis One effective way of managing interest rate risk is through dynamic scenario analysis. Managing interest rate risk is a complex but essential task for community banks.

Does it address a “culture of compliance”? Culture of compliance. FinCEN issued an advisory in 2014 highlighting the importance of a strong culture of compliance for senior management, leadership, and owners within financial institutions. This includes compliance from top, to middle, to frontline leadership. Calibration.

Model risk management guidance ( FRB SR 11-7 , OCC Bulletin 2011-12 , FDIC FIL-22-2017 ) outlines that the guiding principle for validation is an effective challenge to the model design, implementation, and use. Evaluate the sensitivity analysis performed and identify studies missing that might have a material impact in the model.

On March 23, 2020, the FDIC’s Office of Minority and Women Inclusion (OMWI) announced that it will request 2019 diversity self-assessments from FDIC-regulated financial institutions. The FDIC regulates insured state banks that are not members of the Federal Reserve System and insured state thrifts.

The OCC and FDIC have issued a joint proposal to revise their regulations implementing the Community Reinvestment Act (CRA). Although the Federal Reserve, OCC and FDIC, are the primary CRA regulators, the Fed did not join the proposal and presumably will issue a separate proposal. ” Click here to register. Our thoughts.

The OCC, Federal Reserve Board, FDIC, NCUA and CFPB have issued an “ Interagency Statement on the Use of Alternative Data in Credit Underwriting.”. The statement sets forth the agencies’ recognition of the benefits of using alternative data (AD) in credit decisions.

Probability of default and how it's used for expected loss Probability of Default/Loss Given Default analysis is a method used by larger institutions to calculate expected loss. Now that it’s implemented, it’s crucial to ensure ongoing compliance and efficient management of the allowance for credit losses (ACL).

according to FFIEC and FDIC data. Technology can help streamline and automate many manual lending processes, reduce compliance costs, and enhance risk management. Technological changes in the banking industry have allowed for better product delivery, data analysis, and back-office efficiency,” the report states.

The Q1 2023 compliance date is near for smaller SEC-reporting financial institutions and private or not-for-profit banks and credit unions, and progress is decidedly mixed, according to the Abrigo 2022 CECL Survey. What are their biggest challenges with the current expected credit loss model?

Reducing costs but appeasing regulators seems like an oxymoron, yet, many AML compliance and operations leaders are being asked to do just that. They even mentioned that these approaches “can maximize utilization of banks’ BSA/AML compliance resources.” But is it possible? Federal encouragement starts now.

The FDIC provides a listing of resources that can be used to better identify and mitigate potential cyber-risks. Information Sharing and Analysis Centers (ISACs). The FDIC encourages subscribing to these various groups to ensure that you receive regular security alerts, tips, and other updates. FBI InfraGard.

While the FDIC and Federal Reserve did not join the OCC in releasing this rule, they have released their proposed rule. Bank assessments aim to be a “complete picture” analysis of their activities and how they are serving their communities. Key Takeaway. Revised Reporting Guidelines.

The OCC acted alone in issuing the final CRA rule without waiting to achieve consensus with the FDIC, the agency with which the OCC had jointly issued the proposed rule. Until the compliance date is reached, banks must continue to comply with parts 25 and 195 of the OCC’s regulations (12 C.F.R.

However, regulators themselves have been criticized for encouraging de-risking by driving highly risk-adverse decisions by FIs, who are unwilling to take the chance and assume the compliance costs of doing business with specific customers who may in fact be “legitimate,” but whose risk profile is deemed to be high due to their group affiliation.

While the FDIC and Federal Reserve did not join the OCC in releasing this rule, they have released their proposed rule. Bank assessments aim to be a “complete picture” analysis of their activities and how they are serving their communities. Key Takeaway. Revised Reporting Guidelines. ” CRA Blog.

sent a letter to federal regulators Monday requesting an analysis of bank trading data that is being collected as part of the Volcker Rule. Carolyn Maloney, D-N.Y.,

Banks such as TD, Wells Fargo and Bank of America drew attention this year for money-laundering issues. That's one of several top regulatory news items in 2024.

Consumer Lending Laws & Compliance Financial institutions offering consumer loans need to know about these major consumer lending laws and recent compliance issues. Takeaway 1 Risk tied to consumer lending compliance has been elevated as a result of the pandemic and associated operating challenges. Pandemic Issues.

The changing of the guard at the Consumer Financial Protection Bureau and hope among bankers for mergers and acquisitions activity are popular items this month.

Commercial real estate loans have been integral to the success of many small banks. Long before the Great Recession made everyone in the banking industry rethink nearly everything about how they did business, numerous community banks were highly dependent on CRE loans for revenue.

A memorandum issued by the Office of Management and Budget entitled “Guidance on Compliance with the Congressional Review Act” creates a new “speed bump” for final rules issued by the CFPB as well as other independent regulatory agencies such as the Federal Reserve, the FCC, the FDIC, the FTC, and the OCC.

A memorandum issued by the Office of Management and Budget entitled “Guidance on Compliance with the Congressional Review Act” imposes a new review process on final rules issued by the CFPB and other independent regulatory agencies such as the Federal Reserve, the FCC, the FDIC, the FTC, and the OCC.

The letter was conditioned on Upstart’s agreement to a model risk management and compliance plan that required it to analyze and address risks to consumers, and assess the real-world impact of alternative data and machine learning. The Bureau issued its first (and so far only) no-action letter in September 2017 to Upstart Network Inc.

The CFPB cited prior Federal Reserve and FDIC guidance and its recent consent order related to ASPN overdraft fees. CFPB Compliance Bulletin 2022-06 also addresses the practice of charging a fee for returned deposited items.

Although the OCC’s CRA final rule technically became effective on October 1, 2020, it provides transition periods for compliance based on a bank’s asset size, type of charter, and business model.

A California federal district court judge has rejected challenges to the OCC’s and FDIC’s Madden -fix rules brought in two separate lawsuits by state attorneys general. Section 7.4001(e) and the FDIC rule is codified at 12 C.F.R. The OCC rule is codified at 12 C.F.R. Section 160.110(d). In People of the State of California, et al.

The time is ripe for Congress and the president to shrink the Federal Deposit Insurance Corp.'s s board of directors back down to its original three members, removing the Consumer Financial Protection Bureau's seat.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content