This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This article covers these key topics: Updates to CRA compliance requirements CRA compliance by bank size: W hats required ? How data analytics can simplify CRA compliance Complying with enhanced CRA data requirements Most banks recognize that their enterprises can only thrive if their customers do , too.

During the webinar, experts shared data and insights about CRE lending trends and offered advice for managing related risks. As Trepps analysis highlighted, their reliance on relationship-driven lending and tighter funding conditions make their experiences more nuanced.

Manual back-end steps bog down loan approvals Financial institutions can make financial analysis, risk rating, pricing, and other steps for processing small business loans less painful. This article covers these key topics: Cultivating fertile ground for small business lending Do large lenders have an advantage in small business lending?

Bank and credit union leaders can use data to inform small business lending Small businesses are showing resilience. As rates stay high, concerns about credit risk and borrower health are top of mind for bank and credit union leaders, especially as it relates to lending to small businesses. Interest coverage ratios have stayed strong.

Boost your small business lending efforts from the bottom up Small businesses play a crucial role in our economy, and one of the critical factors in their success is access to funding. You might also like this guide for smarter, faster small business lending.

Understand and meet borrower expectations For community financial institutions (CFIs), small business lending presents both a challenge and an opportunity. Understanding what small businesses need from a lending partner is the first step in improving loan decisioning. According to Kirby, speed is the top priority.

Abrigo's most popular whitepapers and checklists on lending and credit risk Abrigo experts' insights on CFPB 1071, loan policies, and risk ratings were popular with banking professionals. Watch NOW Takeaway 1 Abrigo's experts produced many pieces on lending and credit risk to provide strategies and tools to help banking professionals.

Develop an MBL program while mitigating risk Credit unions looking for alternate paths to growth in today's rising rate environment may be primed to leverage member business lending. Takeaway 3 The specific policy areas outlined below should be carefully considered by credit unions engaged in member business lending.

Loan Decisioning Allows Small Business Lending to Grow Community financial institutions can leverage automated loan underwriting to increase small business lending and achieve consistency. . Takeaway 2 Loan decisioning allows institutions to efficiently allocate credit analysts’ time for profitable small business lending.

What an LOS Is, and How It Benefits CFIs A loan origination system automates and manages the lending process to address common challenges. Takeaway 1 The lending landscape is increasingly competitive and the process is frustrating. Compliance. You might also like this report on commercial loan automation systems DOWNLOAD.

Credit and Lending Software Overcome Common Lending Problems Banks and credit unions that leverage an integrated lending and credit platform reap the benefits of a consistent, efficient and defensible lending program. Lending and Credit Software. Would you like other articles like this in your inbox?

This information can identify areas of need and develop targeted lending programs that address those needs. Additionally, financial institutions can integrate data from their internal systems, such as loan origination and servicing systems, to better understand their lending activities.

With the National Credit Union Administration issuing its final member business lending (MBL) ruling as of January 2017, credit unions are seeing increased flexibility in their lending limits. Automated analysis and administration Processing several loans manually can be time-consuming and increases the risk of human error.

Regulators the world over are beginning to take a closer look at the alternative and marketplace lending business model. Also, in China, analysts at Yingcan Group pointed to the government’s P2P and marketplace lending crackdown as being likely to shrink the industry by as much as 70 percent this year. In the U.S., In June, the U.K.’s

Banking institutions are responding by integrating advanced technologies, particularly artificial intelligence and data analytics, into their lending operations to enhance efficiency and adaptability. Facilitation of embedded lending while ensuring compliance: Embedded finance initiatives must adhere to regulatory requirements.

Takeaway 2 Process management features of a loan origination system help manage the workflow, from analysis through closing. Basic functions of a loan origination system When evaluating a loan origination system, lenders are rightly concerned with three major areas: the customer or member experience sound lending practices efficiency.

Lending-as-a-service company ezbob is rolling out a new solution designed to enable banks to more easily onboard clients and manage their Know Your Customer (KYC) due diligence. 12) said ezbob’s lending platform now includes a module that allows financial institutions to automate the customer onboarding process.

Lending Tech With Almost Steady Grades (Even With Rough Semesters). Mortgage services provider ICE acquired mortgage services provider Black Knight bringing together the two largest providers in the space.

The Hong Kong Monetary Authority has, as finews.asia reported this past week, amended its credit risk management guidelines in a way that seeks to boost the embrace of analytics when lending to smaller firms. The solution ensures compliance with the second payment services directive (PSD2).

Our risk and regulatory compliance experts, Carl Aridas and Chandni Patel, have just returned from XLoD 2024 in New York. Conquer Compliance The insights that Carl and Chandni gathered at XLoD highlight the ongoing evolution within the industry.

In a survey of community banks and credit unions at the 2016 Sageworks Risk Management Summit, 42 percent of respondents said Commercial Real Estate, or CRE, lending was their primary focus for loan portfolio growth. For many, commercial real estate lending may be the ticket. For many, commercial real estate lending may be the ticket.

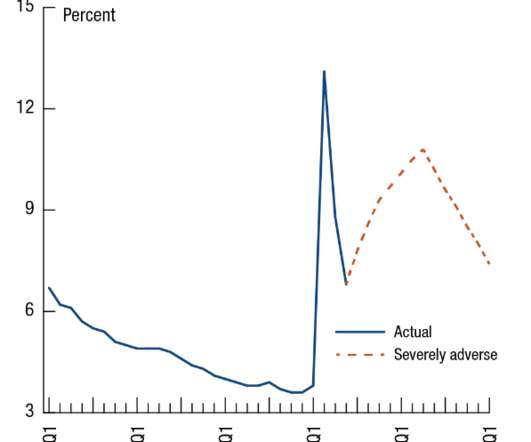

Federal bank regulators work together to design Comprehensive Capital Analysis and Review (“CCAR”) stress tests that are designed to ensure that even in the case of a severe recession, significant banks can lend to households and businesses. dollar against those countries’ currencies.

They should be knowledgeable of both sound lending practices and their own institution’s specific lending guidelines. In addition, they should be familiar with pertinent laws and regulations affecting credit and lending activities. But what if the minimum expectations are set so high that it discourages wannabe loan reviewers?

While regulators had transparency and financial security in mind when introducing more stringent requirements for banks following the global financial crisis, financial institutions faced a sudden surge in the burden compliance. The Key To Compliance Is Data.

Adapt to a dynamic banking environment with real-time lending & credit data Lender dashboards and reports showing the lending pipeline, pricing trends, emerging risks, workflow bottlenecks, etc. Ironically, data for making lending and credit decisions for the financial institution can also be one of the toughest assets to harness.

The Fed’s Comprehensive Capital Analysis and Review (“CCAR”) stress tests are designed to ensure that large banks are able to lend to households and businesses even in a severe recession. In 2020, the Federal Reserve found that large banks were generally well-capitalized under a range of hypothetical events.

The gen AI consultant can talk intelligently about leadership, bank performance, financial structuring, marketing, lending, legal, compliance, and deposits. Complexity Because AI can handle data and input from a variety of sources, it provides the most significant time savings compared to human analysis.

The Financial Stability Board says Basel III rules have not led to a squeeze of the small business bank lending market, according to reports on Friday (June 7). The FSB announced Friday the findings of its analysis of Basel III regulations on the small business lending space.

The implementation of Section 1071 of the Dodd Frank Act brings a significant shift in reporting requirements for small business lending. It’s crucial to understand upcoming compliance dates and how technology can aid your financial institution in fulfilling these new obligations for data collection and reporting.

Learn how a core deposit analysis helped improve this institution's forecasts. One way to find out is by allocating surplus budget money to a core deposit analysis. In a competitive lending environment, many banks and credit unions are concerned about losing good-quality loans if they over-price them. Lending & Credit Risk.

We conducted an analysis of consumer behavior patterns and […]. We wanted to know the answer to that critical question, so Credit Sesame partnered with Megan Hunter Antill and Jessica Yu, Ph.D., candidates in Quantitative Marketing at Stanford Graduate School of Business, to find out.

It's about ensuring that every aspect of your lending operation is optimized for efficiency and effectiveness. Assign clear responsibilities and establish accountability at all levels—from mechanics and calculations to analysis of covenant breaches. Talk to a specialist to learn more.

AAR is the global leader for online news, product and innovation information on risk, compliance, and trading. The products featured in the report include: · Credit Analysis. The annual report features Sageworks as a credit risk software vendor alongside global technology and financial leaders SAS and UBS Delta. Loan Administration.

Such tools are being used to automate the development of risk profiles, identity verification and data analysis — areas that are key to ensuring quick and secure verification before funds are disbursed. Instant Payment Challenges In Online Lending. The Digital Lending Approach And Real-Time Payments.

Community banks are critical to ag lending and small business lending. Additionally, community financial institutions are more likely to leverage relationship lending to help smaller businesses obtain loans that they might not be able to secure with larger institutions based solely on their financial information. SBA Lending.

This workflow process also allows for the identification of patterns that may single out a deficient closing agent or branch that needs to strengthen documentation compliance. As each step is completed, the process will move forward until the analysis and risk grade assignment are approved.

Retail banks respond to the Federal Reserve’s short-term interest rate adjustments with corresponding changes in lending and deposit rates. This analysis helps both current and potential clients understand the resilience of different deposit types to rising interest rates.

Given the task is often assigned to the Chief Credit Officer or other leaders within the credit department, developing a stress testing methodology may come at the risk of losing steam on other areas, even business development if the stress tester is also responsible for lending. Why are top down stress tests valuable to the institution ?

Takeaway 1 BSA and fraud functions have historically been siloed, and IT has been external to compliance. Takeaway 3 Cyberattacks are also on the rise, lending even more importance to communication and collaboration among the BSA, fraud, and IT functions. Increased cybercrime requires all three to collaborate.

Case Study: SBA Lending – The Traditional Approach Small Business Administration (SBA) loan production is the perfect example of a business line that screams for digitization. Banks will tend to transform consumer lending instead of tackling all of lending or all of onboarding. This is an example of scalability in banking.

One of the principles underlying the Basel Committee on Banking Supervision’s December 2015 supervisory guidance on accounting for expected credit losses is that “A bank should have a credit risk rating process in place to appropriately group lending exposures on the basis of shared credit risk characteristics.”

Abrigo Connect provides curated insights into your customer base and sources of risk, including in-depth analysis of alerts, cases, SARs, CTRs, and transaction volumes to streamline and enhance board reporting. Stay up to date on the CFPB 1071 data collection rule and other lendingcompliance topics.

Focus loan reviews on risk in the portfolio Continuous loan review monitoring helps banks and credit unions ensure credit review systems support safe and sound lending. discussed how they use continuous monitoring in their efforts to ensure safe and sound lending practices.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content