This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Manual back-end steps bog down loan approvals Financial institutions can make financial analysis, risk rating, pricing, and other steps for processing small business loans less painful. Among large banks, 42% currently use financial technology in small business lending, compared to 30% of small banks, according to the FDIC.

In the wake of regional bank failures, one potential answer to equity shorting and bank runs is having the FDIC increase deposit insurance. We believe any change to the FDIC insurance coverage should aim to maintain and advance our credit markets. There is no escaping this conclusion: FDIC insurance promotes risk-taking by managers.

Lenders and credit analysts must organize into one cohesive credit memo the following: borrower information, financial ratios, any global cash flow analysis, the assigned risk rating, proposed loan pricing, and terms of the proposed loan. The rating for a loan should represent the sum of the earlier information and analysis provided.

The five federal agencies are: the Consumer Financial Protection Bureau (CFPB), the Federal Deposit Insurance Corporation (FDIC), the Federal Reserve Board (Fed), the National Credit Union Administration (NCUA) and the. Textual analysis. Office of the Comptroller of the Currency (OCC).

FDIC officials in March outlined several types of weaknesses in loan underwriting, administration and oversight practices that are emerging at some banks with CRE portfolios. Eberley, director of the FDIC's Division of Risk Management Supervision wrote in the publication.

In various press releases, the Federal Deposit Insurance Corporation (FDIC) has highlighted that an estimated $16.3 billion of the total cost incurred from the failures of Silicon Valley Bank (SVB) and Signature Bank was designated for safeguarding uninsured depositors. Commencing with the first quarterly assessment period of 2024 (i.e.,

On May 31, the Federal Deposit Insurance Corporation (FDIC) reported to the public what many banks already knew and had been experiencing for the past year – that deposits are declining in the American banking sector. There has almost been $1.2 Trillion removed from the banking system over the past year.

FDIC-insured “Problem Banks” list has been increasing over the past two years. We considered 18 variables to explain the statistical significance using a T-test analysis between the positive and negative ROE bank group with a p-value of 0.01. The summary of our analysis appears in the table below. Bank ROE is now a problem.

Reduce approval layers According to the FDIC, 73% of banks have at least three levels of approval for small business loans. Simplify underwriting criteria and eliminate unnecessary documentation. 62% even require board approval. Removing excessive approval layers can significantly speed up loan decisioning.

As of January, there were 3,989 in-store branches of FDIC-insured institutions housed within retail stores, a decrease of 2.3% In-store branches are satellite bank branches located inside large retail spaces, such as supermarkets or chains like Walmart and Safeway. since June 30, 2019, and 6.5%

The Federal Deposit Insurance Corporation (the “FDIC”) has published a request for information in the Federal Register (the “RFI”) seeking comment on approaches it uses, or is considering using, to analyze the effects of its regulatory actions and rulemaking. The format and presentation of regulatory analysis.

Account for the details before your FDIC bank acquisition Consider these tips for assessing your institution and a to-be-acquired institution for a smooth integration You might also like this webinar, "Valuation and purchase accounting: Navigating the changing M&A landscape."

In addition, he noted, a recent consent order from the FDIC required an institution with assets below $1 billion to ‘establish satisfactory quality control procedures over the alert clearing and investigation process. Abrigo Advisors expect this emphasis on quality control will be a theme during exams —even at smaller institutions. “Our

The FDIC today released a new staff study highlighting how economies of scale developed at community banks (those with $10 billion or less in assets) between 2000 and 2019. The post FDICAnalysis Examines Community Bank Economies of Scale appeared first on ABA Banking Journal.

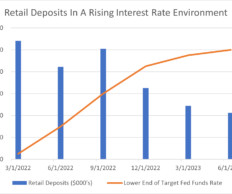

Retail Deposits Defined The FDIC classifies retail deposits as demand or term deposits placed within an FDIC-supervised institution by a retail customer or counterparty, excluding brokered deposits. 2Q 2022, first quarter 2023) and upward (3Q 2022) far more sharply than retail deposits.

The plain language of the governing federal statute applies only to interest that an FDIC-insured state bank may charge. Allegedly, the FDIC’s rule represents an expansion of the FDIA’s preemption of state law interest rate caps by extending the preemption to assignees of loans originated by such banks.

Second, the hedge provider must be an FDIC insured institution and structure its hedges as a qualified financial contract (QFC). We see substantial risk to community banks in dealing with non-FDIC hedge providers or those that do not offer QFC protection – think Lehman Brothers.

Second, the hedge provider must be an FDIC insured institution and structure its hedges as a qualified financial contract (QFC). We see substantial risk to community banks in dealing with non-FDIC hedge providers or those that do not offer QFC protection – think Lehman Brothers.

More construction loan monitoring ultimately decreases loan default, according to a new FDIC Center for Financial Research working paper. While it doesn't necessarily reflect the views of the FDIC, the paper includes preliminary findings from research by FDIC staff and an FDIC Visiting Scholar. On-site inspections.

The Data Behind The Drivers of ROA In Q2/24 the number of FDIC-reporting community banks was about 4,100. To find the drivers of ROA, we consider 23 different variables, and run a correlation analysis for each variable. The table below shows our analysis for all reporting banks. Approximately 5.7%

Key Takeaways The FDIC issued an advisory to FIs encouraging safe and sound lending practices in today's ag lending environment. FDIC) issued an advisory to financial institutions encouraging exceptionally safe and sound lending practices in agricultural lending. On January 28, the Federal Deposit Insurance Corp.

Community banks are expanding their loan portfolios to include more small business loans, according to the most recent Community Bank Performance report by the FDIC. Through a Sageworks poll , we found that many institutions rely on on-the-job training for tax return analysis – one component of the credit analysis process.

Takeaway 2 Asset/liability management models use earnings or income simulation models and gap analysis to measure short-term IRR. Takeaway 3 The most common model to measure long-term IRR is an economic value of equity (EVE) analysis. FDIC) noted in its 2021 Risk Review. EAR, Gap Analysis. EVE Analysis.

Second, community banks should use FDIC-insured institutions as hedge providers, and the hedges must be structured as qualified financial contracts (QFC). We see substantial risk to community banks in dealing with non-FDIC hedge providers or those not offering QFC protection – think Lehman Brothers. Conclusion.

We covered the basics of account analysis in Part 1 ( HERE ), and in this article, we highlight best practices for managing an analyzed transaction account. For analysis, the framework can be put in a “lattice cube” with each interrelated element in a corner. Traditionally, banks have included credit charge fees into analysis.

One issue raised in the RFI is “to what extent should the CFPB be consulted by the FDIC when considering the convenience and needs factor and should that consultation be formalized?”. Whether the FDIC finds these arguments persuasive is yet to be seen.

Bankers since the financial crisis have become accustomed to seeing language like the following: “The FDIC is re-emphasizing the importance of prudent interest rate risk oversight and risk management processes to ensure FDIC-supervised institutions are prepared for a period of rising interest rates.” FDIC FIL-46-2013 October 8, 2013.

The FDIC paper The Entry, Performance, and Risk Profile of De Novo Banks published in April 2016 reports that the number of de novo bank failures and acquisitions annually has drastically declined since 2010, primarily due to the fact that new bank formations have become nearly inexistent.

Analysts note that today, the percentage of professionals working in the agricultural sector remains so low that including them in national jobs calculations would not have a statistically relevant effect on overall analysis. “As Below, PYMNTS breaks down the key data points from Reuters’ analysis on the farming sector’s banking challenge.

This analysis helps both current and potential clients understand the resilience of different deposit types to rising interest rates. Transaction Accounts Regulators classify transaction accounts under the Monetary Control Act of 1980 and the Federal Reserve Regulation D for federal reserve requirements on deposit liabilities.

By way of example: ICIJ’s analysis, according to its site , found that in half of the reports, banks didn’t have information about many of the entities that were tied to the transactions. “In Much of those revamped efforts come, perhaps not surprisingly, through advanced technologies.

The FDIC has issued its widely anticipated final rule resolving the uncertainty caused by the Second Circuit’s Madden v. Although the press release accompanying the FDIC’s final rule states that the “FDIC’s action mirrors” the OCC final rule, the two final rules are not identical in every respect. Midland Funding decision.

is set to see its first new community bank in decades, as the Federal Deposit Insurance Corporation (FDIC) lent its approval for MOXY Bank to launch in Washington, D.C. The FDIC’s announcement said a private placement offering will raise at least $25 million for the bank ahead of its launch. Bloomberg listed Casey G.

The FDIC has issued an Advance Notice of Proposed Rulemaking (ANPR) seeking comment on its regulatory approach to brokered deposits and interest rate restrictions. The FDIC’s current regulations on brokered deposits and interest rate restrictions are set forth at 12 C.F.R. Section 337.6.

The FDIC has issued the March 2022 edition of Consumer Compliance Supervisory Highlights which includes a description of some of the most significant consumer compliance issues identified by FDIC examiners during consumer compliance examinations conducted in 2021. Fair lending.

Yet the FDIC said in previous analysis that the actual volume of traditional bank loans to small businesses in the U.S. Yet the FDIC said in previous analysis that the actual volume of traditional bank loans to small businesses in the U.S. a figure it says surpasses that of many traditional institutions in the country.

On March 23, 2020, the FDIC’s Office of Minority and Women Inclusion (OMWI) announced that it will request 2019 diversity self-assessments from FDIC-regulated financial institutions. The FDIC regulates insured state banks that are not members of the Federal Reserve System and insured state thrifts.

Model risk management guidance ( FRB SR 11-7 , OCC Bulletin 2011-12 , FDIC FIL-22-2017 ) outlines that the guiding principle for validation is an effective challenge to the model design, implementation, and use. Evaluate the sensitivity analysis performed and identify studies missing that might have a material impact in the model.

I don’t understand why Professor Levitin is attacking the OCC and FDIC for filing an amicus brief in an “obscure small business bankruptcy case to which a bank was not even a party.” The brief was an exceptional piece of drafting and analysis and the banking agencies do not deserve to be denigrated for a supposed lack of class here.

I don’t understand why Professor Levitan is attacking the OCC and FDIC for filing an amicus brief in an “obscure small business bankruptcy case to which a bank was not even a party.” The brief was an exceptional piece of drafting and analysis and the banking agencies do not deserve to be denigrated for a supposed lack of class here.

In response to these complaints, the CFPB provided a list of steps that consumers can take to protect themselves, including being vigilant for signs of a scam, reporting any suspicious claims of FDIC insurance, knowing the best way to contact a platform in the event of an issue, and knowing the owners of any crypto-asset platforms used.

The OCC and FDIC have issued a joint proposal to revise their regulations implementing the Community Reinvestment Act (CRA). Although the Federal Reserve, OCC and FDIC, are the primary CRA regulators, the Fed did not join the proposal and presumably will issue a separate proposal. ” Click here to register. Our thoughts.

With the assistance of the FDIC, Fulton Financial acquired certain assets, debt and deposits of Republic Bank. This analysis does not require the ability to predict future interest rates or future cost of liabilities or cost of capital. This first bank failure in 2024 is reported to cost the Deposit Insurance Fund $667mm.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content