This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Our analysis shows that an average community bank can expect $9.7mm NPV of income (about 1% ROA) on a $100mm loan portfolio when the average loan life is seven years, versus only $5mm NPV of income (about 0.50% ROA) on the same portfolio where the average loan life is 2.3 years (both portfolios measured over a ten-year life).

During the webinar, experts shared data and insights about CRE lending trends and offered advice for managing related risks. As Trepps analysis highlighted, their reliance on relationship-driven lending and tighter funding conditions make their experiences more nuanced.

Data collection and analysis will be key to complying with the CRAs expectations for enhanced data collection, expanded assessment areas, and tiered performance evaluations, Transform CECL data into stress testing insight. Must comply with strict benchmarks for lending, investment, and community development initiatives.

Manual back-end steps bog down loan approvals Financial institutions can make financial analysis, risk rating, pricing, and other steps for processing small business loans less painful. This article covers these key topics: Cultivating fertile ground for small business lending Do large lenders have an advantage in small business lending?

Boost your small business lending efforts from the bottom up Small businesses play a crucial role in our economy, and one of the critical factors in their success is access to funding. You might also like this guide for smarter, faster small business lending.

Bank and credit union leaders can use data to inform small business lending Small businesses are showing resilience. As rates stay high, concerns about credit risk and borrower health are top of mind for bank and credit union leaders, especially as it relates to lending to small businesses. Interest coverage ratios have stayed strong.

Avoid common mistakes in your global cash flow analysis Get proficient in your global cash flow analysis efforts. Global Cash Flow analysis is used by financial institutions to assess the combined cash flow of a group of people and/or entities to get a global picture of their ability to service the proposed debt.

The basics of commercial credit analysis Learn the foundations of credit analysis, including key data analysis strategies and best practices. . For more information on the basics of credit analysis, check out this webinar: WATCH NOW. Avoid common missteps in commercial credit analysis. Setting the foundation.

How industry analysis can improve your credit risk management Understanding your customers' businesses leads to better loan pricing, structure, and risk management. WATCH WEBINARS Takeaway 1 All businesses perform industry analysis, but financial institutions in particular must know their customers' competitive landscape.

We conducted a loan performance analysis for over 5,000 individual hedged commercial loans originated by almost 400 community and regional banks across the country. Our analysis demonstrates that loan-level hedging has offered community banks a strong competitive advantage in the current interest rate environment and competitive landscape.

In the wake of the 2008 global financial crisis, and banks' subsequent pullback from the small- to medium-sized business ( SMB ) lending arena, a slew of alternative lenders emerged onto the scene to fill the credit gap. What's just as important is to ensure that lending technology is flexible.

Recent data and trends of the small business lending market SMB Lending Insights is a snapshot of current financial trends and metrics that impact small and medium-sized business (SMB) lending and financial institutions. You might also like this guide for smarter, faster small business lending.

Key Takeaways Financial institutions who want to maintain a healthy share of business lending this year and through potentially tougher economic times ahead want to be in the best position possible before trouble hits. Abrigo's Business Lending Readiness Survey found many processes stymie those efforts. learn more.

Understand and meet borrower expectations For community financial institutions (CFIs), small business lending presents both a challenge and an opportunity. Understanding what small businesses need from a lending partner is the first step in improving loan decisioning. According to Kirby, speed is the top priority.

Abrigo's most popular whitepapers and checklists on lending and credit risk Abrigo experts' insights on CFPB 1071, loan policies, and risk ratings were popular with banking professionals. Watch NOW Takeaway 1 Abrigo's experts produced many pieces on lending and credit risk to provide strategies and tools to help banking professionals.

For example, if cattle lending occurs across four markets, reviewing it holistically requires manual effort just to piece together a universe from which to draw a sample. For the first time, we could evaluate lending segments independently of the bank's organization. Adapt your credit analysis processes to address economic volatility.

Develop an MBL program while mitigating risk Credit unions looking for alternate paths to growth in today's rising rate environment may be primed to leverage member business lending. Takeaway 3 The specific policy areas outlined below should be carefully considered by credit unions engaged in member business lending.

Probability of Default/Loss Given Default analysis is a method used by generally larger institutions to calculate expected loss. PD is typically calculated by running a migration analysis of similarly rated loans, over a prescribed time frame, and measuring the percentage of loans that default.

Develop better ag lending workflows before demand picks up. A better ag lending process makes applying smoother for borrowers and can allow efficient ag loan growth without adding a lot of staff. Takeaway 1 Now is the time to plant the seeds for harvesting growth in the ag loan portfolio by creating a better ag lending process.

Loan Decisioning Allows Small Business Lending to Grow Community financial institutions can leverage automated loan underwriting to increase small business lending and achieve consistency. . Takeaway 2 Loan decisioning allows institutions to efficiently allocate credit analysts’ time for profitable small business lending.

In this article, we provide a quantitative analysis to support this conclusion. The table below shows a summary of our analysis (community banks are defined as banks under $10B in assets). The post Loan Performance Analysis – Hedged vs. Unhedged Loans appeared first on SouthState Correspondent Division.

Ready to catch the next wave of lending growth? Commercial and industrial lending (C&I) will be the next big performance driver for banks and credit unions. You might also like this paper on how institutions can produce smarter, faster lending. C&I lending will be the next “bomb.”

Months after he called out “irrational” student lending that has been impacting the economy through his annual letter, JPMorgan Chase CEO Jamie Dimon noted that U.S. student lending is “hurting America.”

Takeaway 2 A consumer loan origination system can help FIs offer a fully digital retail lending experience. How can FIs overcome retail lending challenges? In today's competitive – and increasingly digital – consumer lending environment, financial institutions will need to find ways to adapt to changing customer expectations.

Strong demand is a factor in the ag lending outlook ahead Ag lenders can begin taking steps to ensure they are prepared and can provide positive customer or member experiences. The outlook for ag lending has its share of uncertainty. Inflation, rates are factors in ag lending outlook. Farmers expect worse in 2023. Rising inputs.

Personalized Touch with Efficient Service Can Boost Lending Banks and credit unions can boost business lending by combining a relationship focus with transaction-oriented processing. . This competition can only increase as the lending landscape continues to shift.

Lenders and credit analysts must organize into one cohesive credit memo the following: borrower information, financial ratios, any global cash flow analysis, the assigned risk rating, proposed loan pricing, and terms of the proposed loan. The rating for a loan should represent the sum of the earlier information and analysis provided.

Credit and Lending Software Overcome Common Lending Problems Banks and credit unions that leverage an integrated lending and credit platform reap the benefits of a consistent, efficient and defensible lending program. Lending and Credit Software. Would you like other articles like this in your inbox?

How construction administration units mitigate construction lending risk Construction lending involves unique risks and requires specialized processes. WATCH Takeaway 1 The OCC recommends that construction lending risk be managed by specialized real estate and construction lenders who report to the credit department.

The Data Around Bank Efficiency To understand our analysis into bank efficiency, we measured the correlation coefficient between the efficiency ratio and ROA for banks between $100mm and $10B in assets at negative 0.74 (one of the highest factors driving community bank performance).

Who the competition is, what the lending competition is offering, their delivery channels, and service levels can help community banks differentiate their services and enhance their competitive advantage. However, community banks largely exclude these big institutions from their SWOT or competitive analysis.

What an LOS Is, and How It Benefits CFIs A loan origination system automates and manages the lending process to address common challenges. Takeaway 1 The lending landscape is increasingly competitive and the process is frustrating. The best commercial lending software is an LOS that can handle the entire life-of-loan process.

The Concepts Lending Curve: A yield curve shows interest rates associated with different contract lengths for a particular interest rate instrument. While economists may use the shape of the yield curve to gauge future economic strength, bankers should pay particular attention to the lending curve.

One example: a $400 million-plus bank serving customers and businesses in western Ohio and through its specialty lines of business nationwide began a project to optimize its use of Abrigos Sageworks lending and credit solutions. Find out how Abrigo helps optimize lending with small business loan origination software.

It was into this world that the much celebrated digital lending fintech OnDeck recently sold to Enova for $90 million, a virtual fire sale at way under 1X OnDeck’s revenue. They primarily support – don’t compete with – federally insured bank lending. And pricing is a unique area of analysis where there aren’t dozens of competitors.

Key Takeaways The FDIC issued an advisory to FIs encouraging safe and sound lending practices in today's ag lending environment. FDIC) issued an advisory to financial institutions encouraging exceptionally safe and sound lending practices in agricultural lending. Learn More.

Our analysis is demonstrated graphically below and further discussion follows. Despite the arguments of better service, differentiated products, or ability to lend on broader loan categories, the reality is that loans are won from other institutions on pricing or structure (neither a long-term desirable outcome for the winning bank).

Takeaway 1 Global cash flow can provide a more holistic lending picture as lending decisions have become more complex. Takeaway 2 Institutions usually leverage global cash flow analysis if a borrower has complex credits. Takeaway 3 Financial institutions should implement these best practices to effectively use CFC analysis.

Criticized commercial real estate loans soared by 144 percent, to $26 billion, according to an analysis by the Financial Times. This comes as many hotels have occupancy rates in the single digits, shopping mall traffic remains low and office workers work remotely.

On the lending side, loan rates are expected to follow prime rates down, but the spread over prime may remain higher due to lingering credit risk concerns. Risks in multifamily CRE lending remain elevated, particularly in the luxury segment. The commercial real estate office sector remains stressed.

It’s time for banks and credit unions to finally execute those C&I lending priority initiatives. Senior bank and credit union executives have ranked commercial and industrial (C&I) loans as a top lending priority over the past several years in Cornerstone Advisors’ annual What’s Going On in Banking research.

As a loan reviewer, you need to be technically sound in order to do your job, which means you need to have a fundamental understanding of financial analysis, tax analysis, and all of the regulatory laws that surround the credits that you’re going to be reviewing,” Cooley says. Credit Analysis Training. Lending & Credit Risk.

Takeaway 2 Process management features of a loan origination system help manage the workflow, from analysis through closing. Basic functions of a loan origination system When evaluating a loan origination system, lenders are rightly concerned with three major areas: the customer or member experience sound lending practices efficiency.

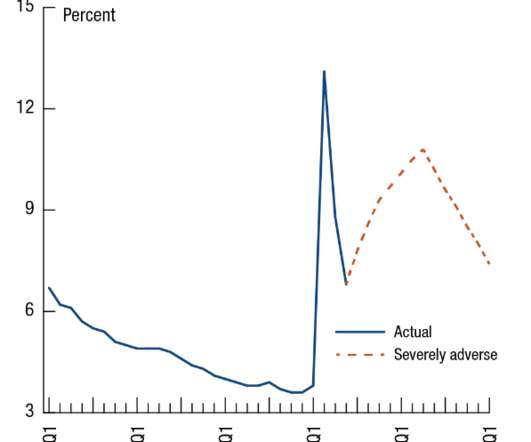

The Fed’s Comprehensive Capital Analysis and Review (“CCAR”) stress tests are designed to ensure that large banks are able to lend to households and businesses even in a severe recession. In 2020, the Federal Reserve found that large banks were generally well-capitalized under a range of hypothetical events.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content