This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Likely trends are shaped by a dynamic rate environment The top issues facing executives managing credit portfolio risk and the balance sheet at financial institutions are shaped largely by the dynamic rate environment, according to Abrigos outlook for major trends in the year ahead. Navigate rate environment uncertainty with confidence.

Every organization manages data internally that provides support in running the operations, as well as to provide enriched content to an external audience such as buyers or distributors. Finding the right tools to utilize for data analysis can be tricky and hard to understand, but resources like these can help you along the way.

Our analysis shows that an average community bank can expect $9.7mm NPV of income (about 1% ROA) on a $100mm loan portfolio when the average loan life is seven years, versus only $5mm NPV of income (about 0.50% ROA) on the same portfolio where the average loan life is 2.3 years (both portfolios measured over a ten-year life).

They also share tips for managing risk and pricing. As a result, financial institutions with CRE concentrations find it increasingly important to strategically manage the competitive pressures and risks related to origination, refinancing, and loan performance. We can help you set up stress testing that's right for your loan portfolio.

It's quite a process for marketing teams to develop a long-term data management strategy. It involves finding a data management provider that can append contacts with correct information — in real-time. Forward-thinking marketing organizations have continuously invested in a database strategy for enabling marketing processes.

How industry analysis can improve your credit risk management Understanding your customers' businesses leads to better loan pricing, structure, and risk management. WATCH WEBINARS Takeaway 1 All businesses perform industry analysis, but financial institutions in particular must know their customers' competitive landscape.

.” This article explores the methodology and shows you what this analysis means for a typical bank. How RFM Customer Segmentation Analysis Works Recency, Frequency, and Monetary value are each aspect of a customer trait that denotes some value in banking. Which of your customer segments should we market to help stem defections?

Find commercial real estate risks in the loan portfolio Sound risk management practices in commercial real estate lending help lenders manage CRE credit losses and protect the portfolio's profitability. LISTEN Takeaway 1 Effective CRE risk management involves adapting to changing market fundamentals to avoid excessive loan losses.

While every bank will take some level of credit, interest rate, liquidity, and operational risk, the question is this: Are banks in the business of taking risk to earn higher revenue, or are banks managing relationships and should avoid risk (and the higher return) when possible? Each loan would earn the bank the market clearing ROA.

Customer service should be fit for a king," Burger King exclaimed in a video about the guerilla-marketing campaign. Daniel Schröder, marketing director at Burger King Sweden and Denmark, told Adweek that the new social media push grew out of an effort to fix the chain’s own online communications with guests. Even our old friends.".

The product generates significant fees and helps drive deposit balances, yet debit cards rarely get a mention in strategy, marketing, or customer profitability circles. This is an excellent early management position for an up-and-coming banker. While there are many overlooked products in banking, the debit card is perhaps the greatest.

With the growing number of data sources and feeds about client contacts, sales and transactions – and market data from the company’s internal and external sources – the data acquisition life cycle needs to continuously be streamlined, standardized, consolidated, and monitored. Client Data Hub – Sales Intelligence.

One way to easily envision this, according to Abrigo Advisory Services Manager Manuel Aya, is to think of it as the value that arises from retaining depositors, and hence deposits, at an institution versus needing to go into the open market to fund activities. This could reduce the intangible value of deposit-related assets.

Rootstock Software , which works in providing cloud enterprise resource planning (ERP) solutions for the Salesforce platform, is partnering with digital engineering and technology firm Nagarro to break into the cloud ERP market in the U.S., Leveraging Nagarro’s ERP team, we’ll quickly extend and deepen our market reach.".

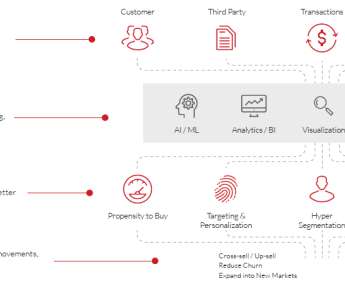

Institutions can use their data to tailor LLMs and maintain an acute pulse on their numbers, giving them an invaluable awareness of where they stand in the market against competitors. For example, using generative AI image analysis, one can determine if an image has been altered, which helps control insurance fraud and identity theft.

Key topics covered in this post: Regulatory focus Key questons for ALCOs Governance and concentration risks Expect the unexpected Regulators 'could not be more clear' Today’s regulatory climate is turning up the heat on financial institutions when it comes to liquidity and interest rate risk management.

Banks don’t have enough product managers. A manager may oversee the operation of a product, but few banks have product managers who drive product development and performance. This article further explores what it means to be a bank product manager. What is Bank Product Management?

Here are five ways financial institutions can make the most of their CECL data to help with competitive positioning, more effective pricing, asset/liability management (ALM), and other decision-making: Peer analysis and comparison We often categorize data into two types: raw/input data and the output, or enriched data.

This ALM 101 post describes the value at risk(VAR)/economic value of equity (EVE) risk perspective (long-term risk to market value of capital). Takeaway 1 Interest rate risk for financial institutions is the risk that earnings and market value may decline as market interest rates change. . It is the third in a series. .

It is the goal of Perficient’s Financial Services consultants to help financial services executives, whether they lead banks, bank branches, bank holding companies, broker-dealers, financial advisors, insurance companies or investment management firms, the knowledge to know the status of AI regulation and the risk and regulatory trend of AI regulation (..)

Takeaway 1 Interest rate risk for financial institutions is the risk that earnings and market value may decline as market interest rates change. . Takeaway 3 Two methods of measuring short-term interest rate risk are a gap analysis and, more commonly, an income simulation. ALM 101: Introduction to Asset/Liability Management.

Despite borrowing more and tapping credit lines, they're managing leverage and meeting debt obligations, according to Abrigo's proprietary data. They’re borrowing more, but they’re also managing their leverage and meeting debt obligations —even as they feel the pressure of high rates. Business credit line utilization is up.

You might also like this infographic: "6 Reasons to Update Your Core Deposit Analysis." Takeaway 2 Several challenges associated with developing assumptions for non-maturity deposits can be addressed with core deposit analysis. These are the checking, savings, and money market accounts borrowers deposit into the institution.

Navigating interest rate management in today's environment As regulators focus on interest rate risk management, read about what financial institutions can do to be ready for a rate drop. You might also like this on-demand webinar, "Navigating uncertain times: Strategies for effective risk management and compliance."

With loans, it’s hard to discern expert-level skills unless you know the market and the credit. Non-Expert Deposit Pricing Management – How To Destroy Bank Franchise Value The best way to quickly destroy value is to peg a deposit product to an index such as SOFR, Prime, Fed Funds, or Treasuries. Deposits, however, are pure.

These technologies are also used to better target marketing in retail and customize trade recommendations in wealth management. Risk Management. AI may be used to augment risk management and control practices. Textual analysis. Credit Decisions. Cybersecurity.

Film quality aside, there have been few movies in the history of the World that have done a better job at marketing than Barbie. This article highlights these lessons and applies them to marketing deposits. We will also stipulate that you don’t have $100mm to spend on a marketing budget. Marketing made it so.

In a few short months, stronger economic data (higher GDP, stronger job market, and stubborn inflation) changed the market’s and the Fed’s view on the future path of interest rates. The market and the Fed are now aligning on only one rate cut in 2024 – obviously this will change over the course of the year as the economic data evolves.

The treasury or cash management customer is usually a bank’s most profitable customer on a risk-adjusted basis ( HERE ). In this article, we discuss cash management profitability and rank the most profitable industries for banks to go after. Cash flow stability is also a factor in cash management profitability.

Last week, the American Banking Association (ABA) held its annual Bank Marketing Conference in Denver, receiving rave reviews. The theme was – developing your marketing superpowers. Amid the brewery networking, superhero costumes, and fun, some fantastic bank marketing lessons were had, and not just for bank marketers.

Key Takeaways ALM professionals often inquire about reports they can run using their ALM models to help manage their financial institutions. I’m often asked by asset/liability management professionals for advice on using ALM models to generate reports that provide meaningful information to aid in managing the financial institution.

Key Takeaways ALM professionals often inquire about reports they can run using their ALM models to help manage their financial institutions. I’m often asked by asset/liability management professionals for advice on using ALM models to generate reports that provide meaningful information to aid in managing the financial institution.

Best practices for assessing models and managing risk Sound model development, implementation, use, and validation is especially important as CECL models debut. . What are model risk management and model validation? Appropriate” and “timely” are relative concepts, so for low-risk models, an analysis might occur every three years.

My last blog dove into the customer data management challenges financial companies might encounter when starting the personalization journey. Today, I’ll address customer intelligence and the benefits it provides. It enables you to build deeper and more effective customer relationships.

The goal here is to give bankers that don’t utilize a funds transfer pricing and activity analysis methodology a glimpse into the cost of producing the most popular deposit categories. We will use their data and methods for this analysis. Cost of Deposit Sales and Marketing.

Asset/liability management basics In part 1 of this "Introduction to ALM" blog series, learn the goals of asset/liability management and how it can help financial institutions. Takeaway 1 ALM in banking means managing the cash flows of assets and liabilities to increase profitability, manage risk, and maintain safety and soundness. .

Now, banks and credit unions must determine how to safely and effectively manage risk in the portfolio while also driving growth at their institution. Therefore, it’s essential that the credit memo captures the complete picture of the borrower to ensure proper risk management. This is especially true in an economic downturn.

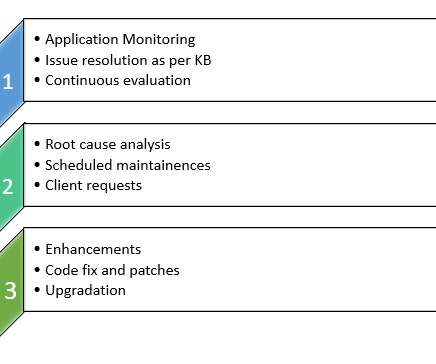

Managed service offerings (MSO) is the department in an organization responsible for all application support activities. Typically, MSO tracks and reviews weekly report on the following deliverables: Incident, problem, and change management. Level 2: Root cause analysis. Problem management and stability analysis.

OneStream is a driving force that enables financial transformation and helps organizations move to the next level of corporate performance management (CPM). It enables teams to shift more time to value-added analysis, partnering with lines of business, and improving alignment for strategic decision-making across the enterprise.

.'” The Forrester report took an in-depth look at each service provider’s strengths across three categories: strategy, current offering, and market presence. It segments each vendor by market presence and functionality to advise application development and delivery professionals on choosing the right partner for DPA implementation.

According to the report, the biggest challenge for B2B marketers this year is managing coordination with channel partners. Leading the Way: Partner Relationship Management (PRM). Streamlining partner marketing. Improving lead routing and management. Increased marketing budget efficiency valued at $1.7

DOWNLOAD Takeaway 1 A human-in-the-loop approach plays a vital role in ensuring that AI systems effectively support alert and case management for AML/CFT suspicious activity monitoring. While some alerts are simple and can easily be handled by AI, many are complex and require extensive analysis.

People have been talking about content marketing for years. The effects of good content marketing can be long-lasting, offering ongoing engagement while other tactics capitalize on shorter-term opportunities. Create a Content Roadmap and Management Systems. Content marketing is a marathon, not a sprint.

The gen AI consultant can talk intelligently about leadership, bank performance, financial structuring, marketing, lending, legal, compliance, and deposits. Gen AI excels at distilling options down to recommendations, which is helpful to management teams that are having a hard time deciding.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content