This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Avoid common mistakes in your global cash flow analysis Get proficient in your global cash flow analysis efforts. Global Cash Flow analysis is used by financial institutions to assess the combined cash flow of a group of people and/or entities to get a global picture of their ability to service the proposed debt.

When it comes to the risk management process, there is no one-size-fits-all approach. “It is as much an art as a science,” says Tim McPeak, risk management consultant at Sageworks. ” But these inconsistencies pose significant challenges to managing credit risk at financial institutions. Utilize technology.

We conducted a loan performance analysis for over 5,000 individual hedged commercial loans originated by almost 400 community and regional banks across the country. Our analysis demonstrates that loan-level hedging has offered community banks a strong competitive advantage in the current interest rate environment and competitive landscape.

In this webinar, Sageworks is teaming up with Linda Keith CPA again to bring you more great information about tax return analysis. Linda has been a guest speaker on several Sageworks webinars that covered topics like Global Cash Flow , Red Flags for Tax Return Analysis and Making Judgement Calls for Tax Return Analysis.

In this guest column, Jason Alpert, Managing Partner of Castlebar Holdings , explains how financial institutions should respond. However, given recent industry and employment trends as well as limited resources, the workout/restructure of the problem loan could be managed by the same individual or group that originated the loan.

How would your institution manage this additional workload while maintaining compliance with daily deadlines? With a Suspicious Activity Monitoring Services package, Abrigo assigns experienced financial crime professionals as project managers for the institution.

Accounting, consultancy and technology firm Crowe is rolling out a new solution designed for hospitals to automate daily bank reconciliation processes and manage cash flow, the company said in a recent announcement. The financial services sector is promoting innovation in the area of healthcare financial management.

During a recent Sageworks webinar , Linda Keith, CPA, covered the top questions she gets from bankers on k-1’s, pass-throughs and global cash flow analysis. She explains that you should think of this as investment activity, not active management of the business. View the webinar recording to see Keith’s answers to all 15 questions.

Manual back-end steps bog down loan approvals Financial institutions can make financial analysis, risk rating, pricing, and other steps for processing small business loans less painful. Financial analysis Manual data entry related to financial statements and tax forms is like filling a jar with tweezerspainstakingly slow.

nonprofits are also opaque, considering only a small percentage is required to file some version of Form 990, the return for organizations exempt from income tax. Therefore repayment analysis needs to be based on unrestricted funds.” Failing to hold the nonprofit to proper financial management and reporting standards.

You might also like this webinar, "How to manage a high-performing construction loan portfolio." WATCH Takeaway 1 The OCC recommends that construction lending risk be managed by specialized real estate and construction lenders who report to the credit department. Takeaway 2 Construction lending risk is unique.

There are several reasons for this, analysts say, but regardless, there is a clear need for tight cash management in the construction sector. “Because of that complexity, taxes are more complex – it’s a snowball effect. The way taxes are done in the construction industry is different than in other industries.”

Exclusive: Arrangement has allowed bank to earn billions of pounds nearly tax-free for over 12 years Barclays has avoided nearly £2bn in tax via a lucrative arrangement in Luxembourg that allowed it to pay less than 1% on profits in the tax haven for more than a decade. Continue reading.

India’s YES BANK is tapping into tax data to expand small business (SMB) lending. Reports in MENAFN on Friday (April 13) said the company plans to offer loans to micro, small and medium-sized businesses based on their Goods and Services Tax (GST) returns. Singapore, Germany and Hong Kong.

Takeaway 2 Institutions usually leverage global cash flow analysis if a borrower has complex credits. Takeaway 3 Financial institutions should implement these best practices to effectively use CFC analysis. The GCF analysis is performed during the initial loan underwriting or during an annual review. What is global cash flow?

Tax reform played a key role for several corporate successes in the first quarter of 2018. ” However, the latest analysis from the Association for Financial Professionals (AFP) suggests businesses are reluctant to let go of that cash. . Analysis found a significant increase in cash holdings among U.S.

As a loan reviewer, you need to be technically sound in order to do your job, which means you need to have a fundamental understanding of financial analysis, taxanalysis, and all of the regulatory laws that surround the credits that you’re going to be reviewing,” Cooley says. Credit Analysis Training. Watch Webinar.

However, closer analysis and lessons from history demonstrate that to counteract inflation’s free cash flow-destroying effects, revenue must grow substantially higher than the inflation rate. Sensitivity Analysis. A sensitivity analysis tests assumptions for lenders to use to assess a project’s ability to service debt.

Then there are vendor contracts, employment agreements, statements of work, loan documents, financial statements, tax returns, deposit account documents, policies, and an array of similar applications. Pulling data off a tax return has a low error rate while pulling data off an attorney-prepared loan document is more challenging.

Expense management technology is now a saturated market, particularly for the small business space – which is notoriously difficult to serve, because they are too small for large, enterprise-grade solutions, but too large for consumer-specialized tools. ” What is clear, though, is that demand for T&E technologies is on the rise.

Commercial real estate lending continues to receive regulatory scrutiny and reminders for financial institutions to practice solid risk management. Eberley, director of the FDIC's Division of Risk Management Supervision wrote in the publication.

A credit risk manager at one bank with $900 million in total assets estimated that her team received approximately 8,220 tax returns in the 2015 calendar year. The company was named “Overall Most Innovative” for its Electronic Tax Return Reader (ETRR). Enter Sageworks.

Technology may be enabling automation in small business (SMB) accounting and financial management, but rather than cutting out the need for human accountants in the field, this tech disruption is supporting a change in the profession. This means that in the SMB FinServ space, there is a significant market opportunity to target the accountant.

These expansions can come with growing pains, including identifying new customers to whom the bank can make loans, creating more rigorous and objective credit analysis policies and training bank employees on those policies. Loans across categories increased, with commercial and industrial loans growing at the fastest rate, roughly 5.3

The thing about databases is they’re siloed and they’re generally centralized, and they’re owned and managed by someone who has unilateral editorial rights. Similarly, automating more of what is put into client accounting systems (such as expense reports), can pave the way for use of more sophisticated technologies for analysis.

ERC gave eligible businesses a refundable tax credit of up to 50% of $10,000 for qualified wages paid per employee. Community banks can now white label this same product to onboard and process employee retention tax credits for the bank’s small business customers AND prospects. In 2020, the U.S.

expense management platform Sweep , professionals like gig workers, freelancers and the smallest of the SMBs are being left out of the T&E solutions market because they lack those resources. According to Billel Ridelle, founder and CEO of newly-launched U.K. Focusing On Integration. Before PSD2, U.K.

Takeaway 2 Process management features of a loan origination system help manage the workflow, from analysis through closing. A loan origination system (LOS) should perform several basic functions to automate and manage the end-to-end steps in the commercial loan process. Workflow & Analysis. Beyond Origination.

Ideally, this is a person or persons central to the creation and management of Supplier and Customer data. Users include Procurement, Accounts Payable, Sales and Marketing, Accounts Receivable, and anyone else who uses this data to conduct business or create an analysis. Tax Organization Type – Corporation, Partnership.

Boards of directors and executive management teams cannot afford to manage risks casually on a reactive basis, especially considering the rapid pace of disruptive innovation and technological developments in an ever-advancing digital world.”. Finance professionals spoke with Gartner, Inc.

Then there are vendor contracts, employment agreements, statements of work, loan documents, financial statements, tax returns, deposit account documents, policies, and an array of similar applications. Pulling data off a tax return has a low error rate while pulling data off an attorney-prepared loan document is more challenging.

India’s HDFC Bank has teamed up with Mastercard and SAP Concur to manage corporate travel and expense management, according to a report by The Economic Times. The bank will offer a corporate credit card for travelers that provides solutions for expense management and payments while users are on business trips.

One of the first steps in making sure you generate an acceptable return on your investment is to identify quickly a small number of clients with whom you can incorporate the industry data, financial analysis and projections available through ProfitCents. Instead, they sign their tax paperwork and scurry out the door.

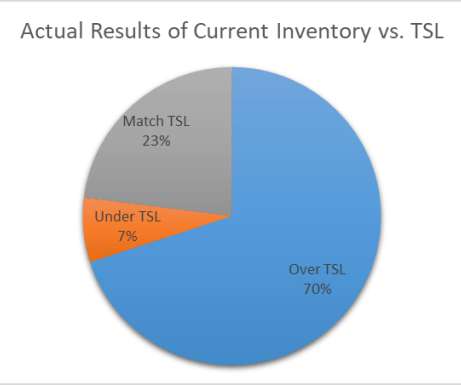

If too many spare parts are held, the prices of financing, insurance, taxes, physical handling, warehousing, etc. This trade-off is illustrated in the following chart: *Carrying cost includes the costs of financing, warehousing, physical handling, taxes, insurance, obsolescence, deterioration, and pilferage. will balloon.

Growth of FinTech funding seems unstoppable, with the latest analysis from Hampleton Partners finding enterprise financial services and integration, online financial services, enterprise financial software and Software-as-a-Service (SaaS) risk management as some of the hottest spots for investors this year. 2nd Address.

However, by performing a global analysis on applicants or considering them for different products, the institution may be able to book more loans. They would not yet have tax returns for the business, and they would likely still be showing poor cash flows. For example, consider a small business owner in their first year of business.

How to close more loans by speeding up lending and credit analysis Seeking a quicker loan origination workflow is worth it. Datos Insights recently described its analysis of more than 1,000 small and midsize businesses (SMBs) comparing how various generations behave differently when shopping for credit for an SMB.

Financial management is mission-critical to the health and vitality of small business (SMB), but it’s also one of the most difficult tasks for entrepreneurs and business owners that may have the skills to launch new products or services, but lack the accounting expertise to handle the numbers.

Accounting, audit and tax services are unlikely to be the growth engines of the accounting profession in the coming years. The weeks and months following the end of tax and audit seasons represent an excellent time for firm leaders to take stock of their accounting practices and the services clients may need.

Sageworks, a provider of credit risk and portfolio management solutions , regularly hosts complimentary webinars for banks and credit unions. During this webinar, attendees heard from Sageworks risk management consultants on how to determine if a loan is impaired and how that impacts the calculation of the ALLL.

The products featured in the report include: · Credit Analysis. Relationship Manager. Electronic Tax Return Reader (ETRR). Specifically, AAR highlights products and services spanning the full life-of-loan suite offered by Sageworks, a suite used by more than 1,100 financial institutions across the United States. Loan Pricing.

Relevant tax forms, quarterly financial statements, or bank statements are acceptable documentation. All other items, such as subcontractor costs, reimbursements for purchases a contractor makes at a customer's request, investment income, and employee-based costs such as payroll taxes, may not be excluded from gross receipts. .

Demand for valuation services is growing, according to a recent AICPA survey , with increased opportunities expected in shareholder/partner disputes, contractual disputes, family law, and gift and estate taxes, among other areas. This can free up senior analysts for the value-added analysis and review. Regulatory changes.

It is important that institutions require this data for a proper credit analysis. Beyond requiring the data, it should be entered into accessible systems, like customer relationship management solutions, tickler software or workflow applications with approval processes.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content