This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Leveraging advanced data analytics , AI, and machine learning can provide real-time insights into customer preferences, behaviors, and financial needs, creating highly individualized experiences that improve engagement and loyalty.

Digital transformation will remain a powerful force, with advancements in AI and machine learning enabling unparalleled operational efficiencies and hyper-personalized customerexperiences. In 2025, AI will play a pivotal role in customer service, fraud detection, risk management, and personalized financial advice.

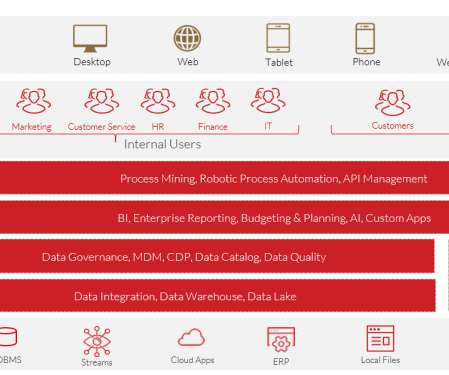

The world of modern data and analytics continues to evolve and is very exciting. They also quietly built out a robust set of services to support any and all use cases related to data and analytics. Outlined below are the Top 10 Things You Didn’t Know about Data and Analytics in the Oracle Cloud: 1.

Connected experiences, in the context of the customer relationship, are driven by a robust data set that confidently presents integrated, diverse data to enable actionable insights that can be automated across the customer’s journey.

The prevalence of online commerce opens new doors for digital fraud, however, both from career fraudsters and opportunistic customers. Developments F rom The World Of Digital Fraud. Developments F rom The World Of Digital Fraud. For more on these and other digital fraud news items, download this month’s Tracker.

Popular use cases include request for payments using the instant payment rails (above), loan payments and transaction verification to prevent fraud. Marketing and Promotions : Banks can create visually appealing and engaging promotional content, including videos and images, to capture customer attention and drive engagement.

Additionally, businesses should explore new revenue models through premium features and address integration complexities with robust data governance and analytics. AI will be pivotal in this transition, enabling automation of key compliance processes such as know your customer (KYC) and anti-money laundering (AML) checks.

Materials, training, and fraud also contribute to bank expenses. Increase Fraud Tools The largest impediment for customers using their card more often is the narrative espoused by many financial sites and advisors that the debit card is less safe than the credit card. Targeting dormancy is also a popular card marketing tactic.

Equifax has inked a deal to purchase artificial intelligence (AI)-powered fraud prevention and digital identity technology provider Kount for $640 million. As digital migration accelerates, managing authentication and online fraud while optimizing the consumer's experience has become one of our customers' top challenges,” Equifax CEO Mark W.

The economic risks of AI to the financial systems include everything from the potential for consumer and institutional fraud to algorithmic discrimination and AI-enabled cybersecurity risks.

Fraud protection specialist Kount and Philadelphia-based payments platform FreedomPay are teaming up to offer “an integrated, complete solution to enable international expansion with fraud-free payments and frictionless customer” experiences. Before, they were limited to one or two areas.

The number of real-time payments has risen dramatically in recent years, and APP fraud has grown alongside it. Bad actors typically perpetrate APP fraud in several ways. APP Fraud Ramps Up. Instances of APP fraud around the globe have continued to rise as real-time payment rails extend their reach.

It’s the battle against fraud that can be lost right at the beginning. There’s increased urgency on the part of financial institutions (FIs) to spend more time and money on battling fraud at the point of onboarding, especially as card-not-present transactions surge in the lingering wake of the coronavirus. alone topped $10.2

Consumers are using mobile apps’ order-ahead features and loyalty perks more often during the COVID-19 pandemic, yet chargeback fraud — also known as friendly fraud — is unfortunately also rising. Chargebacks were originally instituted as a last resort for customers, but they have gained popularity alongside digital commerce.

When it comes to deploying corporate resources in the battle against online fraud and account takeovers (ATOs), all too often, guiding principles fail to spot what’s really happening to a business in real time. The rule of thumb here is that after committing account takeover fraud, those fraudsters lie in wait before using the stolen account.

Banking institutions are responding by integrating advanced technologies, particularly artificial intelligence and data analytics, into their lending operations to enhance efficiency and adaptability. Personalization not only enhances the customerexperience but also strengthens the bond between banks and their clientele.

Fighting fraud is a lot harder online, and a lot harder for merchants and consumers, as card-not-present transactions become the preferred method of malfeasance. In one recent announcement, payments provider TSYS and real-time learning technology platform Featurespace said they were joining forces to offer fraud prevention tools.

Think the life of a vice president of analytics is all about the numbers? But in an interview with PYMNTS, Massy Najafi , who serves in that role at Guardian Analytics , shed light on more than a few other aspects of the job. PYMNTS: What does a day in the life of a VP at Guardian Analytics look like? Think again.

Citi announced on Monday (April 29) the launch of NextGen, its artificial intelligence-powered risk analytics scoring engine. We process nine million transactions annually, and the NextGen project will help us optimize our processes from the back office to the front by expanding the use of digitization, automation and advanced analytics.”.

Both solutions provide increased fraud protection to online transactions made via debit or credit cards. Improving customerexperiences was not the sole focus of 3DS 2.0’s The changes also include enhanced fraud protections for merchants. With the right partners in place, the risk-based nature and data analytics of 3DS 2.0

This year has been even worse on the fraud front,” we learn from the new PYMNTS Preventing Financial Crimes Playbook , done in collaboration with NICE Actimize , “as financial crime stresses FIs that are already confronting the pandemic, economic struggles and an unpredictable political climate. Real-Time, Cross-Channel Fraud Controls.

Fraud attacks’ frequency and complexity will likely continue to rise despite merchants’ best efforts to prevent them. The Latest Fraud Decisioning Developments. The United Kingdom’s RELX , an information and analytics firm, has meanwhile purchased fraud prevention firm Emailage to boost its own anti-fraud efforts.

Data holds the key to helping modern enterprises develop effective anti-fraud strategies. Many businesses are sitting on massive troves of it, but they are also facing down the three “V’s” of data complexity — velocity, variety and volume — which can make tackling fraud even harder. . Structured Versus Unstructured Data.

Digital fraud prevention company Kount is rolling out a complete solution to protect companies from criminal and friendly fraud, the firm announced in a press release on Monday (Oct. Kount’s digital fraud prevention uses artificial intelligence (AI) that mimics a fraud analyst.

It is known that negative friction is bad, ruining customerexperiences and leading to abandoned carts and all manner of dissatisfaction. Merchants in this category seem to be putting positive friction to use,” according to the March 2020 Merchant Fraud Decisioning Playbook , produced by PYMNTS and sponsored by Simility.

Radial , an omnichannel and fraud solutions provider, is promising to take away merchant woes with a suite of solutions, which it says improves order conversion rates and helps eliminate fraud. 2015, online fraud is forecast to explode from an estimated $3.1 With the introduction of EMV chip technology in Oct.

Fraud detection company DataVisor has teamed up with Experian to integrate the company’s “unsupervised machine learning powered transactional risk assessment capabilities” into the Experian CrossCore platform. The move will help detect fraud patterns, the companies said in a press release. “We DataVisor has more than 4.2

Can data make all the difference in the fight against payments fraud? The discussion played off the findings of a new whitepaper from the firm titled, “Driving Up Conversion with Effective Fraud Management.”. What works in preventing payments fraud at a large airline or telco system may not be germane for an electronics retailer.

Insurance fraud is not a new phenomenon, but it is a prevalent one. and comprise up to 10 percent of all insurance payouts, meaning legitimate customers are often forced to pay higher premiums to make up for the losses. The best prevention is really being aggressive: using AI and data to find [fraud].

The same technology that has helped change the world of payments has also fueled fraud complexity, requiring an increasingly sophisticated anti-fraud response – payments fraud has become a €20Bn ($23Bn) worldwide problem for financial institutions while the fraud detection and prevention market will be worth €28.49Bn ($33.19Bn) by 2021 [1].

ACI Worldwide advises that, as the world moves toward immediate payment ecosystems, a holistic view of the transaction, with layered controls from origination to the application of real-time rules, is the only way to push the pedal to the metal on faster payments and put the brakes on fraud. million in 2007 to £52.5

Widely publicized data breaches and hacks have made today’s consumers especially concerned about fraud. Cautious shoppers may find comfort in debit, with fraud losses associated with the payment method declining over the past several years. Card fraud is an ever-present threat. A Big-Picture Approach To Thwarting Debit Fraud.

The last few years have thrown up many challenges for banks and card providers as everything has shifted online, one of the primary challenges being fraud scams. But the online shift has also created opportunities for financial institutions to demonstrate their strong fraud controls in the digital space.

We’ve long dealt with this challenge in fraud and credit risk decisioning, but in using ML across multiple industries, there are entire sets of proposed explanatory algorithms which are either right, ineffective or flat wrong. In 2018 we will see new analytics around relationship epochs.

Simple, we will show, often leads to a better customerexperience, enhanced reliability, better profitability and clearer purpose. Customers and employees will always change faster than policies and procedures. Keeping things simple, is difficult. Keeping the status quo is always easy.

As fewer people visit branches, there is definitely an opportunity for CUs to enhance and elevate their digital banking strategies,” said Salzer, with additional payment options and tightly integrated and customizedexperiences that can rival offerings of big banks.

Positive Aspects of AI in Financial Services As noted by the OCC, advances in computing capacity, increased data availability, and improvements in analytical techniques, have significantly expanded opportunities for banks to leverage AI for risk management and operational purposes.

These tools include: Salesforce Analytics: Finance teams have access to real-time insights into customer behavior, sales performance, and marketing campaign results. Salesforce Einstein AI can be used to identify fraud and waste and to optimize financial processes. Reporting and analytics.

Until recently, use of real-time analytics and big data has been used primarily in areas such as fraud detection, using advanced algorithms to assess a transaction in fractions of a second and determine whether action is required before it is approved. A real-time insight into experience. ” Turning insight into action.

For fraud management, this means the people managing card fraud are not engaged in managing ACH payment fraud, and the person worrying about customerexperience is not the person awake at night with fraud worries. Forward-thinking banks are taking a more holistic approach to fraud management.

These platforms must ensure that all parties are trustworthy, putting them in precarious positions as they work to build their user bases without alienating either side with their anti-fraud measures. . The platform also runs customers’ background checks and processes credit cards through a predictive analytics system to gauge fraud risks.

This is the first in a series of articles in which we tackle some of the most topical fraud issues and decisions facing fraud managers today. Not only is the customerexperience diminished, but in these days of social media, the disgruntled customer may take to Twitter or Facebook to vent their frustrations.

Bankers don’t know what they don’t know, and few bankers outside of national and regional banks have experience with platform selection when it comes to digital banking platforms. Most mobile and online banking platforms allow little innovation and customization. Unfortunately, small businesses often get stuck in the middle.

Bankers don’t know what they don’t know, and few bankers outside of national and regional banks have experience with platform selection when it comes to digital banking platforms. Most mobile and online banking platforms allow little innovation and customization. Unfortunately, small businesses often get stuck in the middle.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content