This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The financial services sector is experiencing transformative changes driven by technological advancements and innovative trends. Additionally, the emergence of embedded finance and an increased focus on regulatory compliance are compelling financial institutions to continuously adapt and innovate.

Their contributions are massive, and if you’ve ever worked with AML Officers and fraud professionals, you know just how vital they are. Every day, I’m reminded of the critical role the teams at our 2,500 bank and credit union customers play in anti-money laundering (AML), combating the financing of terrorism (CFT), and fraud prevention.

In the August Digital-First Banking Tracker® , PYMNTS explores the latest in the world of digital-first banking, including how the pandemic is driving ATM innovation, how FIs are protecting both digital accounts and ATMs from potential fraudsters, and the new cybercrime-fighting techniques that are revolutionizing the digital banking industry.

Harnessing consumers’ digital information is critical to the success of any business, and data analytics and artificial intelligence (AI) can be especially powerful tools. Fast-food giant McDonald’s was not interested in using AI or data analytics until it noticed that many of its competitors were benefiting from the technologies.

Payments Trend #1: AI-Driven Payment Innovations The landscape of payments and financial services in 2025 will be marked by groundbreaking innovations and user-centric designs powered by Generative AI (GenAI). Recommended Approach : To navigate these changes, businesses must balance innovation with compliance.

For credit unions (CUs), data analytics can deliver that insight, helping them to more effectively address their members’ specific needs, and informing CUs of the products and services that can deliver the most effective returns on their investments. percent of CUs that did not focus on data analytics. For example, 91.7 Meanwhile, 80.6

This will require being more inquisitive and innovative compared to previous years, as the adoption of AI and cloud technologies continues to expand. Banks can use advanced data analytics and AI to deliver highly personalized financial services, such as customized savings plans and tailored investment advice.

Popular use cases include request for payments using the instant payment rails (above), loan payments and transaction verification to prevent fraud. Better Analytics: RCS provides detailed analytics on message delivery, read receipts, and customer interactions, enabling banks to optimize their communication strategies.

The economic risks of AI to the financial systems include everything from the potential for consumer and institutional fraud to algorithmic discrimination and AI-enabled cybersecurity risks. He argued that well-designed checkpoints could help balance the need for innovation with necessary safeguards to prevent runaway growth.

This article covers these key topics: The evolution of AI Lending: A legacy of data-driven innovation Generative AI in lending: The next frontier Abrigo's approach to AI Parallel journeys of AI, banking technology Artificial intelligence (AI) is often heralded as a revolutionary force in todays world, but its story stretches back decades.

This week's look at payment rail innovation is all about speed, both for legacy rails and new ones. Combining these elements, we are creating a broad platform with faster technology and smarter and better services that the industry can trust as a foundation for innovation towards their own end-clients," he added.

fraud prevention firm Featurespace announced on Wednesday (Feb. Noting the worldwide cost of fraud is estimated at £3.89 trillion) Featurespace said as fraud techniques evolve so must prevention solutions. With the evolution of fraud , P2P payments and eCommerce are increasingly becoming key areas of cyberattacks.

It’s no secret that, as fraudsters continue to evolve and increase the sophistication of their tactics, the fraud prevention landscape must do the same in order to stay one step ahead. With global fraud attacks on the rise , Forter is looking to transform the need for retailers to manage these rules-based systems that produce scores.

Equifax has inked a deal to purchase artificial intelligence (AI)-powered fraud prevention and digital identity technology provider Kount for $640 million. As digital migration accelerates, managing authentication and online fraud while optimizing the consumer's experience has become one of our customers' top challenges,” Equifax CEO Mark W.

However, financial institutions (FIs) are getting better at separating vital areas of innovation from the hype. Banks are increasingly focusing on the fundamentals when determining their innovation agendas. Payment technology is in many ways the flagship among the fleet of innovations that banks are pursuing.

Think the life of a vice president of analytics is all about the numbers? But in an interview with PYMNTS, Massy Najafi , who serves in that role at Guardian Analytics , shed light on more than a few other aspects of the job. PYMNTS: What does a day in the life of a VP at Guardian Analytics look like? Think again.

But how much are FIs really investing in blockchain and artificial intelligence (AI) compared to more foundational innovations? The latest Innovation Readiness Playbook looks at where FIs have been focusing over the past three years and what their plans are for the near future. Data analytics is ready for a surge in interest, however.

Anti-money laundering, data security, mobile/digital payments, fraud-fighting and payment tech rounded out the top five — with each ranking as a lead priority for over 50 percent of credit union executives. percent) of credit union executives naming it as an innovative top priority. Where Analytics Are Working.

Fighting fraud is a lot harder online, and a lot harder for merchants and consumers, as card-not-present transactions become the preferred method of malfeasance. In one recent announcement, payments provider TSYS and real-time learning technology platform Featurespace said they were joining forces to offer fraud prevention tools.

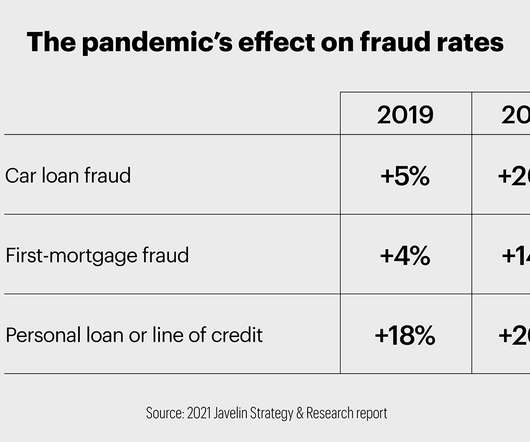

Fraud targeting digital banking users has been around as long as digital banking itself, but it has recently become more prevalent. The pandemic is exacerbating the problem, with a study finding that 22 percent of Americans were the targets of pandemic-related fraud attempts as of March. APP fraud is not a new occurrence.

Consumers are using mobile apps’ order-ahead features and loyalty perks more often during the COVID-19 pandemic, yet chargeback fraud — also known as friendly fraud — is unfortunately also rising. A Proactive Approach To Friendly Fraud. Friendly fraud often develops around online promotions at restaurants.

Citi announced on Monday (April 29) the launch of NextGen, its artificial intelligence-powered risk analytics scoring engine. We process nine million transactions annually, and the NextGen project will help us optimize our processes from the back office to the front by expanding the use of digitization, automation and advanced analytics.”.

Fraud Threats To Digital Banking. Another threat is identity fraud, in which bad actors will either steal an individual’s identity or forge a new one, and then use it to open new accounts or apply for fraudulent loans they have no intention of paying back. Identity fraud accounted for $16.9

PSCU has prevented over $277 million in would-be fraud last year, 30 percent more than in 2018. PSCU said it regularly invests in industry-leading cyberattack prevention tools – like machine learning (ML) and data analytics – across all channels. Pindrop blocks attempted contact center fraud and works to protect accounts from loss.

EXCLUSIVE—Cloud infrastructure and data analytics are becoming more and more integral to financial services, and Capital One is one bank ahead of the curve. “We We are a very data-driven company, we want to bring the bank to the customer,” Linda Apsley, vice president of data engineering at Capital One, said of the bank’s use of […].

As more customers moved online, fraudsters took advantage of new and increasingly inventive opportunities to commit remote authentication fraud. These types of scams fall under the broad term of remote authentication fraud, and they’re increasingly common—and inventive. Examples of remote authentication fraud. New account fraud.

In an interview with PYMNTS, Denise Stevens , senior vice president and chief product officer at PSCU , said contextual offers and predictive analytics will help CUs compete more effectively with larger, traditional financial institutions (FIs) — and cement member loyalty. Data Analytics.

Countering digital fraud is a lot like playing whack-a-mole: As soon as one fraudster is taken out, two more pop up where they’re least expected. The popularity of digital banking services has created ample opportunities for bad actors, leaving banks scrambling to protect themselves against the rising tide of fraud. It helps.”.

Although CU members want innovation in member loyalty and rewards, most credit unions are not delivering these programs up to the desired standards. Credit union members’ high expectations when it comes to loyalty innovation do not necessarily make or break their banking relationships. Loyalty Innovation Strategies .

IBM RegTech Innovations. These technologies bring capabilities that speed risk modeling, automate fraud detection, ensure regulatory compliance, enable distributed trust, and protect sensitive financial information. We have developed a new approach to detecting financial crimes and fraud using graph analytics and machine learning.

While many companies have enough analytics, pattern recognition and science behind their data to feel confident on their decision making, Bise said more will be needed to stay one step ahead of them. It’s clear that as payments get faster and technology advances, fraud is moving at the same speed. Safety In Numbers.

Technology and innovations advanced in leaps and bounds in 2023, including enhancements to AI, the introduction of generative AI and investment in data analytics.

These tactics cast a wide net of fraud over the fleet card industry – from issuers and acquirers to fleet managers, employers and employees themselves. The company’s latest solution, EazyFuel , offers fraud and risk management directly to all players in a fleet card transaction, in addition to payment processing and other capabilities.

So, how are CUs to approach their website and mobile innovations with different generations that hold different expectations? About the Credit Union Innovation Playbook. The Credit Union Innovation Playbook , a collaboration between PYMNTS and PSCU , delves into the innovation agendas of players in the credit union ecosystem.

The growth of Same-Day ACH seems to also suggest that previous concerns about the risk of more fraud as a result of accelerated transactions has not held the industry back from adopting the functionality. focuses on enhancing payments speed domestically, payments innovators have taken the speed of cross-border payments to task, too.

Coupon fraud is particularly dangerous for the restaurant industry, where margins are razor-thin and any profit decline could spell disaster. What Is Coupon Fraud? Fraudsters exact coupon fraud in various ways. Coupon fraud costs U.S. There is a distinct difference between extreme couponing and coupon fraud, though.

But, Vigue added, 2017 will be a year of continued innovation in the technology that can prevent, detect and mitigate a corporate cyberattack. Seventy-three percent of organizations experienced attempted and/or actual payments fraud in the past year.”. What cybersecurity threats will impact corporate buyers and suppliers in 2017?

The financial industry is responding with innovation at the individual company level, but also collectively, with financial institutions (FIs) teaming up. A recent study from the American Bankers Association found that losses from fraud attempts against bank deposit accounts totaled $25.1 Are fraud-fighters winning?

Banking institutions are responding by integrating advanced technologies, particularly artificial intelligence and data analytics, into their lending operations to enhance efficiency and adaptability. Explore and integrate alternative data sources and innovative scoring models to offer fairer assessments of creditworthiness.

.” Another major barrier to adoption is the concern of real-time payments fraud , a threat for both service providers and corporate users. “There is less time to apply traditional fraud techniques,” said Shultz. “There is less time to apply traditional fraud techniques,” said Shultz. ”

This rampant availability of users’ data makes it easier for bad actors to wreak havoc and commit fraud. She recently spoke to PYMNTS about how Scotiabank has revamped its fraud strategy in recent years. “I Scotiabank’s Three-Pronged Innovation Strategy. It is estimated that more than 4.1

A majority (55 percent) of corporate professionals identified real-time payments as their top B2B payment service priority, according to the Real-Time Payments Innovation Playbook. With innovation comes new challenges. Losses from fraud were estimated to hit $4.2 The real estate market also recently saw innovations.

A survey found that 62 percent of customers worry about fraud — such as pilfered payment details, account takeovers or fake reviews being left in their names — when interacting with QSRs. Securing payment data and other aspects of the customer experience is the keystone to driving customer demand during the pandemic and in the future.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content