This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Now that the cannabis industry is maturing and better understood, is it time for financial institutions to take on the risk of cannabis lending? Cannabis-related businesses (CRBs)spanning everything from cultivation to retailrepresent a market in need of lending services, from working capital to real estate and equipment loans.

This article covers these key topics: Debt-service coverage ratios are steady. Businesses' working capital cycles are longer. Bank and credit union leaders can use data to inform small business lending Small businesses are showing resilience. Leveraged has improved since 2019. Interest coverage ratios have stayed strong.

Would you like other articles like this in your inbox? While significantly more efficient than mailing forms to the SBA, there are some shortfalls to E-Tran, and a vendor can help Loan submission platform Leveraging E-Tran for increased SBA lending The U.S. Key Takeaways E-Tran is the SBA's loan submission platform.

Automating the key steps that often occur in the back office leads to faster decisions, stronger customer or member relationships, and more profitable lending to small businesses. This article covers these key topics: Cultivating fertile ground for small business lending Do large lenders have an advantage in small business lending?

Recent dynamics of the small business lending market A deep understanding of the small business lending landscape and potential efficiencies can help banks and credit unions grow their portfolios. You might also like this guide for smarter, faster small business lending. Record new business formation and a wider gap between U.S.

The most-read lending & credit blogs in 2023 Probability of default, CECL model validation, and stress testing were among Abrigo's top blogs on ALM, CECL, and portfolio risk this year. Takeaway 2 The top lending and credit blog posts focused on the benefits of banking technology, interest rate management, and developing risk ratings.

In 2015, news outlets ran articles about the “ gold mine ” of venture capital investments in the alternative finance sector. More recently, data released from GLI Finance — an investor focused on the small business alternative finance market — reveals the difficulties of alternative lending investment in 2019.

In this article, we break down the lessons from this long-term trend. Germain Depository Institutions Act of 1982 enabled thrifts to offer money market accounts and expand lending powers, fostering competition with banks. of C&I lending. In 1980, all foreign-controlled banks composed about 13% of commercial lending.

Ready to catch the next wave of lending growth? Commercial and industrial lending (C&I) will be the next big performance driver for banks and credit unions. You might also like this paper on how institutions can produce smarter, faster lending. C&I lending will be the next “bomb.”

In this article, we quantify commercial loan pricing trends from our Loan Command data that will hopefully help community banks price more effectively and win more profitable business. Countering this trend is more competitive lending than we have seen in 2024 that manifests in more price concessions and less than expected margin relief.

Recent stats and dynamics of the small business lending market Understanding the small business lending landscape and potential efficiencies can help banks and credit unions grow their portfolios. You might also like this guide for smarter, faster small business lending. Record new business formation and a wider gap between U.S.

Who the competition is, what the lending competition is offering, their delivery channels, and service levels can help community banks differentiate their services and enhance their competitive advantage. Community bankers need to understand their competitive landscape. The banking industry is nationwide and is becoming less branch-focused.

From leveraging PPP technology to building relationships, reasons for boosting SBA lending are numerous. . Would you like others articles like this in your inbox? Takeaway 1 SBA lending can expand your product offerings to help win deals with prospects and existing business customers or members. Why SBA Lending?

We will consider the minimal project DSCR in this article and cover the debt yield topic in future blogs. However, in today’s economy and rapid interest rate changes, the 1.20x and 75% LTV are highly misleading measures, and the reason for this is the expected increase in currently low real estate capitalization (cap) rates.

In this article, we highlight the state of the bank commercial real estate office lending sector and make an argument about why banking might be better off than most analysts think. The State of Office Lending Risk – Traffic 2024 will mark the fifth consecutive year where office demand has declined.

Last month, the National Credit Union Administration (NCUA) approved the long-awaited final rule on risk-based capital requirements for credit unions. The Federal Credit Union Act requires NCUA to update its risk-based capital standards to be comparable with the federal banking agencies,” Matz added.

In this article, we provide a five-step AI-enabled process that will help your bank with solving strategic challenges. Will capital, for instance, become more expensive or cheaper? Step 2: Structure Choosing a Problem-Solving Approach When Solving Strategic Challenges Different problems lend themselves to various forms of solutions.

In our article last week ( HERE ), we discussed how the yield curve is currently flat between the three and 20-year points. Current Risk in Term Lending. With no additional reporting, no additional accounting, and no capital or collateral costs, the bank retains the full relationship.

A recent American Banker article discussed why the local food movement is good for community banking. Develop a relationship-based lending framework. There is also good news for small business owners (SBOs), as bank-to-business lending is expected to increase in 2014. Develop a relationship-based lending framework.

There was an interesting article in The Independent last week about the big banks becoming bigger since the financial crisis hit. The article notes that the big American banks control 70% of all US assets, and that this figure has increased 40% since 2008.

Leveraging the efficiencies gained from lending software Banks and credit unions that leverage an integrated lending and credit platform reap the benefits of a consistent, efficient and defensible lending program. Would you like other articles like this in your inbox? Lending and Credit Software. Ag Lending.

This article is the second in a two-part series on top concerns and growth strategies of community banks. banks are moving back into commercial real estate (CRE) lending as the economy continues to improve. Additionally, 57 percent indicated commercial and industrial (C&I) lending as an area of opportunity for growth.

Prepare now for potential changes to FHLBs Capital rules and membership criteria are among the areas where banks could see changes in how the Federal Home Loan Bank system operates. Capital rules and membership criteria are among the areas where banks could see changes. Would you like other articles like this in your inbox?

From leveraging PPP technology to building relationships, reasons for boosting SBA lending are numerous. . Want other articles like this on SBA loan origination in your inbox? Takeaway 2 Far fewer financial institutions regularly participate in SBA (7a) lending than the more than 5,000 that joined the PPP. . Why SBA Lending?

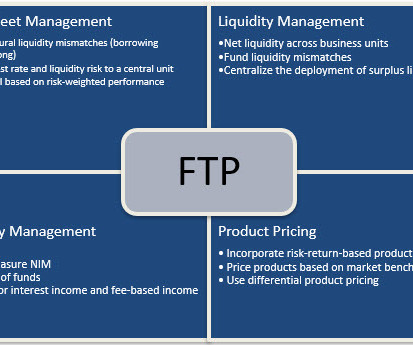

In a previous article ( HERE ), we discussed the concept of Funds Transfer Pricing (FTP), why systemically important banks and large regional banks incorporate FTP, and why community banks should also consider implementing FTP. In this article, we look at using FTP attribution to better understand lending profitability.

This article presents our six-step framework for getting started, discusses using AI for strategic planning, and looks at some of its strengths and risks. The gen AI consultant can talk intelligently about leadership, bank performance, financial structuring, marketing, lending, legal, compliance, and deposits.

5), Alenka Grealish, senior analyst at Celent, penned an article for American Banker with a prediction: The small business (SMB) credit space is headed for a “shake-up.” Between market consolidation and partnerships with traditional banks, alternative lending is certainly already an in-flux market. Alternative Lending.

Introduction A few good men and women In previous articles, we have explored the objectives of a loan review and credit risk review system in general. They should be knowledgeable of both sound lending practices and their own institution’s specific lending guidelines.

Financial institutions that want to play in the small business lending sandbox need to bring their digital toys. article , former Small Business Administration administrator Karen Mills said community banks with strong small business customer bases that don’t find new ways to serve them digitally are going to face a “reckoning.”

In our last article ( HERE ), we highlighted the methodology around why banks should calculate and drive value through customer profitability and product profitability. We focused mainly on customer profitability and used risk-adjusted return on capital as a proxy for profitability. increase in M/B.

Banking reports to inform risk management and strategy These reports on capital, growth, and liquidity help financial institutions spot warning signs. Takeaway 2 Reports that assess capital, growth, and liquidity provide banking professionals data to drive decisions. Regulators review them to assess safety and soundness.

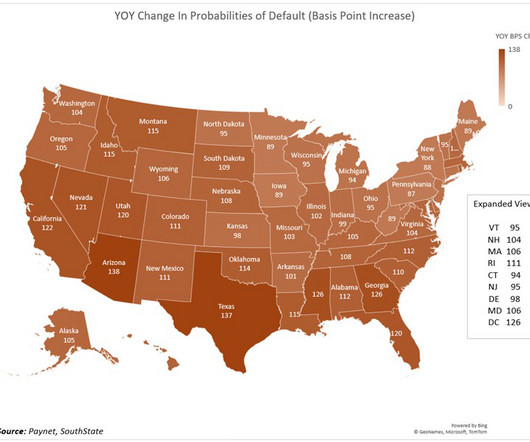

Lending is getting riskier. In this article, we look at what is happening at the state level, look at 30 common industries where credit risk is rising, and 30 industries where credit risk is the lowest. This data is critical for pricing, capital allocation, and marketing. Once again, it is time to play more defense.

The three risks are: 1) rising funding costs to erode profitability, 2) reduced capital at small banks compared to larger banks, and 3) elevated commercial real estate (CRE) credit risks. Reduced Capital for Community Banks This is the more nuanced analysis in Moody’s banking sector analysis, but one that requires understanding.

Last week, we published an article [ here ] discussing how fair value accounting for assets and liabilities may have prevented the failure of Silicon Valley Bank, even if sound risk mitigation practices were not resolutely embraced by management. At its basic premise, FTP distributes banking profit between lending and deposits.

Last week, we published an article [ here ] discussing how fair value accounting for assets and liabilities may have prevented the failure of Silicon Valley Bank, even if sound risk mitigation practices were not resolutely embraced by management. At its basic premise, FTP distributes banking profit between lending and deposits.

Last week, we published an article [ here ] discussing how fair value accounting for assets and liabilities may have prevented the failure of Silicon Valley Bank, even if sound risk mitigation practices were not resolutely embraced by management. At its basic premise, FTP distributes banking profit between lending and deposits.

Would you like others articles like this in your inbox? Nevertheless, many financial institution executives have taken – and are taking – steps that will help address their top concerns related to lending and profitability. Technology sets up future lending success. Capitalize on the momentum you gained during 2020.

Like other types of lending, banks must remain cautious to avoid too heavy of an agricultural concentration or too much lending within a certain ag segment. The challenge is that market conditions in this type of lending tend to be volatile. Without diversification, risks will be expounded.

In a survey of community banks and credit unions at the 2016 Sageworks Risk Management Summit, 42 percent of respondents said Commercial Real Estate, or CRE, lending was their primary focus for loan portfolio growth. For many, commercial real estate lending may be the ticket. This reflects a larger industry trend.

Would you like other articles like this in your inbox? Community banks are critical to ag lending and small business lending. Technology can help streamline and automate many manual lending processes, reduce compliance costs, and enhance risk management. How can community financial institutions thrive in 2021?

22) that it will buy Pennsylvania-based JetPay , “a provider of end-to-end payment processing and human capital management solutions,” according to a statement. JetPay ’s services include card acceptance, processing, payroll, payroll tax filing, human capital management services and other financial transactions.

In this article, we give a practical example of how scalability in banking works and how to use it to your strategic advantage. Case Study: SBA Lending – The Traditional Approach Small Business Administration (SBA) loan production is the perfect example of a business line that screams for digitization.

Even though many loans were booked at below-par value (more information HERE), increasing margins helped drive significant revenue resulting in one of the best years for an initial risk-adjusted return on capital. In this article, we provide a loan pricing update and highlight some critical areas where banks can improve.

In this article, we look at what is happening at the state level, at 30 common industries where credit risk is rising, and at 30 industries where credit risk is the lowest. This data is critical for pricing, capital allocation, and marketing. Getting more granular in credit risk means a more efficient allocation of capital.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content