This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Their flexibility, low premia and underlying leverage appeal to all market participants ranging from conservative investors hedging against intraday market volatility to aggressive traders speculating for quick profit generation. The improved market conditions have encouraged both market participation and innovation.

In this article, we look at those 150 safest banks to learn five connected lessons on how to create a bank that can withstand the next great economic downturn. Every bank in our 150 safest bank list is a capital generating machine because of earnings. This should be every board and bank CEOs main job.

This article covers these key topics: Debt-service coverage ratios are steady. Businesses' working capital cycles are longer. Longer working capital cycles drive line utilization Businesses are holding inventory longer (81 days in 2023 vs. 72 in 2019) and extending receivables (31 to 41 days). Leveraged has improved since 2019.

In this article, we quantify commercial loan pricing trends from our Loan Command data that will hopefully help community banks price more effectively and win more profitable business. Why many banks assumed four rate cuts at the end of 2024 and start of 2025, the market, and hence most banks) are now assuming zero to two.

the As interest rates go back up and volatility continues to remain high, banks’ cost of capital has undergone a significant shift up. Your cost of capital is essential to know for several reasons. Produce over your cost, and you will be able to attract more capital. Why Calculate Your Cost of Capital?

CRE UNDERWRITING Recent data, just released from Real Capital Analytics, shows that since the start of the year (month-end April), commercial real estate (CRE) has appreciated 2.6% In major markets, this appreciation has been closer to 4.9%, and in secondary markets, price appreciation has been 1.5%.

In this article, we break down the lessons from this long-term trend. Germain Depository Institutions Act of 1982 enabled thrifts to offer money market accounts and expand lending powers, fostering competition with banks. and money market mutual funds were 13% or greater. In 1985, there were 14,417 FDIC banking charters.

This article covers these key topics: What is a core deposit intangible? One way to easily envision this, according to Abrigo Advisory Services Manager Manuel Aya, is to think of it as the value that arises from retaining depositors, and hence deposits, at an institution versus needing to go into the open market to fund activities.

The COVID-19 pandemic has challenged the economic and labor markets, impacting all businesses regardless of their size. If your organization is looking to capitalize on cloud technology in 2021, here are a few trends to keep in mind. The Public Cloud Market Will Surge. Cloud-Native Technology Will Power Digital Transformations.

There have been many a banker who has said they want to offer a high-yield account because the “higher interest expense is just like paying marketing costs.” In this article, we explore the tactic of a high-yield deposit account. The logic that “rate sells itself” is true. However, is this the best move?

The Recession and its subsequent rate of bank failures underscore the need for banks of all sizes to invest in developing a capital plan. The Recession taught many institutions that whatever processes had been in place for managing capital were not sufficient. The result was insufficient capital. Forward-looking review 4.

Last week, the American Banking Association (ABA) held its annual Bank Marketing Conference in Denver, receiving rave reviews. The theme was – developing your marketing superpowers. Amid the brewery networking, superhero costumes, and fun, some fantastic bank marketing lessons were had, and not just for bank marketers.

The AOCI is an accounting adjustment meant to reflect the economic value of assets and is the process of “marking loans to market.” In this article, we explore what signals marking your loans to market might send. However, the public markets were another story. Capital got scarce. Loan AOCI Adjustment.

People have been talking about content marketing for years. The effects of good content marketing can be long-lasting, offering ongoing engagement while other tactics capitalize on shorter-term opportunities. Content marketing is a marathon, not a sprint. Understanding the market and competition is a good place to start.

Emotions drive markets in the short term, so no matter how good your information is, trying to guess where the market will be in a year is just that – a guess. Therefore, our capitalmarket assumptions are based on expectations for average returns over the next 10 years. annualized over the next 10 years.

N26 “has been in contact with potential advisers for the fundraising, though discussions are at an early stage and no final decisions have been made, the people said, asking not to be identified because the deliberations are private," Bloomberg's article states. "A Venture capital investment in Europe’s FinTech industry has surpassed $35.4

In this article, we provide a five-step AI-enabled process that will help your bank with solving strategic challenges. Will capital, for instance, become more expensive or cheaper? The data is analyzed on the test market, and a path is decided on. At this point, attempting to test a solution is most helpful.

Cannabis-related businesses (CRBs)spanning everything from cultivation to retailrepresent a market in need of lending services, from working capital to real estate and equipment loans. Get details The opportunities: Why cannabis lending may make good business sense The legalized cannabis market grew $2.6

The front office is screaming down to the Settlement Office, “Operations, we need more capital!” Any operations team that has dealt with a stock loan trading desk can contest the inherent friction between providing more available securities to the desk and reliance on settlement cycles and market constraints.

In the olden days, if you wanted to market deposits, the head of Retail would come to Marketing and say something like – “We need to raise deposits.” ” Marketing would then put together some ideas for a print or digital campaign; Retail would sign off on it, and then they would roll it out.

For small- and medium-sized businesses (SMBs) in need of capital, bank loans are undoubtedly the first place they look. The bond market, on the other hand, isn’t the most likely of places for an entrepreneur to seek financing. Several years ago, however, SMBs began to show interest in the bond market, too.

In this article, we highlight the state of the bank commercial real estate office lending sector and make an argument about why banking might be better off than most analysts think. Because of strong corporate earnings and substantial employment, the office market is getting a reprieve from a full-fledged downturn.

If you want to grab a material amount of new deposit balance, offer a 5.05% money market rate, post it all over Instagram, and sit back and watch the money roll in. In this article, we will show you 15 proven deposit marketing campaigns that will rack up deposit-gathering wins while building a high-performing bank in the process.

This change in approach introduces new variables in the interest rate projections that for decades have been a non-issue as we were effectively in a 0% interest rate market. Markets move in unpredictable ways when least expected. This happens when market expectations are for a reduction in inflation or a flight to safety.

Square now manages $100 billion in annual payments and has an $83 billion marketcapitalization, the article said. Before Square, launched by Twitter co-founder Jack Dorsey in 2009, SMBs had a hard time maneuvering point-of-sale (POS) card transactions.

There was an interesting article in The Independent last week about the big banks becoming bigger since the financial crisis hit. The article notes that the big American banks control 70% of all US assets, and that this figure has increased 40% since 2008.

award-winning Here’s Why digital marketing video series, Eric Enge talks about GPT-3, one of the latest developments in the Artificial Intelligence space. I’m the Principal for the Digital Marketing Solutions Business Unit at Perficient. And combined with other investors, they put in a billion dollars of seed capital.

620 million has been financed to date, with Sequoia Capital, Amazon, and T. Companies also need the California DMV’s approval mentioned earlier in this article. Other companies continue to arrive in the expanding self-driving vehicle market. Rowe Price Associates contributing.

With the current flat or slightly inverted yield curve, plus the current volatility of the market, borrowers have a pricing advantage to lock in long-term, fixed-rate loans, leaving lenders with the interest rate risk without appropriate compensation. Without this minimum staff, we believe that is difficult to create a viable B2B program.

This article presents our six-step framework for getting started, discusses using AI for strategic planning, and looks at some of its strengths and risks. The gen AI consultant can talk intelligently about leadership, bank performance, financial structuring, marketing, lending, legal, compliance, and deposits.

In this article, we look at several basic capitalmarket precepts that the average investment officer lives with every day but lenders may not notice. . With a low and flat yield curve, generating profits through investments has become more challenging.

In 2015, news outlets ran articles about the “ gold mine ” of venture capital investments in the alternative finance sector. Yet at a time when analysts say VCs are focusing more on late-stage investment , alternative lenders are having a tougher time securing funding, particularly market newcomers in a crowded market.

In a recent article ( here ), we discussed why banks that take risks to earn higher revenue demonstrate lower performance as measured by ROA. While in that blog, we specifically considered the risk-return tradeoff for credit risk; in a future article, we’ll consider interest rate risk. However, success does not occur by happenchance.

In our last article ( HERE ), we highlighted the methodology around why banks should calculate and drive value through customer profitability and product profitability. We focused mainly on customer profitability and used risk-adjusted return on capital as a proxy for profitability. The answer is – most likely.

In only one example noted in this space, as reported this week , tech startup Social Finance (SoFi) is closing a merger deal with blank-check firm Social Capital Hedosophia Holdings Corp. We note that can stoke enthusiasm, and capital commitments (i.e., V to file an IPO. As to where SPACs go from here is anyone’s guess.

In an article last week ( Here ), we discussed how the higher-for-longer interest rate environment will affect the community bank sector. Profitability Reality at Community Banks In a recent article ( Here ), we used CAPM (capital asset pricing model) to calculate community banks’ cost of capital – which we conclude is now 12.50%.

Prepare now for potential changes to FHLBs Capital rules and membership criteria are among the areas where banks could see changes in how the Federal Home Loan Bank system operates. Capital rules and membership criteria are among the areas where banks could see changes. Would you like other articles like this in your inbox?

Based on the futures market, the Federal Reserve is expected to raise the Fed Funds rate to 3.00% at its December 2022 meeting. In this article, we analyze the industry’s cost of funding earning assets (COF) and track how community banks’ COF behaves relative to larger banks. Historical Cost of Funds Analysis.

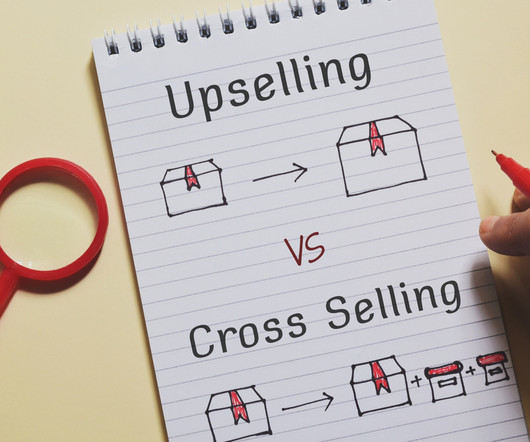

In two previous articles ( here and here ) we discussed how loan size and loan term affect the profitability of commercial loans. In this article, we consider the common features of upselling and cross-selling. In this article, we consider the common features of upselling and cross-selling.

Cryptocurrency markets plummeted after oil prices crashed and the stock market spiraled into another sell-off frenzy, according to reports on Monday (March 10). . warned prices could drop to near $20 a barrel,” the CNBC article said. As the global oil benchmark plummeted to as low as $31.02 a barrel, Goldman Sachs Group Inc.

A slew of articles have been published explaining the reason for this bank’s failure. Not The Root Causes We think that the most disingenuous cause of the bank’s failure as cited in various articles is the “uncertain environment.” However, that faster growth was not unusual and reflects the bank’s higher growth markets.

In two recent articles, we reviewed the banking industry’s deposit behavior with regard to cost of funding earning assets (COF) ( HERE ), and we compared how community banks’ COF behaves relative to national banks in a rising interest rate cycle ( HERE ).

According to CoinDesk, “The broader cryptocurrency market accompanied BTC in its steep sell-off and has shed more than $15 billion in total marketcapitalization in the last 24 hours.”. But it will also have ripple effects that will hit downstream, perhaps in some unexpected places, according to a PYMNTS article.

It was led by “Energize Ventures and Lux Capital, each of whom invests heavily in companies, fundamentally advancing how society implements and utilizes advances in technology,” Zededa said in a statement. percent by 2024. Security Upgrades?

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content