This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This article covers these key topics: Debt-service coverage ratios are steady. Businesses' working capital cycles are longer. Thousands of banks, credit unions, and accounting firms use our riskmanagement and lending solutions, contributing to this cooperative data model for banking intelligence. Nearly all U.S.

Meet Model RiskManagement Expectations Updates to the FDIC RiskManagement Manual should steer institutions toward a model that managesrisk and drives growth. Would you like other articles like this in your inbox? Model RiskManagement in the spotlight. FDIC Update.

Best practices for assessing models and managingrisk Sound model development, implementation, use, and validation is especially important as CECL models debut. . Would you like other articles like this in your inbox? What are model riskmanagement and model validation? Model governance overview. Federal guidance.

While we will cover the general lessons HERE , in this article, we wanted to focus on the root cause – how and why interest rate risk caused the second-largest bank failure in US history (Washington Mutual was the largest in 2008). That combination made their liabilities very sensitive to safety.

The lender needs to put forth an accurate and complete picture of the borrowernot only for the borrowers sake, but also for the financial institutions riskmanagement. Focus on relevant repayment and credit risk information Whats relevant in a credit memo? But they shouldnt be an exercise in verbosity or regulatory appeasement.

This article covers these key topics: Cultivating fertile ground for small business lending Do large lenders have an advantage in small business lending? But these businessesoften the backbone of their communitiesdepend on access to capital. They often must consult paper files as well as information housed in separate digital systems.

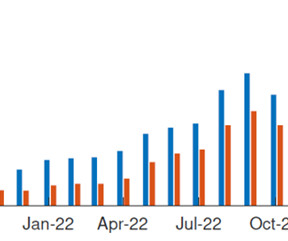

Figure 1: Total S&P 500 options trading volume by Time to Expiry (2016 to August 2023) Source: CBOE article: The Evolution of Same Day Options Trading , 3 August 2023. Potential deficiencies in the current margining system, and the inability of riskmanagement infrastructure to keep pace with new market developments.

This article covers these key topics: What is a core deposit intangible? As a result, lower CDI values may lessen the financial burden for acquirers, improving their capital efficiency. Why are core deposit intangibles important? Read on to learn about the importance of this metric, especially in today's dynamic environment.

Takeaway 2 The top lending and credit blog posts focused on the benefits of banking technology, interest rate management, and developing risk ratings. Takeaway 3 Articles specific to small community banks were among the most-read blogs, with best practices for construction lending at the top of the list.

Takeaway 3 Updates on interest rate forecasting and best practices for managing CRE risk were among the most-read blogs. Abrigo's most popular riskmanagement blogs over the last 12 months cover topics that continue to catch the attention of professionals and regulators. Which credit areas need routine "maintenance"?

Prepare now for potential changes to FHLBs Capital rules and membership criteria are among the areas where banks could see changes in how the Federal Home Loan Bank system operates. You might also like these popular resources on interest rate risk, liquidity, and CECL. Would you like other articles like this in your inbox?

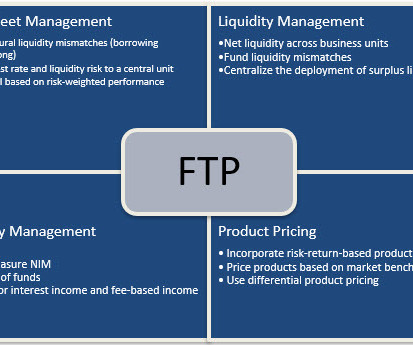

Banking reports to inform riskmanagement and strategy These reports on capital, growth, and liquidity help financial institutions spot warning signs. They help manage and shape strategy in volatile economic and industry conditions. the Community Bank Leverage Ratio (CBLR) and the minimum Tier 1 leverage ratio).

A slew of articles have been published explaining the reason for this bank’s failure. Not The Root Causes We think that the most disingenuous cause of the bank’s failure as cited in various articles is the “uncertain environment.” This first bank failure in 2024 is reported to cost the Deposit Insurance Fund $667mm.

This article outlines a structured approach to ensuring management can confidently answer inquiries about the health of their CRE segments and related credit performance. The health of CRE loans and related credit risk is a focus not only of investors, board members, and other stakeholders but also of upcoming regulatory exams.

Measuring Interest Rate Risk Can Vary by Institution Interest rate risk measurement plays a key role in ensuring an institution's safety and soundness. Would you like other articles on asset/liability management in your inbox? FDIC) noted in its 2021 Risk Review. Measure long-term interest rate risk.

Directors overseeing a bank’s operations are important partners in supervisory efforts, the FDIC noted in the article (“A Community Bank Director’s Guide to Corporate Governance: 21st Century Reflections on the FDIC Pocket Guide for Directors.”). Riskmanagement culture What exactly is a riskmanagement culture?

Takeaway 3 To fully capitalize on the forthcoming C&I wave, institutions need the right products, systems, people, and technology. Want more articles like this? Credit risk : In C&I lending, at least part of the collateral is intangible. C&I lending will be the next “bomb.”

Blog posts to help your asset/liability management (ALM) staff strategize for the future These ALM posts were the most popular in 2022. Would you like other articles like this in your inbox? Th e article is intended for the ALM rookie who wants to understand ALM basics: the process and its usefulness.

Unfortunately, the recent economic crisis highlighted shortcomings in boards’ understanding of risks and the proper oversight of those risks. A recent Wall Street Journal article by Victoria McGrane and Jon Hilsenrath highlighted how the nation’s regulators are increasingly questioning and turning their focus toward bank boards.

In a survey of community banks and credit unions at the 2016 Sageworks RiskManagement Summit, 42 percent of respondents said Commercial Real Estate, or CRE, lending was their primary focus for loan portfolio growth. Learn more about the Sageworks Credit RiskManagement Solution. This reflects a larger industry trend.

As a result, borrowers are encouraged, in the OCC document, to implement riskmanagement practices that reduce their exposure to these risks, including diversification strategies, operations integration, hedging, contracting strategies and/or purchasing insurance.

Consequently, interagency guidance on CRE concentration riskmanagement , released in 2006, helps institutions pursue CRE lending with safety and soundness. A recent article on Banking Exchange by Daniel Rothstein highlighted the continued need for community banks to diversify their portfolios and steps for execution of this task.

In two previous articles ( here and here ) we discussed how loan size and loan term affect the profitability of commercial loans. In this article, we consider the common features of upselling and cross-selling. In this article, we consider the common features of upselling and cross-selling.

Banking has a similar physics problem when management juggles strategy, risk/profitability, and customer behavior. This article will discuss the challenge of managing three potentially opposing forces and look towards physics to help us solve the mystery. Cost cutting at banks often increases risk in unseen ways.

Risks ALM Addresses Will Affect Performance and Strategy Asset/liability management models and processes address credit risk, liquidity risk, and interest rate risk. . Would you like other articles on ALM in your inbox? Which risks does ALM address? Liquidity riskmanagement and ALM.

Cheryl Monk, a writer in New York, reviews the de novo environment in her article published in the July 2017 issue of Independent Banker. Heightened capital requirements that must be met up front 3. Learn more about how Sageworks can help banks and credit unions grow profitably and mitigate risk. It is time intensive.

Therefore, our capital market assumptions are based on expectations for average returns over the next 10 years. Our riskmanagement strategies provided the cushions we had expected during the market’s decline in 2020, with returns independent of the returns from both stocks and bonds. annualized over the next 10 years.

Key Takeaways Riskmanagement practices were on the minds of bankers in 2019 Some of the most popular blog posts of 2019 were about stress testing and CECL. Riskmanagement practices were in the spotlight in 2019. CECL and stress testing.

In a recent Forbes article, Frank Sorrentino, Chairman and CEO of ConnectOne Bank, offered his take on how financial institutions should flip their mindset on regulators and examinations. From a governing body’s standpoint, stress testing builds confidence in a bank’s overall riskmanagement strategy.

The most senior riskmanagement executives at these institutions are under the spotlight, both in the industry and in the media. So when late last month Bank of America announced a management overhaul that directly impacted this important review, it left some in finance scratching their heads.

Financial institution leaders and management should consider ALM as a process for making institutions more profitable and more effective at managingrisk simultaneously. This initial ALM 101 article is intended for the ALM rookie who wants to understand ALM basics: the process and its usefulness. keep me informed.

Introduction A few good men and women In previous articles, we have explored the objectives of a loan review and credit risk review system in general. Loan review management needs to develop a basic loan review curriculum so that their senior loan reviewers are being given recruits acquainted with the basics.

This article looks at trends in growth and composition as well as legal, regulatory, and competitive pressure on noninterest earnings. million customers over "deceptive" overdraft enrollment practices between 2014 and 2018, Banking Dive noted in a recent article about growth in overdraft fees. Portfolio Risk & CECL.

This article outlines some of the math behind small business lending and its profitability and suggests ways for banks and credit unions to better serve this important market while earning appropriate returns. Almost half sought credit to grow their businesses, and 28% applied to make repairs or replace capital assets.

Independent Loan Review Systems in Banking Banking regulators have outlined expectations for effective, independent loan review and credit risk review. . Would you like other articles on loan review in your inbox? Takeaway 1 A system for ongoing, independent credit risk review will not look the same from institution to institution.

27), treasury management firm Kyriba recently announced new funding, an infusion which has come in the form of growth equity. According to news reports by Xconomy, Sumeru Equity Partners led the $45 million growth equity round, Kyriba said, while previous backers at Bpifrance, Iris Capital, Daher Capital and HSBC also participated.

In this article, we would like to define loan pricing discipline and cover bid, why it matters, and demonstrate how most community banks currently are not using loan pricing discipline. There are three ways that managers can price their loans (or any product or service, for that matter): Price to the competition. Cost-plus pricing.

Would you like other articles on fraud and AML/CFT compliance in your inbox? However, banks and credit unions should stay vigilant about choosing the right regtech solutions to tackle the challenges and capitalize on the opportunities it presents.

Would you like other articles on fraud and AML/CFT compliance in your inbox? However, banks and credit unions should stay vigilant about choosing the right regtech solutions to tackle the challenges and capitalize on the opportunities it presents.

Last week, we published an article [ here ] discussing how fair value accounting for assets and liabilities may have prevented the failure of Silicon Valley Bank, even if sound risk mitigation practices were not resolutely embraced by management.

Last week, we published an article [ here ] discussing how fair value accounting for assets and liabilities may have prevented the failure of Silicon Valley Bank, even if sound risk mitigation practices were not resolutely embraced by management.

Last week, we published an article [ here ] discussing how fair value accounting for assets and liabilities may have prevented the failure of Silicon Valley Bank, even if sound risk mitigation practices were not resolutely embraced by management.

Want other articles like this on SBA loan origination in your inbox? During Abrigo’s recent ThinkBIG Conference, credit underwriting and loan portfolio riskmanagement trainer and consultant Michael Wear , CRC , of 39 Acres Corp. Export Working Capital loans are up to $5 million and are for terms of up to 12 months.

Would you like others articles like this in your inbox? During Abrigo’s recent ThinkBIG Conference, credit underwriting and loan portfolio riskmanagement trainer and consultant Michael Wear , CRC , of 39 Acres Corp. Export Working Capital loans are up to $5 million and are for terms of up to 12 months.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content