This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Here’s a scenario. You walk into the office one morning and before you can even get a cup of coffee, you’re alerted that the firm’s website is down. It’s a distributed denial-of-service (DDoS) attack and hackers are preventing your customers from accessing the firm’s website until your financial institution pays up.

Banks are worried about access to their systems, but perhaps need to do more. Benjamin Lawsky, head of the New York Department of Financial Services, said: “A bank’s cybersecurity is often only as good as the cybersecurity of its vendors.

The risks that come with not having an application strategy could also spell trouble as cybersecurity concerns rise. In an age where their most valuable assets are under attack, banks must adopt a vigilant stance in protecting them. The C-suite should regard IT as a strategic business partner, but it simply is not there yet.

In a new twist on an old scam, cybercriminals have tried to get thousands of people to surrender their Wells bank account information by sending authentic-looking emails containing malicious links that lead to a fake website bearing the company's name.

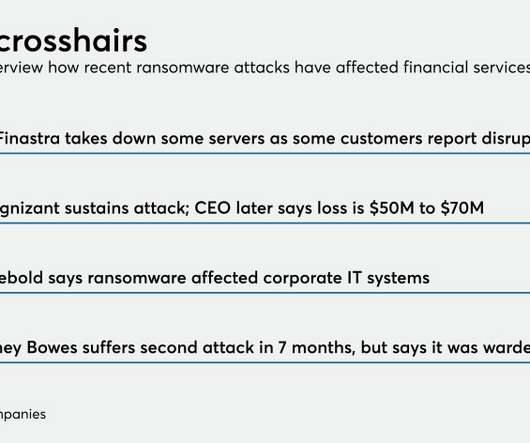

Here’s how banks can guard against that. Cybercriminals have targeted at least four financial services technology companies in recent months, potentially giving hackers back-door access to clients.

Failing to tackle fraud has important implications for customer satisfaction and loyalty – with cybersecurity breaches happening frequently, consumers are very aware of the threats posed by criminals. Customers expect their banks to fight fraud and will leave if they don’t feel safe. Customer loyalty.

Mobile banking use has swelled since the pandemic hit, and law enforcement officials expect hackers to target the credentials of digital novices. The FBI stressed the importance of two-factor authentication and ensuring consumers know how to spot fake apps that carry malware.

In a new twist on an old scam, cybercriminals have tried to get thousands of Wells staffers to surrender their own account information by sending authentic-looking emails containing malicious links that lead to a fake website bearing the company's name.

Peoples Bank in Arkansas and Main Street Bank in Massachusetts are getting smarter about spotting suspicious transactions tied to unemployment benefit fraud as well as warning customers what to watch out for.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content