This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

During 2020, our society has been faced with an economic crisis, health crisis, social justice crisis and environmental crisis. The pandemic has rapidly changed how banks engage with customers and employees; accelerating the shift from in-person interactions to digital engagements.

As readers, you indicated your interest in this year’s top trends on the site including financial regulations on marijuana , banking profitability , online-only banks and the mobile banking revolution.

The events of 2020 have only served to accelerate a number of potentially disruptive trends among consumers when it comes to banking and financial services — What does the emerging future of consumer and retail banking now look like?

Online & Mobile Banking. Since there are no physical branches, digitalbanking tools are crucial to helping customers access and manage their CIT Bank accounts. And, they should be more than enough to handle the majority of everyday banking transactions. Can CIT Bank Replace Your Bank?

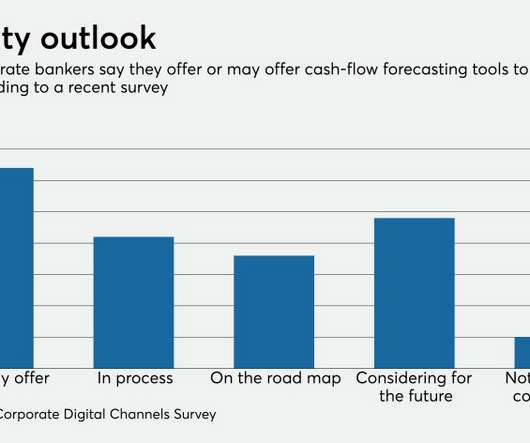

The global bank has rolled out cash-flow forecasting tools as financial institutions race to meet urgent demands from commercial customers trying to navigate uncertain times.

During 2020, our society has been faced with an economic crisis, health crisis, social justice crisis and environmental crisis. The pandemic has rapidly changed how banks engage with customers and employees; accelerating the shift from in-person interactions to digital engagements.

Daylight's initial product lineup includes a prepaid debit card with the customer’s chosen name and educational content around issues unique to LGBT households.

Shawn Rose, chief digital officer, and Holly Pontisso, vice president of customer experience at Scotiabank at Toronto, share how they have adapted their digital offerings for people over 50, including making sure ageist attitudes don’t creep into digital channels or messaging.

Financial institutions that are not ready to fully serve customers digitally face an existential threat. By self-education, we’re not talking about an email reminding customers that the bank is accessible by phone or drive-thru and that digitalbanking is open. Who prints the card?

Mobile banking use has swelled since the pandemic hit, and law enforcement officials expect hackers to target the credentials of digital novices. The FBI stressed the importance of two-factor authentication and ensuring consumers know how to spot fake apps that carry malware.

Digitalbanks are no longer in the ‘money’ business but rather, in the ‘value’ business. Unlike in the past, when more than two products from one bank made a customer loyal, customer behavior is fleeting and their expectations for digitalbanking is increasing every day, because technology is giving them numerous choices and control.

Reality checks for community banks switching to a digital model: There is a lot of talk about digitalbanking however, not all digitalbanking falls under the same umbrella. Community banks must examine what cultural, operational and marketing shifts will happen when they adopt digitalbanking initiatives.

Designing a digitalbank: What are millennials looking for in their financial institution? Spotlight banking biometrics digitalbanking financial institutions internet millennials payments security smartphone wearables' They want transparency, financial advice and fully customizable convenience.

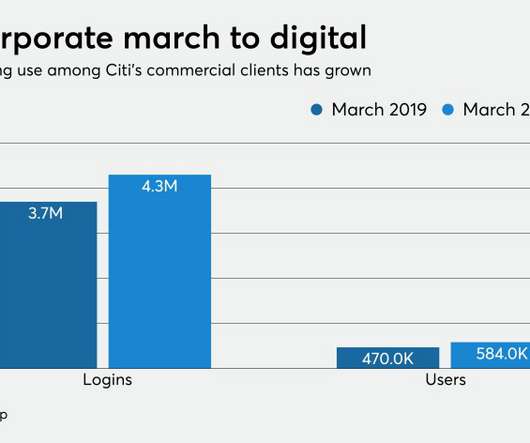

The quarantine and Citi's shift from hardware to software tokens have led to a 300% spike in commercial clients' opening of accounts online as well as increased digitalbanking use.

The digitalbank is on a larger mission to attract younger customers. It's inserting itself into the popular video game in the hope that game players will learn about its products and have fun at the same time.

Harit Talwar, who is moving from CEO of the digitalbanking unit to chairman of consumer banking, says Marcus wants to add checking and investment products, embed its offerings in additional high-profile platforms, and grow far beyond its current 5 million customers.

adults saying they use a BlackBerry as their primary smartphone, it is hard for banks to justify investment in creating and maintaining apps for these devices. What really is “digitalbanking”?: Digitalbanking is widely used in the financial services industry, but experts struggle to define what it really means.

Television executive Ryan Glover, rap star Killer Mike and civil rights icon Andrew Young have launched a digitalbank for Black and Hispanic consumers called Greenwood Financial.

Financial institutions are making fintech partnerships a key priority in 2020, according to a new study from Cornerstone Advisors. In What’s Going On In Banking2020: Outlook for a New Decade , 65% of banks and 76% of credit unions say these partnerships will be an important part of their business strategies this year.

Banks today are under pressure to perform — to generate revenue, to grow and to ensure regulatory compliance. Increasingly, customers do their banking either online or via mobile app, so it’s up to banks to provide users with a digital experience that meets their needs. Central to all of this is the customer.

Articles via Mobile Commerce Daily, Wall Street Journal, The Financial Brand, Banking Exchange. Marketers must understand mobile banking consumers’ lucrative potential: More than 90% of banking households in the U.S. use digital channels to access their banks.

*José Resendiz originally spoke on this topic during an NCR Corporation TEDx Talk in April 2015. A blog like this may not seem like the forum to talk about undertaking an Olympic triathlon, but it actually makes perfect sense. It didn’t just make me better at my job, it taught me to approach my work in an entirely different way.

Eyeprint ID is already in market for consumers among 20 banks in Australia that are leveraging the digitalbanking platform provided by The System Works Group. Many banks are adopting EyeVerify to protect their internal employees phones using solutions from Good Technology and AirWatch. Source: WSJ.

The mobile banking and paperless habits bank customers picked up during the pandemic are here to stay, and financial institutions are working to strengthen their digital offerings, speakers at an American Banker conference said.

The events of 2020 have only served to accelerate a number of potentially disruptive trends among consumers when it comes to banking and financial services — What does the emerging future of consumer and retail banking now look like?

Visionary FinTech Leaders Talk About The New Banking Customer Experience Model – Forbes. Top 5 DigitalBanking Myths – The Financial Brand. In Liberia, Mobile Banking to Help Ebola-affected Women Traders – Huffington Post. ?Snapchat Below are interesting stories the Banking.com staff has been reading over the past week.

Building a DigitalBank is a Matter of Survival – The Financial Brand. Mobile’s Rise Poses a Riddle for Banks – WSJ. Mobile Banking Leaves Something to Be Desired, Consumers Say – eWeek. Below are interesting stories the Banking.com staff has been reading over the past week.

Bank of America ranked as “Best in Class” over 20 top U.S. Bank of America ranked as “Best in Class” over 20 top U.S. FIs must find the sweet spot at the junction of consumer privacy, cybersecurity empowerment, and cybersecurity education to maintain long-lastin. The report me.

Westpac adds fingerprint access to mobile banking app – CNET. Mobile Banking Precautions: How To Avoid Cyberattacks – Investor’s Business Daily. Despite DigitalBanking Growth, Traditional Channels Survive – The Financial Brand. ?Go Go Digital, But Don’t Forget Banking’s Human Factor – American Banker.

Britain just got a new digitalbank and it’s raising tens of millions of pounds: Globally, neobanks (online-only banks) are gaining popularity. These digitalbanks target younger audiences and financial institutions should be watching what they do, and how consumers react to them, in order to readjust priorities.

Thanks to their close relationship with the card networks, banks stand to benefit most from deals like Mastercard’s agreement to buy Finicity and Visa’s pending purchase of Plaid. The prospects for fintechs and consumers are dicier.

Big Banks Still Say ‘No’ to Cloud – American Banker. Banks Need to Examine Resource Allocation – Bank Systems & Technology. DigitalBanking at JP Morgan Chase – Finextra. How Banks Are Trying to Become More Like Tech Companies – MSN Money.

Survey confirms Americans’ increasing use of mobile banking: A study from Carlisle & Gallagher found that 55% of Americans access their financial account information through mobile banking options 2-3 times per week. Spotlight bankingdigitalbanking innovation mobile banking mobile check deposit omnichannel'

Silver surfers in Britain topping mobile and online banking growth charts: Recent data shows that it’s no longer just younger generations using mobile and online banking –their parents and grandparents are starting to jump on the trend too. What have you been reading? Let us know in the comments section below or Tweet @bankingdotcom.

Value of human touch: While technological developments such as digitalbanking bring conveniences to the lives of consumers, we often forget to realize the value of human contact. In banking, tellers are often the first point of contact for members and customers and they help to enhance their experiences.

Business models and adaptability will determine the success — or failure — of financial technology companies as they deal with fallout from the coronavirus outbreak.

Comfort Zones: Acclimating Consumers to Mobile Banking– Nielson. 10 Big Ideas to Improve Your Bank in 2015 – American Banker. ? DigitalBanking through customer centric BPM – Finextra. Spotlight banking big ideas mobile app omnichannel' Macy’s makes omnichannel play with sweeping reorganization– eWeek.

Visionary FinTech Leaders Talk About The New Banking Customer Experience Model – Forbes. Top 5 DigitalBanking Myths – The Financial Brand. In Liberia, Mobile Banking to Help Ebola-affected Women Traders – Huffington Post. ?Snapchat Below are interesting stories the Banking.com staff has been reading over the past week.

Westpac adds fingerprint access to mobile banking app – CNET. Mobile Banking Precautions: How To Avoid Cyberattacks – Investor’s Business Daily. Despite DigitalBanking Growth, Traditional Channels Survive – The Financial Brand. ?Go Go Digital, But Don’t Forget Banking’s Human Factor – American Banker.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content