This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The pandemic has rapidly changed how banks engage with customers and employees; accelerating the shift from in-person interactions to digital engagements. Successfully leading a digital transformation requires much more than smart technology choices, culture is key.

The pandemic has rapidly changed how banks engage with customers and employees; accelerating the shift from in-person interactions to digital engagements. Successfully leading a digital transformation requires much more than smart technology choices, culture is key.

Building a DigitalBank is a Matter of Survival – The Financial Brand. Mobile’s Rise Poses a Riddle for Banks – WSJ. Mobile Banking Leaves Something to Be Desired, Consumers Say – eWeek. Digitaltechnology to open up core banking market – ComputerWeekly. What have you been reading?

Financial institutions are making fintech partnerships a key priority in 2020, according to a new study from Cornerstone Advisors. In What’s Going On In Banking2020: Outlook for a New Decade , 65% of banks and 76% of credit unions say these partnerships will be an important part of their business strategies this year.

Digitalbanks are no longer in the ‘money’ business but rather, in the ‘value’ business. Unlike in the past, when more than two products from one bank made a customer loyal, customer behavior is fleeting and their expectations for digitalbanking is increasing every day, because technology is giving them numerous choices and control.

Reality checks for community banks switching to a digital model: There is a lot of talk about digitalbanking however, not all digitalbanking falls under the same umbrella. Community banks must examine what cultural, operational and marketing shifts will happen when they adopt digitalbanking initiatives.

Banks have one of the largest IT budgets of any industry, but what exactly are organizations getting for the money? Powering innovation starts with transforming technology and its use. The banking and financial services industry nearly tops the list of largest IT budgets, spending an average 6.3 percent of revenue on IT.

If you haven’t already heard of them, EyeVerify developed mobile authentication technology they call Eyeprint ID, that replaces traditional passwords with the uniqueness of the human eye, or your “eyeprint.” How does this technology reduce costs to the traditional banking business?

Business models and adaptability will determine the success — or failure — of financial technology companies as they deal with fallout from the coronavirus outbreak.

How customers interact with their banks through an online component can often mean the difference between staying with a bank or taking their money elsewhere. Unfortunately, however, the technologies that banks are using to produce their digital components aren’t as modern as they should be.

Consumers love paying bills with their smartphones: As technology continues to develop, consumers find themselves with more options than ever before for payments. As smartwatches continue to launch and be integrated into the lives of consumers, it will be interesting to watch how this changes.

Mobile and online bankingtechnologies that the Toronto bank previously rolled out, including a virtual assistant developed by Kasisto and money management tools made by Moven, have become much more popular since the arrival of COVID-19.

Upstart, which specializes in the use of alternative data and AI in credit decisions, will make car loans directly and sell its technology to banks and other lenders.

The North Carolina bank deployed Finxact's new technology, which runs on Amazon Web Services, to make Paycheck Protection Program loans and will use it next to offer business savings accounts and CDs.

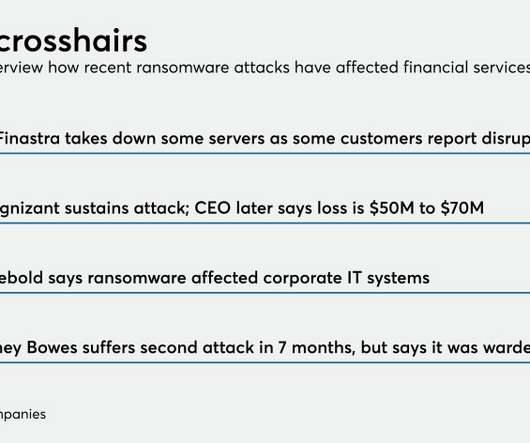

Cybercriminals have targeted at least four financial services technology companies in recent months, potentially giving hackers back-door access to clients. Here’s how banks can guard against that.

In collaboration with the credit union’s own IT team, we devised a solution that built on geo-location capabilities, a set of beacons and the credit union’s mobile banking app to take the ‘manual’ out of the process. With our solution, when the member approaches the credit union, walks in and gets a coffee, the technology does all the work.

MetaBank Bumps Up V-Card Strategy: MetaBank and StoneEagle struck a five-year extension of their partnership, which sees StoneEagle linking MetaBank’s Meta Payment Systems corporate clients into virtual B2B payment technologies. ” What have you been reading lately? ” What have you been reading lately?

Articles via The Wall Street Journal, PYMNTS.com and MIT Technology Review . Latest mobile-banking research shows laptops still reign: A recent survey of 1,000 American adults showed that Americans are still using their laptops to conduct simple banking transactions. What have you been reading?

Foreign banks for years have been using technology that folds several communication and information-sharing capabilities into one platform. Now Citigroup and others here are showing interest because of the growing importance of digital in the pandemic.

Today, consumers interact with their banks via their smartphones, computers and other devices. Value of human touch: While technological developments such as digitalbanking bring conveniences to the lives of consumers, we often forget to realize the value of human contact. What have you been reading?

Business models and adaptability will determine the success — or failure — of financial technology companies as they deal with fallout from the coronavirus outbreak.

Big Banks Still Say ‘No’ to Cloud – American Banker. Banks Need to Examine Resource Allocation – Bank Systems & Technology. DigitalBanking at JP Morgan Chase – Finextra. How Banks Are Trying to Become More Like Tech Companies – MSN Money.

Russia's largest bank is reinventing itself as a technology company and selling its own consumer electronic devices. Its chief tech officer says the moves are all about developing broader, more enduring customer relationships that the bank controls fully.

Articles via Forbes, PYMNTS.com, BankingTechnology and BankTechnology News. Meeting customers anywhere with omnichannel banking: There are more convenient, better ways to bank and consumers are quickly becoming aware of it. What have you been reading?

Bank of America ranked as “Best in Class” over 20 top U.S. Bank of America ranked as “Best in Class” over 20 top U.S. FIs must find the sweet spot at the junction of consumer privacy, cybersecurity empowerment, and cybersecurity education to maintain long-lastin. The report me.

Banks are augmenting their use of masks, distance markers and the like with apps to notify employees of exposure to infected individuals and technology meant to make branch visits safer.

The company is partnering with Sensibill, a fintech whose technology turns photos of receipts into text and helps people track and manage their expenses.

Thanks to their close relationship with the card networks, banks stand to benefit most from deals like Mastercard’s agreement to buy Finicity and Visa’s pending purchase of Plaid. The prospects for fintechs and consumers are dicier.

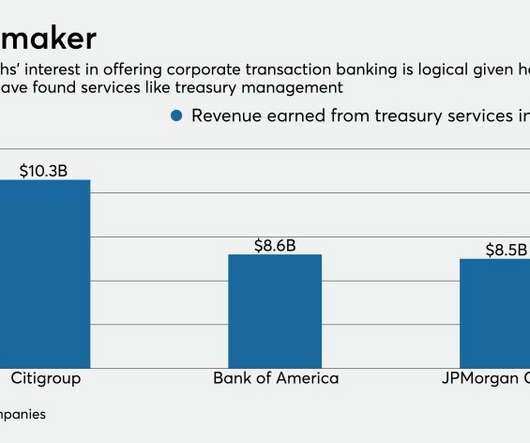

banks, betting that superior technology can lure companies with complex cash-management needs. The Wall Street firm is jumping into a market dominated by a handful of big U.S.

Question: Community branch, personal service, mobile banking—which is the odd one out? For some time now, there have been discussions about the future of community banks in the age of digitalbanking. Answer: None. Otherwise, the industry is in trouble. Things are and will be very different, no doubt about that.

Financial services organisations in China are expected to shine a light for the rest of the world when it comes to innovation in the banking sector in the coming years, with the primary drivers being non-traditional companies that are looking to develop new payment solutions and platforms. A transformed environment. Tech firms lead the way.

The company is partnering with the fintech company Sensibill, whose technology turns photos of receipts into text and helps people track and manage their expenses.

Bank of America is applying a familiar arsenal — including APIs and its popular virtual assistant, Erica — to online business banking, cross-border payments and cash management in an effort to modernize those services.

The retail banking industry has seen major changes occurring in the industry over the last few years with the adoption of mobile banking, the rise to prominence of the millennial demographic, narrowing margins, stagnant top line revenues, the future of the branch and continued regulatory changes. DigitalBanking.

BofA, which has applied for or been granted thousands of patents, has been working recently on technologies that analyze spending patterns to give budgeting advice and use augmented reality to provide estate-planning services.

Just as the onset of online banking capabilities upended traditional industry practices, the slew of mobile banking apps now on the market, and the heavy adoption of those technologies by ‘millennials’ in particular, was bound to make even online banking look old-fashioned. And then, of course, there’s the technology.

Many community banks, like Peoples Community in Wisconsin, say they proceeded despite the technological challenges presented by social distancing because the crisis has exposed the shortcomings of their digital systems.

Thanks to their close relationship with the card networks, banks stand to benefit most from deals like Mastercard’s agreement to buy Finicity and Visa’s pending purchase of Plaid. The prospects for fintechs and consumers are dicier.

Without those personal relationships to foster loyalty, banks have to find a way to digitize that feeling of being known and understood — if they want to have any hope of maintaining customer satisfaction.

Many of the new technologies that come into the infrastructure are supposed to help with those equations, and they surely do. But when it comes time to make predictions about the security issues related to those technologies, it’s a whole other story. To be blunt, banks don’t like to make predictions on cyber-crime.

Now, as part of a new report, it argues that mobile technology in particular will be key. However, the charity argues that digitalbanking will transform lives over the next 15 years and the key to this will be mobile. People can already store money digitally on their phones and use them to make purchases.

Banks compete against each other every day, courting customers with special offers and advanced services that promise to make their lives a little easier. Mobile wallets and other disruptive technologies are becoming the rule, not the exception.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content