This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

If 2019 was the year of the challenger bank, 2020 will be the year payments companies move closer to bank territory. Marqeta, the card issuing and processing startup supporting the capabilities of large companies like Kabbage and Square, sees 2020 as a big year for payments companies branching out into banking.

The alternative lending market is showing signs of defeat against traditional bank loans, and SMEs are strengthening their demands for more than the typical solutions currently offered by traditional FIs. Those services include bitcoin and peer-to-peer lending, analysts said. 65% of U.K. percent of borrower applications.

Financial institutions are making fintech partnerships a key priority in 2020, according to a new study from Cornerstone Advisors. In What’s Going On In Banking2020: Outlook for a New Decade , 65% of banks and 76% of credit unions say these partnerships will be an important part of their business strategies this year.

The Texas bank is leaning on solutions from Lightico and MANTL to quickly set up accounts and handle loans when customers can’t sign documents in person because of the coronavirus emergency.

Estimates vary, but it’s clear that tens of millions of consumers have little or no credit history, and many of them fall outside the purview of traditional lending institutions. Spotlight analytics credit digital tools lending technology' In fact, there’s enormous potential here.

The challenger bank OakNorth has been peddling its lending platform to U.S. banks for a year. When it saw COVID-19 on the horizon, it retooled to include a ratings system predicting how borrowers will be affected by the pandemic.

You recently launched CUneXus Comprehensive Pre-Screened Lending (CPL) Solution. We serve more than 73,000 members, so we’re big enough to offer a wide variety of products and services, yet small enough to offer a pleasant and personable atmosphere. Can you tell us more about that program and partnership?

The challenger bank now offers small businesses checking, lending and payments services on one platform and can link them through Plaid to external bank accounts.

This may also be an opportunity for you to discuss any savings, lending, and insurance products you offer that could be helpful. Couple could benefit from opening a savings or money market account to use as their wedding fund and discussing opening up joint accounts together in the future.

Their argument will clearly be that such draconian measures will hamper lending, which is turn will have a crippling effect on the larger economy. For the record, banks in emerging markets are at least initially exempt from the new rules.)

While those subjects lend themselves well to college football coaching and game plans, they also apply to life and dovetail nicely with banking, and Vantage West’s ability to serve its members. The launch of the series coincided with the start of the 2014-2015 college football season.

In fact, that’s why the original question is so relevant: In the world of community branches, why are personal service and mobile banking seen as being mutually exclusive? To be sure, there’s nothing quite like face-to-face interaction—it’s warm and personal, lending each transaction the ultimate human touch.

The perennial challenge in the industry is for banks to find ways to foster deeper and more satisfying relationships with clients. There are silos between banking services – front line services and lending, not to mention wealth management.

The rapid emergence of crowdfunding, alternative lending, and peer-to-peer transactions strongly indicates that small businesses are shifting away from the traditional banking environment. According to FDIC Data Calls as outlined in the Forbes , in the 4th Quarter of 2014, traditional banks’ commercial loan portfolios saw a 3.1%

Lending Club provides P2P lending, TransferWise provides international payments and remittances, but no one is aiming for the extraordinary economies of scope delivered via a singular platform that is now the norm for BATs.” . “This platform approach is key and a unique difference in China,” InnoTribe stated.

Upstart, which specializes in the use of alternative data and AI in credit decisions, will make car loans directly and sell its technology to banks and other lenders.

Westpac has been operating in New Zealand since 1861 and is one of the country’s largest full service banks with over 1.3 Westpac provides a full range of retail and commercial financial services including home and business lending, funds management and treasury services. million customers.

The owner of The Shuckery in Petaluma, Calif., says she was unable to get a Paycheck Protection Program loan until she responded to an email from the delivery service and BlueVine.

We were looking to streamline our lending process in order to provide a better experience to our customers and loan officers in order to balance an increased workload. Of late, we have introduced faster online loan approvals, online account opening, enhanced mobile access and an automated Switch Kit.

Webster Bank and Customers Bank are among the lenders that have turned to alternative data sources and automated loan reviews to assess business customers' ability to weather the coronavirus pandemic.

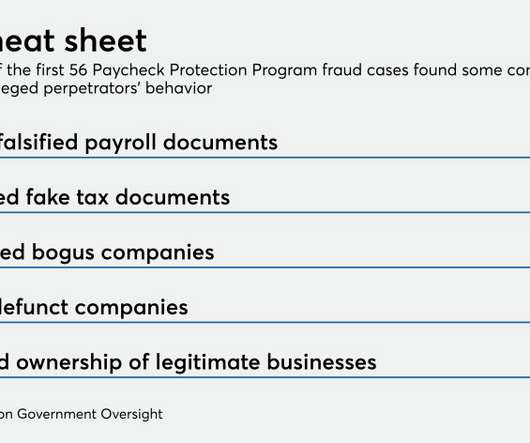

Scammers may have had more success at duping fintechs than banks in obtaining Paycheck Protection Program loans. But there are reasons for this apparent disparity.

Montecito Bank in California began streamlining originations after a natural disaster decimated its community in 2018. The move paid off when the COVID-19 crisis hit and the bank had to quickly step up efforts to help clients.

Their argument will clearly be that such draconian measures will hamper lending, which is turn will have a crippling effect on the larger economy. For the record, banks in emerging markets are at least initially exempt from the new rules.)

As alternative lending is booming, so is the demand for innovative services that support the industry. Historically, operators and leaders in the debt collection space have been long time veterans of the industry, having started as collectors on the production floor.

After tech firms assisted community bankers in processing applications in the Paycheck Protection Program, small-business lenders are continuing to engage with cloud providers and other outside companies to automate the loan forgiveness process.

Regardless of how and why they hit the market, some technology-driven innovations seem to lend themselves to particular vertical markets and/or disciplines. There are lessons to be learned from experiences in retail. Wearable technologies? Ideal for healthcare—fitness tracking alone represents a big draw, and there’s much more to come.

Digital Banking with Omni Face: In the age of IoT (Internet of Things), where the digital world (20%) is joining the enormous physical world (80%), dividing lines between industries will blur and banks will merge with non-banking world to capture value and offer customer delight.

The online lender has already branched out into facilitating payments and analyzing cash flow for small-business customers. Its new checking account is meant to round out those services.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content