This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Here’s a perfect a snapshot of how crazy technology adoption can be. In early December, there was a flood of coverage of wearable technology, mostly focused on how 2015 will be the breakout year. Of course, while most such shows analyze the past, technology forces us to look forward, hence the nuanced approach.

The pandemic has rapidly changed how banks engage with customers and employees; accelerating the shift from in-person interactions to digital engagements. Successfully leading a digital transformation requires much more than smart technology choices, culture is key.

The Banking.com staff recently connected with Alex Trombetta, Vice President of Digital Check ‘s international division, to discuss a recent study they released on ultraviolet check security and technology. Can you give a brief overview of the current state of UV validation technology? Unfortunately, in the U.S.,

Financial institutions are making fintech partnerships a key priority in 2020, according to a new study from Cornerstone Advisors. In What’s Going On In Banking2020: Outlook for a New Decade , 65% of banks and 76% of credit unions say these partnerships will be an important part of their business strategies this year.

Mobile Banking Leaves Something to Be Desired, Consumers Say – eWeek. Digital technology to open up core banking market – ComputerWeekly. Spotlight banking digital technology innovation labs mobile' How Smaller Institutions Are Trying to Get Ahead in Tech – American Banker. ? What have you been reading?

The pandemic has rapidly changed how banks engage with customers and employees; accelerating the shift from in-person interactions to digital engagements. Successfully leading a digital transformation requires much more than smart technology choices, culture is key.

It’s easy to get bogged down in the endless debate over the mingling of bankingtechnology. The bankingtechnology more than the banker will actually make the call. That’s why it can be refreshing to see startups use technology to make instant decisions about loans. So what’s the best way to move forward?

It was barely two years ago that the world’s first facial recognition payment system was developed, but now it seems this technology is set for lift-off globally. Finnish firm Uniqul launched biometric authentication technology in 2013, which used mathematical models of people’s faces to confirm users.

Banks have one of the largest IT budgets of any industry, but what exactly are organizations getting for the money? Powering innovation starts with transforming technology and its use. The banking and financial services industry nearly tops the list of largest IT budgets, spending an average 6.3 percent of revenue on IT.

Business models and adaptability will determine the success — or failure — of financial technology companies as they deal with fallout from the coronavirus outbreak.

shows that in the next two years, wearable technology and smartphone apps will be the go-to payment method. Branch Banking Lessons to Improve the Mobile Experience: Although mobile banking has become largely utilized, especially by millennials, there are a few lessons that banking apps can learn for a more traditional experience.

The Widening Worldwide Reach of Wearables: According to International Data Corporation, wearable technology such as smartwatches, smarter clothing, and eyewear will be more ubiquitous than ever in the near future. Articles via Mobile Marketing Watch, Mobile Payments Today, The Financial Brand, American Banker.

Mobile and online bankingtechnologies that the Toronto bank previously rolled out, including a virtual assistant developed by Kasisto and money management tools made by Moven, have become much more popular since the arrival of COVID-19.

If you haven’t already heard of them, EyeVerify developed mobile authentication technology they call Eyeprint ID, that replaces traditional passwords with the uniqueness of the human eye, or your “eyeprint.” How does this technology reduce costs to the traditional banking business?

Upstart, which specializes in the use of alternative data and AI in credit decisions, will make car loans directly and sell its technology to banks and other lenders.

The North Carolina bank deployed Finxact's new technology, which runs on Amazon Web Services, to make Paycheck Protection Program loans and will use it next to offer business savings accounts and CDs.

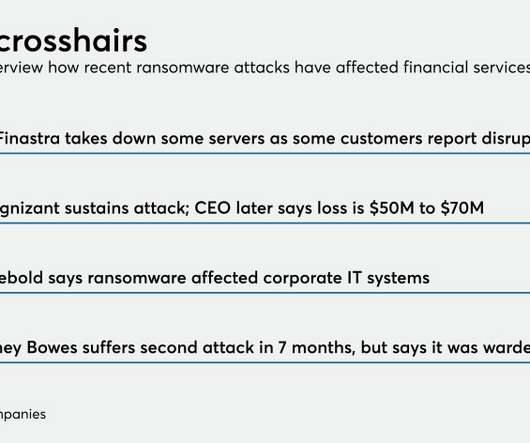

Cybercriminals have targeted at least four financial services technology companies in recent months, potentially giving hackers back-door access to clients. Here’s how banks can guard against that.

Foreign banks for years have been using technology that folds several communication and information-sharing capabilities into one platform. Now Citigroup and others here are showing interest because of the growing importance of digital in the pandemic.

Business models and adaptability will determine the success — or failure — of financial technology companies as they deal with fallout from the coronavirus outbreak.

As consumer preferences are changing as quickly as technology, it’s a challenge for financial institutions to keep up. *Disclosure: Banking.com is powered by Digital Insight. The Digital Age is here, and with it is an ongoing change in consumer behavior. Outdated business models and limited resources could spell missed revenue potential.

SMEs want banks to offer bitcoin services , suggesting the cryptocurrency may not be such a failure after all. According to new research from Accenture, which published the results in its “SME Banking2020: Changing the Conversation” report, small and medium-sized businesses are eager for more value-added services offered by their FIs.

In adopting Apple Pay, did you view this as a welcome technology? Our employees, who are accustomed to our embrace of innovative technologies, welcome Apple Pay and look forward to helping members use it. How do you think credit unions and banks who are not yet offering Apple Pay will fare? We want to hear it!

Russia's largest bank is reinventing itself as a technology company and selling its own consumer electronic devices. Its chief tech officer says the moves are all about developing broader, more enduring customer relationships that the bank controls fully.

A majority of bank CEOS—68%—are confident about their bank’s prospects for revenue growth in 2020, according to the Community Bank2020 Priorities Survey released by ABA today. The post Bank CEOs to Focus on Digitization, Talent Development in 2020 appeared first on ABA Banking Journal.

Remember, technology-aided word of mouth travels much faster and further than any other form of communication. There are many technologies and service providers available to expedite these process. But ultimately, it’s up to the banks, accounting firms and other financial services providers themselves to get moving on this.

It might sound lofty, but the truth is that seeing mobile shift purely in terms of technology is a mistake—it’s more about utility, behavior and yes, context. Thanks to the wide-scale adoption of mobile and social technologies, and the behavioral changes they induce, we now have the data needed to revamp our entire approach.

The mobile movement driving multi-channel banking – BankingTechnology. Rethinking the Bank Branch in a Digital World – Harvard Business Review Blog. Wearables in Banking: Google Glass – Celent Banking Blog. Banks work to stay relevant as technology evolves – Houston Chronicle.

Banks are augmenting their use of masks, distance markers and the like with apps to notify employees of exposure to infected individuals and technology meant to make branch visits safer.

The company is partnering with Sensibill, a fintech whose technology turns photos of receipts into text and helps people track and manage their expenses.

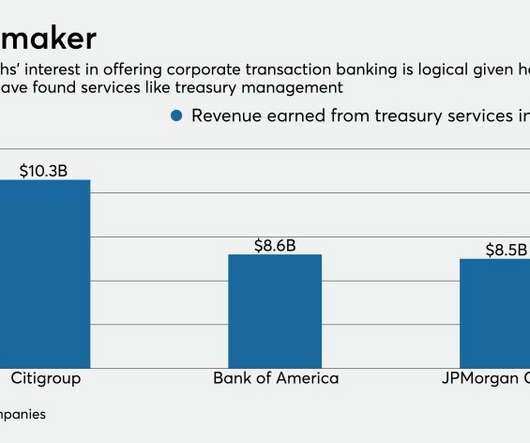

banks, betting that superior technology can lure companies with complex cash-management needs. The Wall Street firm is jumping into a market dominated by a handful of big U.S.

Animation aside, that would probably be Moneyball , an absorbing analysis of the moves made by Oakland As manager Billy Beane to rely more on technology-driven data than old-school scouting to put together his 2002 roster. Anybody remember the last time Brad Pitt showed up in a big-screen movie that didn’t have much blood and gore?

Digital Channels: Windows to Financial Institution’s Soul – Bank Systems & Technology. iBeacon Greetings Leverage Benefits for Customer Engagement Tools – Hospital Technology. Apple Pay Moves World Closer to Mobile Payment Acceptance – Wall Street Journal. What have you been reading?

Dianne shared insight on Banner Bank’s recently redesigned website and new marketing initiatives to further their approach as a “ super community bank.”. Dianne Larsen, Banner Bank. You recently overhauled your website and launched new marketing initiatives. What led to this change?

Introducing new technologies can often be a challenge when looking at customer adoption. In a few sentences, can you tell us about Westpac Bank? . Westpac has been operating in New Zealand since 1861 and is one of the country’s largest full service banks with over 1.3 million customers. Want to hear more from Westpac?

Thanks to their close relationship with the card networks, banks stand to benefit most from deals like Mastercard’s agreement to buy Finicity and Visa’s pending purchase of Plaid. The prospects for fintechs and consumers are dicier.

To be sure, in this environment of constant transformation, even the most comprehensive survey can offer little more than a snapshot in time; today’s killer app is tomorrow’s legacy technology. Even with constant platform shifts, mobile technologies cut costs while easing and enhancing personal service, even for business banking.

Financial institutions are already piloting technology that allows consumers to withdraw money from ATMs using a combination of QR codes and their smartphones. Becoming a smarter bank: With technology always changing and developing, it can be hard for financial institutions , especially smaller ones, to keep up.

New technologies and the growing number of mobile devices have prompted banking institutions to rethink their traditional way of doing business. But just because the technology is available, does it mean we should use it? Bank, “ The Balancing Act: U.S. By Dominic Venturo, Chief Innovation Officer, U.S. Of course not.

Articles via The Wall Street Journal, PYMNTS.com and MIT Technology Review . Latest mobile-banking research shows laptops still reign: A recent survey of 1,000 American adults showed that Americans are still using their laptops to conduct simple banking transactions. What have you been reading?

Today, consumers interact with their banks via their smartphones, computers and other devices. Value of human touch: While technological developments such as digital banking bring conveniences to the lives of consumers, we often forget to realize the value of human contact. What have you been reading?

To be sure, in this environment of constant transformation, even the most comprehensive survey can offer little more than a snapshot in time; today’s killer app is tomorrow’s legacy technology. Even with constant platform shifts, mobile technologies cut costs while easing and enhancing personal service, even for business banking.

The company is partnering with the fintech company Sensibill, whose technology turns photos of receipts into text and helps people track and manage their expenses.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content