This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This blog post delves into the myriad benefits of Azure Integration Services and highlights high-impact examples that demonstrate its transformative potential for financial services organizations. API Management benefits your products & customers as much as it benefits your development teams.

4 Reasons better check fraud prevention is a good investment Check fraud is on the rise. Learn how you can save time and money in the long run by updating check fraud prevention capabilities today. At the same time, check fraud is increasing dramatically. At the same time, check fraud is increasing dramatically.

This blog brings together these insights, presenting the top financial services trends for 2025. Leveraging advanced data analytics , AI, and machine learning can provide real-time insights into customer preferences, behaviors, and financial needs, creating highly individualized experiences that improve engagement and loyalty.

Takeaway 1 Implementing the FedNow Service can help reduce interbank obligations, expand market reach, and enhance customerexperiences. This blog outlines five essential steps and considerations for an effective FedNow implementation. Customize your FedNow plans Customization is key.

This blog was co-authored by: Ashley Simmons In conversations with financial services executives, Perficient consultants consistently delve into the application and usage of artificial intelligence (AI) within the industry. A pivotal aspect of this conversation revolves around the regulatory perspective toward AI.

This blog was co-authored by Perficient’s Chief Strategist and banking expert: Scott Albahary A slowing global economy, coupled with a divergent economic landscape, poses challenges for the banking industry in 2024. Personalization not only enhances the customerexperience but also strengthens the bond between banks and their clientele.

The last few years have thrown up many challenges for banks and card providers as everything has shifted online, one of the primary challenges being fraud scams. But the online shift has also created opportunities for financial institutions to demonstrate their strong fraud controls in the digital space.

Without the ability to have face-to-face branch interactions due to the coronavirus, it became imperative for financial institutions to serve customers effectively through digital channels. See how digitization can improve customerexperiences. Fraud Prevention. learn more. Balancing digitization and personal service.

ChatGPT is a powerful language model that can understand a variety of languages, including emojis, that can assist banks with increasing the productivity of bankers, improving their customerexperience, automating repetitive tasks, and providing personalized financial advice to customers.

Put simply, embedded finance is the placing of a financial product in a nonfinancial customerexperience, journey, or platform. . This may require a data transfer to a bank that will underwrite the credit or credit card or payment, leaving the non-financial firm with increased sales, but no credit, fraud, or payment risk. .

When it comes to fraud, are people worried about the wrong things? New data suggest that people are concerned about fraud, but one of the biggest threats seems to be flying under the radar, at least for consumers. That threat is fraud scams – tactics and techniques that fraudsters are using to trick people into giving away their money.

Financial institutions should be proactive with their fraud prevention on the dark web. . The demand is likely to continue growing, further fueling growth in CNP fraud. In some instances, the “buyers” do not commit the payment card fraud directly; instead, they sell the compromised payment card data in Dark Web marketplaces.

In retail banking, it’s clear customerexperience matters, and the stakes have never been higher. Study after study confirms the importance of providing personalized, integrated experiences for satisfaction and retention of financial services customers. Opportunity #2: When customer satisfaction is on the line.

Creating more efficient operations and improving customerexperiences are the goals driving technology strategies and investments at many U.S. The IT team is able to shift that time to other projects, perhaps on innovation that can improve the customerexperience or better manage operational or credit risk, or improve efficiency. “If

OCI Streaming Service and Kafka Connect – excellent Oracle blog on use cases, set up and benefits of OCI Streaming Service and Kafka Connect. Unlike the other public cloud providers, Oracle has top-rated Cloud applications for ERP, Supply Chain Management (SCM), Human Capital Management (HCM) and CustomerExperience (CX).

Without the ability to have face-to-face branch interactions due to the coronavirus, it became imperative for financial institutions to serve customers effectively through digital channels. See how digitization can improve customerexperiences. Fraud Prevention. learn more. Balancing digitization and personal service.

With less than 12 months to go until EU banks implement their strong customer authentication (SCA) solutions, project teams are facing tough decisions about the most important aspect of the business – customers making payments. The customer will have to provide at least two of the following: knowledge, ownership and inherence.

The benefits of virtual cards—increased control, reduced fraud, improved visibility, rebate opportunities, etc.—are Beyond payment technology, significant investment has been made in improving the customerexperience through user interface enhancements. Source: Accenture research and analysis of publicly available information.

Creating compelling AI omni-channel customerexperiences. Warren Raisch, IBM Executive Strategist, Watson Customer Engagement. Customers expect personalized engagement at every touch point. We’ll discuss the right platforms to handle payment volumes, putting APIs in place and preventing fraud in payments and more.

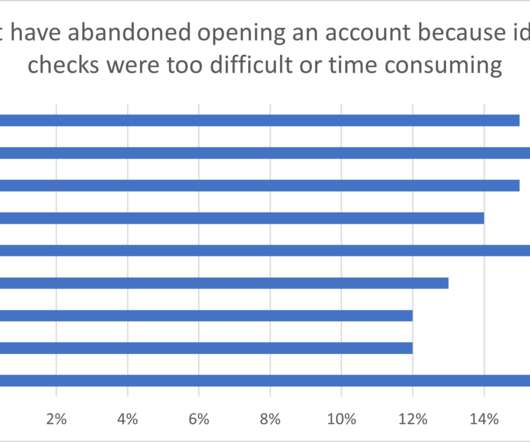

Checks such as identity proofing that get in the way are a stumbling block to success if they’re not managed without causing friction for customers. In my following research findings blog, I will look at how consumers view the methods financial institutions use to authenticate their identities and secure their accounts.

Following the highly successful The 11 Commandments of Digital Banking eBook , we are kicking off a series of 5 deeper dive blog posts that group the 11 commandments below into common themes. Many enterprises have succumbed to the inclination to digitize everything, which by default leads to cold, clinical experiences.

According to a 2022 Association for Financial Professionals report, 66% of organizations experience check fraud. Paper checks are inconvenient, slow, and prone to errors for customers. Tracking check volume by dollar and number plus check fraud should form the basis of the KPIs.

Draw from your personal, industry, or business experience. What specific technologies would you like to see us pursue for a better customerexperience? Here are some sample questions: What specific insights do you have for the next year in our market? Learn to identify emerging CRE credit risk red flags.

Biometric Security Crucial for Fraud Protection and CX. Because customers value ease of use and good fraud protection most, FIs must balance scam protection with making things easy for good customers – but not TOO easy. Customers Prefer Easy & Safe. Customers Prefer Easy & Safe. FICO Admin.

By combining new technology tools and a well-defined workflow process to create efficiency and a better customerexperience, bankers have a generational opportunity to innovate and grow earnings.“. Fraud Prevention. “But most have not materially changed their credit process in decades. Book the right loans at the right price.

Beyond the pleasure of leading a FICO Falcon Fraud Manager User Forum and moderating a couple of panel breakout sessions, I I was also able to catch up with many of the fraud-focused attendees from around the world. Scams: A Top Fraud Concern Scams are becoming a leading fraud concern, all around the world.

Before getting started, CSPs should determine who “own”’ and is accountable for subscription fraud. Is it the fraud team? Also, is there a clear and agreed fraud risk appetite that has exec sponsorship and is agreed by all stakeholders? In part, this is due to the ever-changing nature of fraud. Credit risk?

In this blog post, I’ll take a closer look at Gartner’s five key strategic initiatives that finance leaders are prioritizing in 2023 , and how Salesforce can help. Salesforce Einstein AI can be used to identify fraud and waste and to optimize financial processes.

Payments Fraud in Asia Post Pandemic. Why consumers are moving to banks with the best fraud and scam prevention. Senior Consultant, Fraud and Financial Crime. The growth of real-time payments and fraud in Asia. The appeal of these banking innovations has also made it a honeypot for fraud. Saxon Shirley.

FICO is on a mission to unlock the potential of Applied Intelligence and create a connected end-to-end customerexperience. Digital Transformation: Across industries, optimizing customerexperiences through digital transformation is a common challenge. Surprisingly, research reveals that only a fraction of the massive $1.3

Orchestration enables banks to execute processes related to customerexperience and fraud prevention. As customer journeys and fraud management processes become more integrated and digitized, the outcomes from their automated decisions can influence other decisions made along the chain.

How is application fraud evolving? And what should fraud leaders be doing to manage fraud risk in a digitally connected world? To answer those questions, we spoke with a man with 25 years of experience in fraud management, Bob Shiflet. This balancing act ultimately requires banks to set a fraud risk appetite.

I am pleased to collaborate with Conrad Sheehan in developing this blog. Instant payments are also top-of-mind as customerexperience becomes the currency of competitiveness in retail and commercial payments. Also take a moment to read Mark Quigley’s recent blog, Expecting payments, this instant! 1 InstaPay Tracker.

Half of the banks are concerned that Open Banking will make them more vulnerable to security breaches and fraud, because banks must expose their proprietary software and application programming interfaces (APIs) to allow outsiders to integrate their services. Yet like a rose bush, Open Banking also comes with some thorny threats.

Enterprise Fraud Solution Buyers Want More Agility, More Data. Our recent global survey reveals the investment priorities and functionality requirements for enterprise-level fraud solution buyers. We asked about priorities, plans and requirements for enterprise fraud prevention and detection solutions , and the results are fascinating.

Application Fraud – Does Canada Need a New Approach? FICO’s Fraud, Identity and Digital Banking Survey 2022 shows that customers in Canada want slick onboarding processes, where fraud controls work but don’t delay account opening. And what does that mean for the future of your fraud management solutions?

And you’ll be able to examine how CA’s payment security solutions have helped those banks decrease eCommerce fraud, increase revenue, reduce card operations costs and, most importantly, improve their cardholders’ overall online shopping experience. Hannah Preston. Solution Strategist, Payment Security Division, CA Technologies.

Be fascinated by your customers, not your technology. We are kicking off a series of 5 blog posts that take a deeper dive into these posts, grouping the 11 commandments into common themes. Unintentional or unnecessary friction in the customers’ experience is always bad – however, friction itself is not inherently evil.

I experienced two things: a frictionless digital payment, and a mild customerexperience victory.*. Check out the blog in the tweet below for another payment expert’s hilarious, deeply personal tangle with EMV.). The FICO® Falcon Fraud Platform plays a critical role in enabling frictionless, fraud-free digital payments.

European Card Fraud in 2021: Winners, Losers and Scams. The United Kingdom and the Nordic region continue to lead Europe in terms of digital transformation and fraud loss reduction - but non-card scams are rising fast. Senior Consultant, Fraud and Financial Crime. Senior Consultant, Fraud and Financial Crime.

Home Blog Feed test Is Hyper-Personalization a Game Changer for Fraud Management? The results are differentiating for those companies that have embraced it, serving real-time personalized customerexperiences. The areas of focus are originations and customer management. But fraud must be a consideration here too.

What Is First-Party Fraud? From banks to telcos to debt collection agencies, what looks like unrecoverable bad debt may in fact be first-party fraud. For many people, the word “fraud” evokes images of shadowy criminals using stolen identities and purloined credit card information to commit financial crimes. by Matt Cox.

I am going to keep looking forward – especially when it comes to 2020 predictions for fraud and financial crime. We all know that fraud can happen to you or your loved ones, but what we should we be doing to advocate and protect ourselves? With a more holistic approach, banks will streamline processes and improve customerexperience.

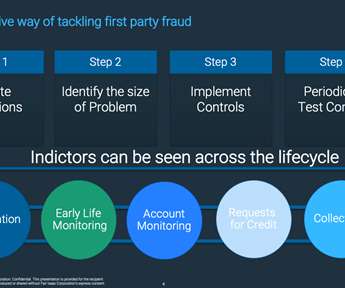

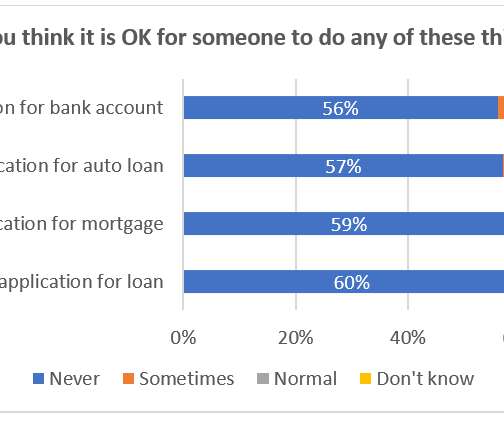

First-Party Fraud Must Be Stopped Across the Customer Lifecycle. Financial institutions face first-party risks “inside the wire” - 14% of customers worldwide think it is normal to exaggerate income on a mortgage application. Another data point demonstrates how customers view the commission of similar types of fraud differently.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content