This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The lender needs to put forth an accurate and complete picture of the borrowernot only for the borrowers sake, but also for the financial institutions riskmanagement. Focus on relevant repayment and credit risk information Whats relevant in a credit memo? Book loans faster while managingrisk.

The 2016 RiskManagement Summit features experts from the American Bankers Association, CliftonLarsonAllen, Crowe Horwath, Grant Thornton, KPMG, and Promontory Financial Group, among others. This September, Tom will deliver an address full of energy, humor and wisdom to help guide leaders on how to fully capitalize on times of change.

Meeting investment accounting and reporting requirements The right technology tools can help institutions manage investment accounting compliance and risk exposure across various investment types. Investment accounting compliance not only minimizes operational risks but also reduces regulatory scrutiny. banking regulations.

and the average exposure to office in their CRE book was between 10 and 20 percent, he said. Rising delinquency rates highlight growing risks. It also helps banks and credit unions evaluate their potential impact on earnings and capital ratios. You might also like this webinar, "Risk rating: The cornerstone of riskmanagement."

3-pronged approach Identifying and quantifying CRE risks Most financial institutions have taken a three-pronged approach to identifying and quantifying risks associated with their CRE segments. Executives should be prepared to discuss credit risk stress testing outcomes and their impact on riskmanagement decisions.

Murex , the global leader in trading, riskmanagement and processing solutions for capital markets, has accompanied Pekao on the transition to the unified integrating platform, slated to be delivered in 2022. Pekao’s implementation covers front-to-back-to-risk, cross-assets.

Meanwhile, new competitors are entering the market and tearing up the traditional banking rule book. The IBM Open Banking Platform provides a risk-managed path to digital transformation, so you can achieve fast time to market and stay ahead of regulatory requirements.

How industry analysis can improve your credit riskmanagement Understanding your customers' businesses leads to better loan pricing, structure, and riskmanagement. You might also like this webinar series, "Tackling common credit risk questions during challenging times." Get more credit risk best practices.

The negative correlation of funded business loans to the Fed funds rate is a staggering 86% as businesses weigh their needs for capital against expensive debt and lenders aim to limit risk. Almost half sought credit to grow their businesses, and 28% applied to make repairs or replace capital assets.

It is also necessary for the Board to decide how an MBL strategy fits in to the credit union’s overall strategy including designating resources, ensuring adequate capital levels and determining a safe and sound growth rate. Evaluate the level of capital needed. ” This study should include: • Industries. • Loans.

An inverted yield curve, continued bank failures, and the desire to managerisk and offer clients higher service are all factors that are driving more community banks to adopt a loan hedge program. Good hedging partners will pass on taking trades that generate revenue for the vendor but create more unforeseen risk.

An inverted yield curve, continued bank failures, and the desire to managerisk and offer clients higher service are all factors that are driving more community banks to adopt a loan hedge program. Good hedging partners will pass on taking trades that generate revenue for the vendor but create more unforeseen risk.

Takeaway 2 Enterprise value goes beyond book value to include earning potential, market position, and intangible assets. Identifying and quantifying potential economic risks associated with financial assets and liabilities becomes much easier with a fair value expert on your team. It helps align mergers with strategic goals.

But many banks and credit unions find that booking loans with a loan origination platform offers their current staff greater functionality, mitigating or eliminating those staffing woes. As our annual loan review survey pointed out, loan review units have a severe workforce shortage at both the junior and senior levels.

This means having processes and people in place for bringing in borrowers, identifying the right loans to book, pricing them correctly, and closing loans quickly and efficiently enough to meet customer needs and institutional goals. Book more loans with a faster turnaround. learn more. Survey: Repetitive data entry common.

The workshop is open to software engineers, data scientists, quantitative riskmanagers, and anyone who is interested in learning more about machine learning models and their applications in finance. *Autoencoder forward rate model in the Q-measure. Autoencoder term rate model in the P-measure. Hands-on examples in Python.

Equity investments reigned this week, thanks to backing for accounts payable (AP) automation firm MineralTree and treasury management company Kyriba , but it was the logistics market that saw the largest venture capital round — and secured another unicorn for the B2B startup space. CRV, Tenaya Capital and GV also participated.

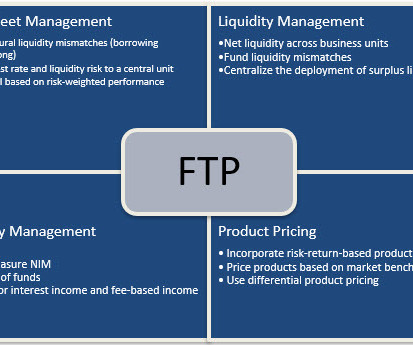

Bank executives that measure and manage the balance sheet based on the fair value of assets and liabilities invariable will change risk behavior, compensation structures, and capital allocation for the long-term benefit of shareholders. At its basic premise, FTP distributes banking profit between lending and deposits.

Bank executives that measure and manage the balance sheet based on the fair value of assets and liabilities invariable will change risk behavior, compensation structures, and capital allocation for the long-term benefit of shareholders. At its basic premise, FTP distributes banking profit between lending and deposits.

Bank executives that measure and manage the balance sheet based on the fair value of assets and liabilities invariable will change risk behavior, compensation structures, and capital allocation for the long-term benefit of shareholders. At its basic premise, FTP distributes banking profit between lending and deposits.

Typically, financial institutions can get a higher net interest margin opportunity when they book a loan than they can by buying an investment. Riskmanagement. Keys to mitigating risk. Credit RiskManagement. Lending & Credit Risk. This type of analysis (e.g. Member Business Lending. Learn More.

Credit products are one of the very few products where the customer takes the bank’s capital with the possibility of non-payment – this arrangement requires substantial scrutiny and underwriting by the bank. Commercial mortgages are long-term commitments and typically contain prepayment provisions.

Treating all credit facilities equally by setting minimum credit spreads regardless of size, term, cross-sell opportunities, lifetime value, and credit quality leads to misallocation of capital and substandard return on assets (ROA) and return on equity (ROE). Many banks target profitable commercial clients. Cost-plus pricing.

In addition, an institution cannot pass a known loss on to the government, so banks or credit unions considering refinancing existing debts on the books now will need to act quickly before financials demonstrate severe losses. Managing Liquidity Risk and Profitability in 2020 Webinar Series. Credit RiskManagement.

Profile Software , an international financial solutions provider, announced today the enrichment of RiskAvert with new capabilities like the introduction of the NPE Prudential Backstop and the Interest Rate Risk in the Banking Book (IRRBB) modules.

Because many banks are now producing below their cost of capital, growth further exacerbates their issues and drives them out of business (likely through a sale) faster. Without the windfall of profit accrued to banks in 2022 because of faster-than-expected rate increases, banks will need to be better allocators of capital.

ALM & measuring long-term interest rate risk Interest rate risk is measured through two approaches. This ALM 101 post describes the value at risk(VAR)/economic value of equity (EVE) risk perspective (long-term risk to market value of capital). It is the third in a series. . Take this example.

Booking long-term fixed-rate loans on-balance-sheet may not make sense for many banks. With no additional reporting, no additional accounting, and no capital or collateral costs, the bank retains the full relationship. Lenders can create solutions best suited for the borrower instead of being constrained by the bank’s ALCO.

Since its launch in 2016, Freightos expanded its feature set to allow businesses to actually book those forwarders, as well as manage and track shipments. ” Last month Uber Freight launched its own platform allowing shippers to access a network of logistics providers and shipping management features.

The company provides cyber insurance for the enterprise coupled with real-time riskmanagement and mitigation. The investment was co-led by Khosla Ventures, Lightspeed and Kramer Capital Partners, the firm said, and brings the total amount raised by At-Bay to $19 million. Blockchain.

Without adequate mitigation, such events may result in claims handling strain and capitalrisk for insurers. That raises a challenge for insurers: should they have adequate risk mitigation measures in place for periods that are both windy and wet? How does the windstorm – inland flood correlation impact insurers’ capital?

• The financial technology firm expands bookings by 300% in H1 2022 versus prior period. The hires include several senior hires with decades of experience in capital markets and technology: Paul Sweeney, Head of Fixed Income Development : Paul has over 20 years of experience designing and developing financial solutions.

By better modelling how this relationship might raise insurers’ capitalrisk we can more firmly argue that insurers’ model assumptions should account for key dependencies between perils. Taking whole years, we investigated how the level of capital required to remain solvent is affected. Outputs are shown in Table A.

Like GDPR, IFRS 9 poses major challenges for collectors , just as it does for accountants, IT, riskmanagers and anyone else in the credit business. Under IFRS 9, he or she has to carry provisions on an up-to-date book, to levels they never had to carry before. So now let’s talk about what you can do.

In addition, an institution cannot pass a known loss on to the government, so banks or credit unions considering refinancing existing debts on the books now will need to act quickly before financials demonstrate severe losses. SBA 7(a) loans have a maximum loan amount of $5 million, but multiple loans are allowed.

Instead of a $25K line where they can look at their books and realize they need a thousand, with what we are launching, they can push a button, and it’s there.”. We have handled authentication, and the riskmanagement and the settlement, so that all that our partners need to do is just start pushing payments,” he added.

After its most recent capital raise in September, SoFi, a marketplace lender that focuses on millennials, has raised nearly $1.5 billion in equity capital since its founding in 2011. billion in equity capital, with a market capitalization close to book value. By comparison, over 100 year old and $7.7 We don't know.

There’s a clear trajectory from daily to intra-day calculations, and in some cases even to real-time XVA calculations to help traders and riskmanagement teams make better operational decisions. Calculating large numbers of XVA sensitivities across the full range of a bank’s trading book is enormously computationally intensive.

I recently shared a long ride with a colleague discussing a Capital Plan project we were working on. In Capital Plans, you would typically use baseline projections, usually taken from the strategic plan, and apply adverse events that, based on the bank's balance sheet and strategy, can occur. JFB's Credit Risk Leading Indicators 1.

Qualifying top five venture capital investors (e.g. venture capital, growth equity, and super angel) and corporates (e.g. corporations and corporate venture capital) must have made equity investments into fintech companies listed on this market map. Capital markets. Blockchain and crypto. digital collectibles”).

If yours is a smaller institution and/or you have higher risk portfolios or segments, you need to dig deeper. Examine the true cost of capital for each slice of your business so you can think clearly about ROI and ROE. Those decisions will reduce capital consumption and generate even more funds for growth initiatives.

Borrowers could consolidate their credit debt at a lower rate, debt buyers could purchase loan packages on the hunt for higher yields and LendingClub could enjoy the relatively low-risk middle ground as the platform that underwrote and packaged the loans, but didn’t have to endure the risks involved in holding those loans on a balance sheet.

Borrowers that require a banner summer season to make their books tint green for the year are also in serious trouble. The scenarios and data an institution used in a prior stress test will help it find potential problems in unemployment, vacancy rates, collateral values, capital rates and property value trends.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content