This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In the journey to improve the payments experience, sometimes the best user experience (UX) is an unnoticeable one. He pointed to one Zoop client, Brazilian food delivery startup iFood , which recently used Zoop technology to introduce its own debit card product for restaurants on its marketplace. "No

With this in mind, PYMNTS recently spoke with Leo Castro, vice president of product marketing and brand for BigCommerce , an eCommerce platform, about the opportunities and challenges of trying to eliminate virtual checkout cart abandonment and converting tech-savvy shoppers into buyers. Importance of nailing UX.

Consumers are likelier to place their trust in brands they recognize, but Linden said they should not do so blindly. Big brands like Target , Home Depot and Equifax have experienced massive cyberattacks, while less prominent ones may be more watertight. Trust is not always based on facts.

While HSN looked to grow its mobile shopper base, both Chase and Best Buy sought to do the same after reaching an agreement to allow the credit card company to offer its digital wallet, Chase Pay, via the retailer’s mobile app.

While mobile has long been a part of the carrier offering – pay a bill, get an ID card, file a claim – this survey reflects the evolution of insurers from transactional into personalized servicing. 3) Tell Me – Authentic, Relevant Brand Messages and Experiences. 1) Know Me – Data & Analytics Relevant to the Customer.

Google’s expertise is in UX design,” he noted. “By Instead of trying to be the bank, Google is leveraging the brand name, banking infrastructure and trusted reputation of two banks, one of which is among the world’s largest global FIs, to acquire new users for that product and for Google Pay. Google’s Aim.

Rewards can help lure customers to a brand and keep them there. credit cards, 1.3 debit cards and 1.3 store affinity cards. I think merchants and issuers alike see the value of rewards in creating a storyline for customers, enhancing the relationship with the brand and driving stronger loyalty,” he added.

One of the biggest trends in fintech today is the rise of digital banking products like mobile checking accounts and new debit cards. From Square to Paypal, a host of fintechs are creating products that let consumers spend money directly out of digital accounts using a physical card. turning Digital p2p payments into debit cards.

Why you should pay more attention to card designs. A story about the humble bank card, and how they're still important, by Benedict Shegog of 11:FS. How to design a modern bank card on BankNXT.

Granted, the UX has gotten a bit nicer, and some streamlining efforts have been baked in, but at its base, Hashemi noted that it’s the same bad experience: The customer has to enter their shipping data, billing data and card information “over and over again, and multiple properties.”. Shopify Pay.

Now, five years later, many coffee brands are clamoring to compete with mobile apps, loyalty points, online payments and even home delivery services. UX, Payments and App Innovation. With major brands like Starbucks nipping at the company’s heels, being on mobile isn’t enough, he said. Costa Coffee , the U.K.’s

It seems like almost weekly I’m hearing something about a new challenger or digital-only bank brand. It had outages with its third party card processor, and then a few days later customers reported not being able to properly view their balances or display transactions. It reminds me of The Fermi Paradox.

NanoPay is finding that for mobile payments to take off, even among early adopters, using a phone to pay must be much more rewarding and convenient than tapping a card. “You want to get into as many use cases as possible,” said Greg Weed, director of card performance research at Phoenix Marketing International.

As of this publication, LinkedIn showed active listings for a UX design alchemist at Critical TechWorks and a product and solutions development alchemist at Together Abroad. “Digital prophet” was the calling card of David Shing, the Australian thought leader who took on the role at AOL in 2011. Brand Warrior.

And after PayFacs do the initial onboarding, the work begins: accepting a variety of payments, reconciling payments in to payments out, factoring in a pricing and billing engine and mapping it all to the local card rails of the country where the business is based. They have to be experts in both software and payments. Risky Business?

Discover’s responsive page dedicated to selling its Cashback Checking is a thing of beauty from top to bottom (though we have some suggestions on a few of the finer points of the UX ). But the card giant makes it easy to compare against four other major brands ( US Bank , Wells , Capital One and Fifth Third ).

This is important for financial brands to pay attention to for two primary reasons. The larger potential disruptor for financial brands is Facebook’s payment tool, known as Facebook Pay. trillion transactions, or $48 trillion, will shift from cash to payment systems, like cards, P2P, and other payment mechanisms.

This is important for financial brands to pay attention to for two primary reasons. The larger potential disruptor for financial brands is Facebook’s payment tool, known as Facebook Pay. trillion transactions, or $48 trillion, will shift from cash to payment systems, like cards, P2P, and other payment mechanisms.

youth to obtain a credit card. So most rely on debit cards for spending. However, debit cards don’t help in establishing credit for the estimated 45 million American adults without a credit score ( see note 1 ). Even before ubiquitous Visa/Mastercards, students in the ’70s and ’80s students easily obtained gasoline charge cards.

An explosion of new consumer finance brands is transforming how people save, spend, and manage their money. These companies are making it easier to make a budget, invest, and buy stocks, as well as to get loans and credit cards. debit & credit cards. In aggregate, they command $1.3 trillion in annual spending. bank accounts.

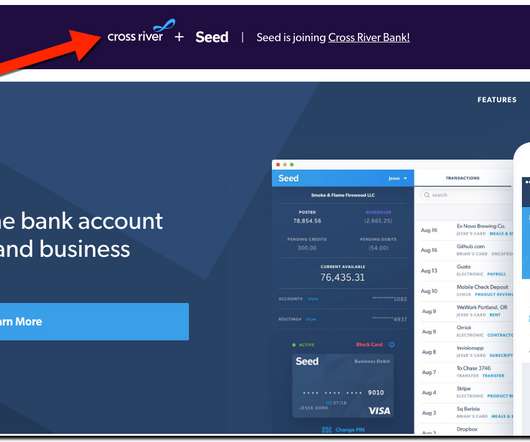

cash holding account), debit cards, and credit lines. But Brex, which only offers a corporate card and Kabbage which only offers a credit line, are not. We are also including divisions of traditional FIs, if they operate under a separate autonomous brand, such as BBVA’s Azlo. Bento for Business. FAB score : 17. Target: – HQ: SF.

Alpharank CEO Brian Ley had just shown how his Customer Influence Mapping technology enables FIs to spot highly-networked “influencers” among their customer base, and how to leverage those influencers to build better engagement and a more customized UX. “We take two to three years of credit or debit card data.

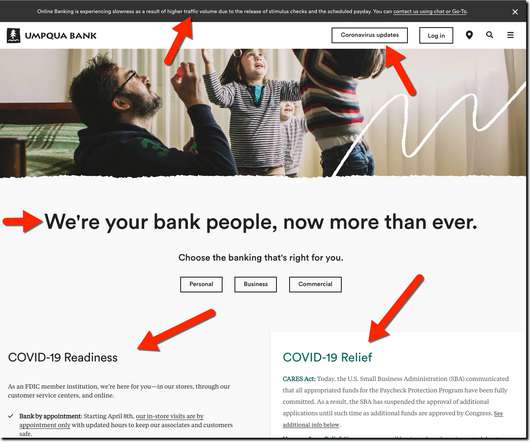

Growing a trusted brand in the financial services sectors is generally a long process. Service UX: US Bank’s Well-Designed Appointment Scheduler. And that’s just to make it to number 500. The top 10 grew an average of 250x in 3 years! It’s rare that a fintech company could ever achieve that type of velocity.

But unlike the previous initial recoveries, we’ll see strong traction from the existing fintech brands as banks finally toss out their legacy branch-based systems (which will have been proven unnecessary during the coronavirus) and funnel buckets of that money into digital tech. . Debt restructuring & interest deferrals.

As if that wasn’t enough, regulators took a sledgehammer to debit fee income with Reg II changes that will begin reducing card-not-present interchange fees starting in July 2023. Acronym of the Year – CCCA (Credit Card Competition Act). Goes to Allison Netzer and Liz High for their provocative tome, Think Like a Brand, Not a Bank.

My favorite website of all time was from the ill-fated dot-com “fintech” card issuer, NextCard. In an era where most traditional brands dumped everything they could think of on the homepage, NextCard made due with just 50 words of copy, an almost “Google-like” experience (and this was before Google).

Second Curve analyst Zack Maxfield opened a TD Bank checking account on his phone in nine minutes while he waited to speak with a teller at one of the bank’s branches, but waited an hour to fund the account and order a debit card. The 2019 Industry Oh Sh*t Moment Award – Goes to Apple and Goldman Sachs for the Apple Card launch.

” SuperMoney also hosts a wealth of personal financial information on topics ranging from auto insurance and business credit cards to tax planning and wealth management. To build the brand consumers think of first whenever they need a financial service. Lulic: Our goal is simple. We aim to get there within two years. .

Chris Messina, inventor of the Twitter hashtag and product designer for Google and Uber, wrote, “[Y]ou and I will be talking to brands and companies over Facebook Messenger, WhatsApp, Telegram, Slack, and elsewhere before year’s end, and will find it normal.”. Crafting a simple UX for a personal finance app is a tall order.

It’s been a long anticipated issue with EMV – the time it takes to “dip” a card compared to the much accustomed “swipe”. It’s not so much the time it takes, it’s more that it’s dead time – you have nothing to do but stare at a POS display waiting for the acknowledgement that you’re able to take the card out again. Insert card – check.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content