This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Meeting investment accounting and reporting requirements The right technology tools can help institutions manage investment accounting compliance and risk exposure across various investment types. Compliance with investment accounting and reporting requirements plays a central role in ensuring operational efficiency and regulatory adherence.

Now that the cannabis industry is maturing and better understood, is it time for financial institutions to take on the risk of cannabis lending? Cannabis-related businesses (CRBs)spanning everything from cultivation to retailrepresent a market in need of lending services, from working capital to real estate and equipment loans.

During the webinar, experts shared data and insights about CRE lending trends and offered advice for managing related risks. As Trepps analysis highlighted, their reliance on relationship-driven lending and tighter funding conditions make their experiences more nuanced. And in some cases, that's not going to play out, unfortunately.

Businesses' working capital cycles are longer. Bank and credit union leaders can use data to inform small business lending Small businesses are showing resilience. Thousands of banks, credit unions, and accounting firms use our risk management and lending solutions, contributing to this cooperative data model for banking intelligence.

While significantly more efficient than mailing forms to the SBA, there are some shortfalls to E-Tran, and a vendor can help Loan submission platform Leveraging E-Tran for increased SBA lending The U.S. Understanding the role of E-Tran in SBA lending is the first step for banks and credit unions to ensure smooth loan processing.

Automating the key steps that often occur in the back office leads to faster decisions, stronger customer or member relationships, and more profitable lending to small businesses. This article covers these key topics: Cultivating fertile ground for small business lending Do large lenders have an advantage in small business lending?

Boost your small business lending efforts from the bottom up Small businesses play a crucial role in our economy, and one of the critical factors in their success is access to funding. You might also like this guide for smarter, faster small business lending.

In 2015, news outlets ran articles about the “ gold mine ” of venture capital investments in the alternative finance sector. But there is evidence that investors’ appetite for alternative lending startups is on the wane, even as overall FinTech funding continues to climb — and as the success of the alternative lending market grows, too.

The most-read lending & credit blogs in 2023 Probability of default, CECL model validation, and stress testing were among Abrigo's top blogs on ALM, CECL, and portfolio risk this year. Takeaway 2 The top lending and credit blog posts focused on the benefits of banking technology, interest rate management, and developing risk ratings.

Develop an MBL program while mitigating risk Credit unions looking for alternate paths to growth in today's rising rate environment may be primed to leverage member business lending. Takeaway 3 The specific policy areas outlined below should be carefully considered by credit unions engaged in member business lending.

While Chinese traders are limited to the purchase of up to $50,000 of foreign currency annually, the volume suggests stablecoins could be being used to circumvent the regulation, according to Chainalysis , the New York-based provider of regulatory compliance software.

Tremors are running through the alternative lending space. Perhaps most ominously, Lending Club CEO Renaud Laplanche suddenly stepped down when Read More. Prosper raised rates, cut staff, and saw a chilly reception from investors for its latest securitization. OnDeck saw shares slide to 30% of their IPO value.

Like many venture capital companies in the payments space, Serent Capital has had a busy year. 15 with the announcement of the launch of its fourth fund, Serent Capital IV — at $750 million. 15 with the announcement of the launch of its fourth fund, Serent Capital IV — at $750 million. That was followed on Dec.

Lending Club survived a brutal second quarter (barely) and is considering some fundamental changes to thrive going forward. Specifically, the beleaguered marketplace lender will consider funding its own loans rather than selling them off post-origination.

The round was led by Blockchain Capital, Standard Crypto, Blockchain.com Ventures and more. Aave recently announced its governance model to help the community access more participation, with old Aave token LEND now able to be swapped for the new Aave token at a ratio of 100 LEND to 1 Aave.

The marketplace lending industry is far from dead. This was the upshot from a venture capital panel at a recent Bank Innovation event in San Jose. Rather, it’s going through a reboot, which will include improved software, increased focus on regulation, and improved transparency.

According to a recent survey by the American Bankers Association (ABA), more than 46 percent of respondents had to reduce offerings for loan or deposit accounts, or other services, at their bank because of regulatory compliance burdens.

“There is a lot of time and energy spent, not only making sure that credit decisions are appropriate, but also managing the compliance aspect,” Maher says. Although the surge in PPP lending highlighted a need for loans among underserved borrowers, it also has led to some creative solutions.

Davies , head of lending at Figure, will spearhead the firm’s initiatives to get a bank charter from the OCC and he will become the Figure Bank chief executive officer, according to Cagney. Davies served as CitiMortgage’s chief executive officer and Citibank’s head of global mortgage in addition to Capital One’s president of home loans.

The opportunity ship has sailed for personal finance management, lending, or robo advisory sectors of fintech, according to Rebecca Lynn, co-founder of venture capital firm Canvas. So where are investors looking for new opportunities?

The two primary issues keeping some lenders from the top of their home equity game are 1) ambiguity in the ownership of their home equity functions and 2) a lack of maturity in their lending systems and processes. Some lenders do a solid job repurposing mortgage lending staff into home equity roles.

Regulators the world over are beginning to take a closer look at the alternative and marketplace lending business model. Also, in China, analysts at Yingcan Group pointed to the government’s P2P and marketplace lending crackdown as being likely to shrink the industry by as much as 70 percent this year. In the U.S., In June, the U.K.’s

” There is a real opportunity here for community banks to position themselves within this movement and capitalize on what the consumer sees as their strengths— relationship-based lending , tailored product offerings, and knowledge of the local community. Develop a relationship-based lending framework.

FinCrime fighters aren’t just checking boxes for compliance. It’s about supporting the people who safeguard banks and credit unions from the growing threats of financial crime and who keep capital flowing to small businesses and families. Staying on top of fraud is a full-time job. Let our Advisory Services team help when you need it.

That’s what the industry needs: competing marketplace lending associations. Today, the three big names in marketplace lending (for now — more on that below) that were not in the just-launched Marketplace Lending Association have formed the Innovative Lending Platform Association.

This week’s look at these partnerships and data integration efforts finds a focus on small business lending and compliance, while some newly forged partnerships are also looking to help banks strengthen their own FinTech collaboration agreements. Finovate Capital Adds MonetaGo Technology. Billy Reveals Open Banking Plans.

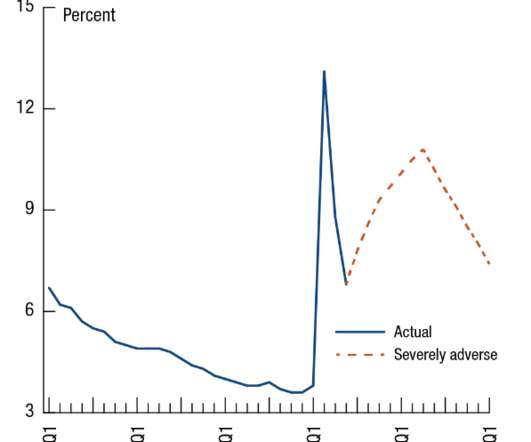

Federal bank regulators work together to design Comprehensive Capital Analysis and Review (“CCAR”) stress tests that are designed to ensure that even in the case of a severe recession, significant banks can lend to households and businesses. As repeated by federal bank regulators, the required economic scenarios are not forecasts.

Last week, I participated in a Finextra webinar on the topic of “Connected Credit and Compliance for Lending Growth” with panelists from ING, Vertus Partners, Misys and Credits Vision. Cost of compliance. Changing client expectations. Competition from new entrants.

In 2020, the Federal Reserve found that large banks were generally well-capitalized under a range of hypothetical events. The Fed’s Comprehensive Capital Analysis and Review (“CCAR”) stress tests are designed to ensure that large banks are able to lend to households and businesses even in a severe recession.

Following the recent financial crisis, the Basel Committee of Banking Supervision (BCBS) set out to “strengthen global capital and liquidity rules with the goal of promoting a more resilient banking sector.” The three pillars include maintaining minimum capital requirements, a supervisory review process and market discipline.

Bombay Stock Exchange (BSE) has relaxed guidelines for how Indian small- to medium-sized businesses (SMBs) can tap the capital market, loosening restrictions on net tangible assets and positive cash flow in order to jump-start the country’s virus-ravaged economy.

The gen AI consultant can talk intelligently about leadership, bank performance, financial structuring, marketing, lending, legal, compliance, and deposits. Nuanced questions about human capital or culture tend to be nuanced and difficult for Gen AI to opine accurately on. The right questions are also important.

It’s been a brutal year for the alternative lending industry. Scandals, staff cuts, rate hikes, and recently a Lending Club investment posted its first negative return in five years this August.

While regulators had transparency and financial security in mind when introducing more stringent requirements for banks following the global financial crisis, financial institutions faced a sudden surge in the burden compliance. The Key To Compliance Is Data.

Two years ago today, Lending Club was ringing the bell on an IPO that one early investor called “a no-brainer.”. Lending Club’s model does not need bank branches on each street corner, and it can turn around in minutes and hours, not days. “I So what went so right for LendingClub two years ago today at its IPO — and then so wrong?

The Hong Kong Monetary Authority has, as finews.asia reported this past week, amended its credit risk management guidelines in a way that seeks to boost the embrace of analytics when lending to smaller firms. The solution ensures compliance with the second payment services directive (PSD2).

Compliance and Decision-making. Distinct risk management processes can be both effective for satisfying compliance requirements and helpful for strategic decision making. Likewise, liquidity shock tests provide clarity and guides decisions around raising capital, concentration limits, and excess capital. CRE Lending.

Here are the five companies of Class 4 of INV Fintech: Bloxable: Bloxable provides decentralized solutions for lending origination and the securitization of mortgages […]. The six companies were chosen from among a wide array of applications from across the globe.

This post investigates whether large and small banks in the UK and US differ in the cyclical patterns of capital positions and credit provision. The reforms aimed to ensure that banks have sufficient capital resources to absorb losses and reduce the cyclical effects of bank capital (and regulation) on the supply of bank credit in stress.

You might also like this webinar, " AML Compliance and Sanctions Requirements for Non-Bank Financial Institutions. Streamlined compliance : Compliance with varying state regulations significantly burdens money transmitters. Compliance and reporting : Mandate implementing robust AML and CTF programs by money transmitters.

Banking reports to inform risk management and strategy These reports on capital, growth, and liquidity help financial institutions spot warning signs. Takeaway 2 Reports that assess capital, growth, and liquidity provide banking professionals data to drive decisions. Regulators review them to assess safety and soundness.

Informal actions are generally appropriate for institutions that receive a composite rating of “3” for safety and soundness or consumer compliance. Section 38 of the FDI Act authorizes the FDIC to issue Prompt Corrective Action directives to institutions that are less than adequately capitalized. Inadequate capital. Learn more.

Large banks will have capital requirements of up to 13.4%, to ensure their survival in a severe recession and to still be able to lend Risk Management Compliance Duties Feature3 Feature.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content