This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

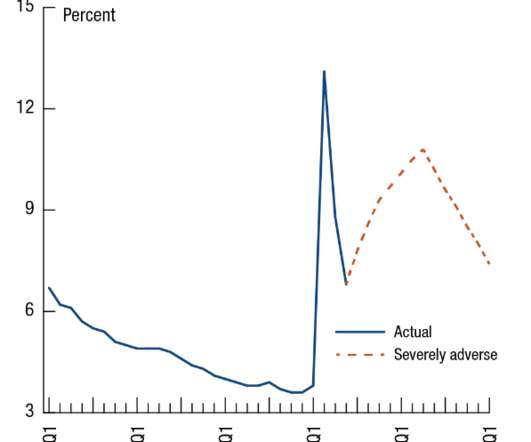

The Fed’s Comprehensive Capital Analysis and Review (“CCAR”) stress tests are designed to ensure that large banks can lend to households and businesses even in a severe recession. The 23 large banks tested remained well above their risk-based minimum capital requirements.

In 2020, the Federal Reserve found that large banks were generally well-capitalized under a range of hypothetical events. The Fed’s Comprehensive Capital Analysis and Review (“CCAR”) stress tests are designed to ensure that large banks are able to lend to households and businesses even in a severe recession.

On balance, the literature is critical of loan forbearance in the corporate sector because of its potential to contribute to zombification a situation where bank lending keeps unproductive firms alive, resulting in lower aggregate total factor productivity. The Act boosted the aggregate capital stock by 1.4% on average over 201018.

Federal bank regulators work together to design Comprehensive Capital Analysis and Review (“CCAR”) stress tests that are designed to ensure that even in the case of a severe recession, significant banks can lend to households and businesses. As repeated by federal bank regulators, the required economic scenarios are not forecasts.

‘Zombie lending’ occurs when a lender supports an otherwise insolvent borrower through forbearance measures such as repayment holidays and temporary interest-only loans. In a recent paper , I examine whether these lending practices contributed to the subsequent low output experienced by the euro area. Belinda Tracey.

Top down and bottom up analysis can inform capital assessments. Effective stress testing can benefit many different facets of lending, from risk management and strategic decision-making to capital adequacy and liquidity management. Stress testing and capital adequacy. Stress testing and risk management.

Today in the payments news roundup, Stripe launched Stripe Capital to simplify the way internet companies can access funds. Stripe Gets Into Lending. Stripe unveiled the rollout of Stripe Capital to simplify the way internet companies can access funds. Also, commercial and consumer cards issued in the U.S. generated $6.13

The gen AI consultant can talk intelligently about leadership, bank performance, financial structuring, marketing, lending, legal, compliance, and deposits. Nuanced questions about human capital or culture tend to be nuanced and difficult for Gen AI to opine accurately on. The right questions are also important.

Banks consistently produce under their cost of capital. However, for the average bank, their cost of capital is between 9% and 14% depending on the bank’s equity liquidity with an average of 12.5%. As an industry, we misallocate capital. You can’t develop lending expertise overnight. Why is that?

It also means removing ritualistic contentsuch as unnecessary analysis of debt service coverage for a working capital linewhen it doesnt directly relate to how the loan will be repaid. But they shouldnt be an exercise in verbosity or regulatory appeasement. Kirby suggested focusing on what truly affects repayment and credit risk.

Financial institutions that want to play in the small business lending sandbox need to bring their digital toys. But how can community banks successfully compete with big banks and fintechs that are spending billions on their digital lending capabilities? Source: DeBanked ) Square Capital lent about $1.6 Source: DeBanked ).

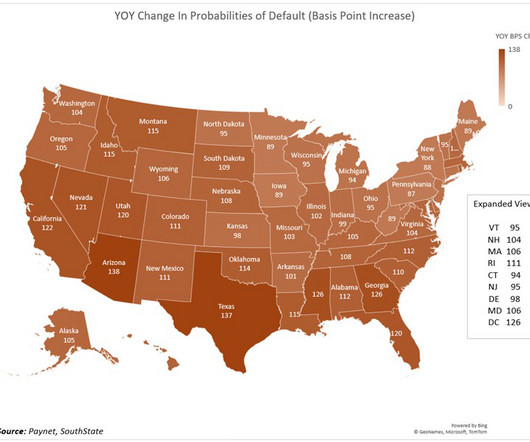

Lending is getting riskier. This data is critical for pricing, capital allocation, and marketing. As can be seen, the consumer is starting to feel the credit shock first while commercial lending is still performing. Minnesota, North Dakota, and Iowa were the least risky states to lend into. This quarter, it is 2.58%.

Enterprise value, or the fair value of the acquired credit union, becomes the imputed “purchase price” of the transaction and acts as the baseline in the purchase price allocation exercise for goodwill determination. Enterprise value considers more than just the book value of a credit union's assets and liabilities.

Are there high capital or technological costs? View specific examples of industry analysis in practice in this webinar Contact experts Watch Now Conclusion The long-term benefits of incorporating industry analysis Industry analysis is not an academic exercise. Barriers to entry: Is this an industry that is easy to get in or out of?

Takeaway 3 Using stress testing scenarios helps banks and credit unions determine whether estimated loss rates will push projected capital levels below regulatory thresholds. Banks and credit unions must be able to adjust when necessary to ensure viability of the institution and the ability to supply capital to their local economy.

have already used an alternative lending platform, particularly among younger entrepreneurs. “It can be a hugely time-consuming exercise researching all the traditional and alternative financing solutions on the market.” firm that bridges companies with a range sources to obtain loans, equity financing or grants.

unsecured lending is bad rather than unsecured lending should only be extended to high pass risk rated credit). The following is an example of how I would address the structural exception of non-recourse lending. a significant capital injection into the borrower, or other collateral such as liquid assets).

Strategic Horizon and Capital As mentioned, the problem that bank’s often run into when it comes to strategic planning is their time horizon is too short. The fundamental problem is a bank’s implied average life of capital is long, some 18+ years, but their strategic horizon is too short – likely under three years.

With a risk rating system in place that allows for accurate and consistent ratings, portfolio managers can perform a variety of risk management exercises such as setting the reserve, stress testing, capital planning and strategic planning.

ALM | 4 minute read Key Takeaways Many financial institutions view asset/liability management as a "check-the-box" regulatory exercise. An extreme focus on using ALM to manage the risk of rising rates means some FIs overlook using ALM to grow earnings and capital, putting them at risk of underperformance. Lending & Credit Risk.

There is also a risk of higher loan defaults eroding banks’ equity capital, which could lead banks to tighten lending conditions. However, this effect is small in our model given the size of banks’ capital buffers. Given this, there would be little additional benefit to raising bank capital requirements further in our setting.

Lending Discipline: Hedging programs make loan pricing more transparent and force bankers to exercise sensible pricing methodologies. This capital ratio is used to assess the possible riskiness of a hedge provider.

25% 140 banks will have capital levels that have fallen below 8%. So far, bankers have taken comfort in the soundbite that “this crisis is different” because of the strong capital levels and risk management rigor that has developed since the Great Recession. Practice the art of surgical lending.

Analysis should be performed on concentrations, as a percentage of capital, in terms of: (1) Collateral type such as multifamily, retail, office, etc. (2) This exercise may reveal the need for bigger-picture data analysis. For example, your top goal for next year might be to expand your lending geographic footprint.

Stress testing gives an institution a serious look into their capital and reserves, and if they possess enough of each to remain viable, should a recession hit. Both CECL and stress testing take top-down and bottom-up approaches to test the capital adequacy of a financial institution. Portfolio Risk & CECL. Learn More. Credit Risk.

Although our Tier 1 leverage ratio is greater than 10%, you criticized us for our stress scenarios contained in our capital plan. Aside from the clear lack of analytic rigor you exercised to come to this conclusion, it is important to remind you that estimating future negative events that impact our capital is guesswork.

Lending execs across the country were clearly dissatisfied with how manual processes and lackluster technology were used to stumble through those massive re-fi volumes. Bankers face a lot of work and challenges as they attempt to marry new lending systems with elegant, customer-friendly lending processes. Now we’re talking! .

A recent round of bank merger announcements and the marquee Capital One/Discover deal illustrate this mantra’s popularity. An exercise Cornerstone likes to conduct: Take a look at the top 20% of the bank’s headcount and review comp and bonus in descending order. Why is this important?

In the future, people could shop, exercise and socialise within the metaverse. This interoperable capacity has been showcased by decentralised finance (DeFi), which replicate financial services such as lending and exchange typically conducted by a centralised authority, but in a decentralised manner.

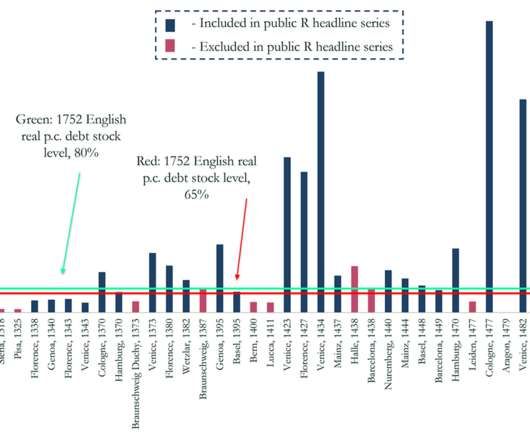

The yellow and blue series display the new “global” data in nominal and real terms: these have to be constructed from a wide array of scattered archival and printed sources, and should be thought of as a DM public long-term debt series that incorporates both consolidated and unconsolidated voluntary lending across the full risk spectrum.

David Blumberg, founder and managing partner of Blumberg Capital, said the research indicated a “huge opportunity for fintech companies to grow and scale as more consumers begin to recognize the benefits of fintech” A separate report from KPMG , focusing on the UK market, revealed that total investment in fintech reached $1.4

The main challenge with CECL is that it will require higher levels of capital to be kept in reserve and lead to changes in lending practices and portfolio and product management. Those who best implement CECL will have greater retained earnings and lendingcapital than their competition. Sound appealing?

A Connecticut federal district court has refused to dismiss claims filed by the CFPB against a mortgage company and three of its principals for alleged Truth in Lending Act (TILA), Mortgage Act and Practice (MAP) Rule, and Consumer Financial Protection Act (CFPA) violations.

If you want the head of commercial lending or retail banking to take ownership of the continuous improvement of their spreads so the bank can improve its net interest margin, you must first measure it. Some financial institutions consider strategic planning a regulatory exercise or look to do it themselves to save money.

For example, alternative lending saw consolidation in 2017 as investment to VC-backed alternative lending companies swung heavily to growth-stage companies like unicorns Kabbage , SoFi , Affirm , and GreenSky , all of which raised $100M or more in 2017. Slowdown in 2018?

Decentralized Finance, Blockchain, and CBDCs Why Peer-to-Peer models fail against oligopoly, with Lending Club shutting down p2p platform, Seedrs/Crowdcube merging, and Morgan Stanley buying Eaton Vance for $7B. the Lending Clubs) end up becoming banks and seeking the thing it looked like they would disrupt. They all (i.e.,

Decentralized Finance, Blockchain, and CBDCs Why Peer-to-Peer models fail against oligopoly, with Lending Club shutting down p2p platform, Seedrs/Crowdcube merging, and Morgan Stanley buying Eaton Vance for $7B. the Lending Clubs) end up becoming banks and seeking the thing it looked like they would disrupt. They all (i.e.,

The business model here needs to focus on a strategy that balances lending growth while keeping risk in check. With this approach, loan pricing is not an isolated exercise. It's a strategy that requires accurate customer validation and data analysis, with an emphasis on action-effect modelling rather than hypothesis.

Three years later, for many, it is now rightly recognised as perhaps the most important pillar of our health and wellness, alongside exercise and diet. BTCjam, a P2P marketplace launched in 2012 to borrow and lend using bitcoin, announced the company has made “the difficult decision” to close up shop, according to multiple news sources.

But should a board, in exercising their fiduciary duties, perform this analysis routinely without determining to sell the FI first? Strategy execution typically lends itself to a long-term view. In its simplest form, the discount rate in the above sample should be the shareholders'' expected capital appreciation of the FIs stock.

More importantly, no one is going to spend political capital to move mountains in Washington over a possible problem. The fraudulent activity of several Wells Fargo employees is a sobering reminder that governance and risk management shouldn’t simply be “check the box” exercises.

More importantly, no one is going to spend political capital to move mountains in Washington over a possible problem. The fraudulent activity of several Wells Fargo employees is a sobering reminder that governance and risk management shouldn’t simply be “check the box” exercises.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content