This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The lender needs to put forth an accurate and complete picture of the borrowernot only for the borrowers sake, but also for the financial institutions riskmanagement. Focus on relevant repayment and credit risk information Whats relevant in a credit memo? Kirby suggested focusing on what truly affects repayment and credit risk.

Stress Testing | 7 minute read Key Takeaways Stress testing is an important component of sound riskmanagement. Top down and bottom up analysis can inform capital assessments. Stress testing provides banks and credit unions with a unique opportunity to better manage their institution’s financial performance. .

Most people who exercise regularly can vouch for the side benefits of physical activity. Incorporating some of the findings from the stress tests into strategic plans, forecasting, and other riskmanagement processes can provide more value. “It Incorporate into capital-planning process.

How industry analysis can improve your credit riskmanagement Understanding your customers' businesses leads to better loan pricing, structure, and riskmanagement. You might also like this webinar series, "Tackling common credit risk questions during challenging times." Get more credit risk best practices.

Mastercard’s Vocalink’s offering supports the requirements of Payments Canada, such as the Bank of Canada’s riskmanagement criteria and ISO 20022. Railsbank, the British Banking-as-a-Service (BaaS) upstart, completed a $37 million funding deal co-led by Ventura Capital and MiddleGame Ventures.

Takeaway 3 Using stress testing scenarios helps banks and credit unions determine whether estimated loss rates will push projected capital levels below regulatory thresholds. Regardless of regulatory pressure, measuring and managing key risks are the cornerstone of community financial institutions’ enterprise riskmanagement (ERM) programs.

During the risk rating process, the lender is determining the borrower’s ability to repay the loan and assessing the potential volatility of future loan payments. Finally, a risk rating can help the lender determine if they will reprice or re-structure the loan when it comes time for renewal.

ALM | 4 minute read Key Takeaways Many financial institutions view asset/liability management as a "check-the-box" regulatory exercise. An extreme focus on using ALM to manage the risk of rising rates means some FIs overlook using ALM to grow earnings and capital, putting them at risk of underperformance.

Curry added, “We have recommended authorizing a basic set of powers that both federal savings associations and national banks can exercise, regardless of their charter, so that savings associations can change business strategies without moving to a different charter.”

Benchmarking can help banks better optimize capital as it gives bank management a sense of what the average is for the industry. In comparison, 25% is capitalized and depreciated over three, five, or ten years, depending on the nature of the expense. How does your IT investment move you within your risk envelope?

Strategic Horizon and Capital As mentioned, the problem that bank’s often run into when it comes to strategic planning is their time horizon is too short. Riskmanagement also needs to change. Finding your bank tied to a rural area that is decreasing in size and profitable demographics is your bigger risk.

Enterprise value, or the fair value of the acquired credit union, becomes the imputed “purchase price” of the transaction and acts as the baseline in the purchase price allocation exercise for goodwill determination. Enterprise value considers more than just the book value of a credit union's assets and liabilities.

Non-recourse loans While the bank historically has not experienced excessive levels of charge-offs due to loans not having one or more guarantors, there is considerable evidence to show that the options available to resolve a problem situation, as well as the costs incurred to exercise such options, are adversely affected by the lack of guarantees.

Lending Discipline: Hedging programs make loan pricing more transparent and force bankers to exercise sensible pricing methodologies. This capital ratio is used to assess the possible riskiness of a hedge provider.

This in turn means greater risk of ‘debt deleveraging’ by heavily indebted households and firms, who may be forced to reduce their spending in order to meet their debt obligations, potentially amplifying any recessionary effects. However, this effect is small in our model given the size of banks’ capital buffers.

Stress testing gives an institution a serious look into their capital and reserves, and if they possess enough of each to remain viable, should a recession hit. Both CECL and stress testing take top-down and bottom-up approaches to test the capital adequacy of a financial institution.

Without adequate mitigation, such events may result in claims handling strain and capitalrisk for insurers. That raises a challenge for insurers: should they have adequate risk mitigation measures in place for periods that are both windy and wet? How does the windstorm – inland flood correlation impact insurers’ capital?

It turns out that confidence is more valuable than capital. While we wrote about the root cause of the failure of Silicon Valley Bank (SVB) HERE , the lessons of the current banking crisis go beyond interest rate riskmanagement. The ratio would provide a bank’s current core capital position to risk-adjusted assets.

By better modelling how this relationship might raise insurers’ capitalrisk we can more firmly argue that insurers’ model assumptions should account for key dependencies between perils. Taking whole years, we investigated how the level of capital required to remain solvent is affected. Outputs are shown in Table A.

Failing to understand and account for these options can lead to ineffective modeling and riskmanagement. Further, the bank, and customer, have other, non-interest rate reasons for exercising their option, most notably safety. We are in a period of very high volatility, and the full impact of this optionality may not be correct.

For this and other reasons, now is a good time to review and refresh articles, bylaws and committee charters to ensure resilience and bolster riskmanagement. But if they see it as a riskmanagement tool, it’s a game changer. He also recommends not updating the resiliency document as only a “table-top exercise.”

25% 140 banks will have capital levels that have fallen below 8%. So far, bankers have taken comfort in the soundbite that “this crisis is different” because of the strong capital levels and riskmanagement rigor that has developed since the Great Recession. Benchmark every function and drive excellence.

It’s been nearly a decade since the financial crisis exposed how a weak riskmanagement framework and lack of governance can almost permanently debilitate even one of the strongest capital markets. Regulators are exercising their new oversight by increasing the costs of non-compliance.

Instead of going to the gym, they’re climbing on their Peloton bikes or exercising in front of their Magic Mirrors with trainers and others who are part of those digital fitness communities. And instead of investing in tickets to go to a game, they’re investing in smart flat-screen TVs to watch live sporting events at home with friends.

Instead of going to the gym, they’re climbing on their Peloton bikes or exercising in front of their Magic Mirrors with trainers and others who are part of those digital fitness communities. And instead of investing in tickets to go to a game, they’re investing in smart flat-screen TVs to watch live sporting events at home with friends.

Organisations are being permitted to use their capital buffer to help in the current situation. Organisations need to be agile to incorporate the changes and they will need to revisit their models to rate the real risk. Management are reminded that the current very fluid situation is hindering reliable forecasts.

There have been significant numbers of forbearance requests from customers, and C&R teams will need to exercise discipline regarding when and how forbearance is provided. For example, BaFIN (the Federal Financial Supervisory Authority in Germany) is offering some freedom in their assessment of capital requirements.

a nice, detailed set of thinking on Yearn, the most advanced tech that DeFi has to offer: Mergers and Acquisitions in open-source Decentralized Finance, and its $5 billion market capitalization. Much of this is an exercise in grim arithmetic. It’s got your yield farming and your Pickles and Creams. Slowing GDP growth by 1.5%

a nice, detailed set of thinking on Yearn, the most advanced tech that DeFi has to offer: Mergers and Acquisitions in open-source Decentralized Finance, and its $5 billion market capitalization. Much of this is an exercise in grim arithmetic. It’s got your yield farming and your Pickles and Creams. Slowing GDP growth by 1.5%

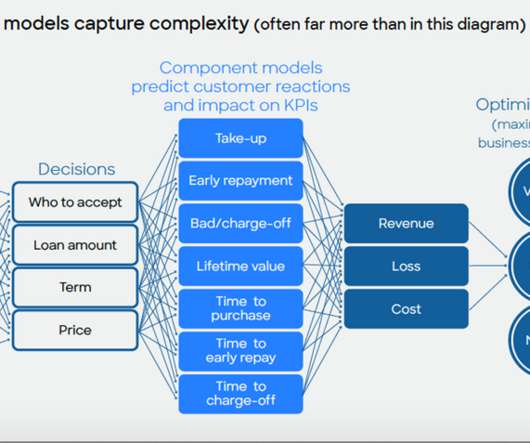

The most popular posts in our Customer Development category dealt with digital banking, optimizing credit line increases, loan pricing and machine learning for credit risk models. With this approach, loan pricing is not an isolated exercise. Instead, loan prices are optimized within the context of the entire customer offer.

More importantly, no one is going to spend political capital to move mountains in Washington over a possible problem. The fraudulent activity of several Wells Fargo employees is a sobering reminder that governance and riskmanagement shouldn’t simply be “check the box” exercises.

More importantly, no one is going to spend political capital to move mountains in Washington over a possible problem. The fraudulent activity of several Wells Fargo employees is a sobering reminder that governance and riskmanagement shouldn’t simply be “check the box” exercises.

As federal borrowings increase, those borrowings crowd out (reduce) capital available for private investments. A smaller supply (of private capital) increases required return on capital and interest rates. Further, orthodox economic understanding is that as federal debt grows, general interest rates in the economy rise.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content